How to survive a bear market?

The financial media tells me that the US Federal Reserve and the RBI will soon raise interest rates because inflation is out of control. If inflation is hot, interest rates rise, and the Fed stops printing money, liquidity will dry up, and the markets will apparently crash between 50-80%. According to the “experts”, the target for the Nifty 50 is 5000 with strong support near 0.

It’s just stunning and frankly a bit funny how quickly the sentiment in the markets went from euphoria in 2021 to despair in 2022. There’s no denying that the markets look weak. The Nifty 500 is down by just 3.3% year to date (YTD), but 50%+ of the stocks are down between 20%-50% from their 52-week highs. It’s the same in the S&P 500 as well—high-flying growth stocks have fallen back to earth.

So, why are people freaking out? What’s happening? Are we headed for a serious crash? What should you do? What follows is the most boring and obvious post ever.

There’s always a reason to sell

The first thing to remember is that there’s always a reason to sell. You often hear more bearish views than bullish views. But the peculiar thing is we are innately optimistic.

Professor Tali Sharot, who teaches cognitive neuroscience at University College London, found that we are wildly optimistic about ourselves and underestimate the odds of bad things happening. But we tend to be quite pessimistic about the world in general. This explains why bearish news can travel around the world while bullish news is still putting on its shoes.

I made a chart with some of the biggest “world-ending events” overlaid on Sensex since the 1980s. We’ve kept seeing events that could trigger the next big crash every few years, but despite that, the Sensex kept chugging along. Investing requires a fair bit of optimism, I guess.

Journey of Sensex since 1980 (open image in a new tab to enlarge).

This chart shows you the peak to bottom fall of BSE Sensex, Midcap, and Smallcap indices. Take a look at 2008, 2012, 2016, and 2020. Those are what real crashes look like. Look at the extreme right of the chart, that’s 2022, and that’s what investors are freaking out over. Sure, it could get worse, you don’t know that, and neither does anybody else.

Historical drawdowns

So, what should you do?

As you can see above, 10%-20% falls are fairly common. Of course, this is at an index level, and these falls will be much sharper at an individual stock level.

But if you are investing in direct equities, volatility is the price you pay for returns that can be higher than the indices. Single stocks can fall way more than the indices, and all of today’s wealth creators like Infosys, TCS, Kotak & HDFC have routinely fallen more than 30%. But on the other hand, a stock needn’t go up just because it has fallen sharply. For every Infosys that recovered from an 80% fall, there will be 100 other Reliance Power’s that went to zero.

Here’s a stat to give you a sense of how hard it is to pick stocks. According to a study by Hendrik Bessembinder of Arizona State University, from 1926 to 2019, $47 trillion of shareholder wealth was created in the US. Of this, just 83 stocks were responsible for $23 trillion. The remaining $23 trillion was from over 25,500 companies. I came across a presentation of his which found the same in India as well—just 1% of stocks created 83% of the wealth from 1990 to 2018. This is what people mean when they say stock picking is hard. I’m not saying don’t pick stocks, but I’m showing you the odds.

This will end badly. Can I time the market?

“Only two people can buy at the bottom and sell at the top – one is God and the other is a liar.” – Vijay Kedia

If you think that we are heading into a serious crash, you mostly have 3 choices:

- Go to full 100% cash or partial cash

- Tactical allocation

- Do nothing

Assuming that you sell everything and go to 100% cash, you have to be right twice—you have to perfectly time the top and bottom. If you get things wrong, the cost of being wrong can be huge. Just ask all the people who’ve been calling for a market crash in the US since 2010.

We all think we’re geniuses—we are not. But let’s say you did try to time the market, how would that look?

There’s a category of mutual funds called Balanced advantage or Dynamic asset allocation funds. They can invest in equity and debt between 0-100%. They try to deliver equity-like returns with lower volatility by increasing and decreasing equity & debt exposure based on valuations, trends, and other “proprietary in-house” models.

Performance of BAFs and DAFs

Here’s how the funds that existed as of Jan 1st, 2019 performed during the COVID crash. These are new categories, longer and cleaner data isn’t available. I’ve compared them with Nifty 50, which is 100% equity, and DSP Equity and Bond fund, which is a 65% equity & 35% debt aggressive hybrid fund. Of course, this is just one data point, but still, the performance is all over the place.

For all their fanciness, most of these funds don’t deliver. Your odds of picking the good ones in advance are pretty much a coin toss. You would have been better off just having static equity and debt allocation. The world’s most obvious statement: Market timing is hard. Shocking right?.

The only free lunch

Market timing is hard. That leaves us with the next best options—asset allocation and diversification.

“Asset allocation eliminates the need to predict the near-term future direction of the financial markets and eliminates the risk of being in the wrong market at the wrong time.” ― Richard A. Ferri

Asset allocation is how you divide your money between various asset classes—we had written about it here. This means investing in uncorrelated assets classes like domestic and international equities, debt, real estate, and gold. By uncorrelated assets, I mean assets that don’t all move together.

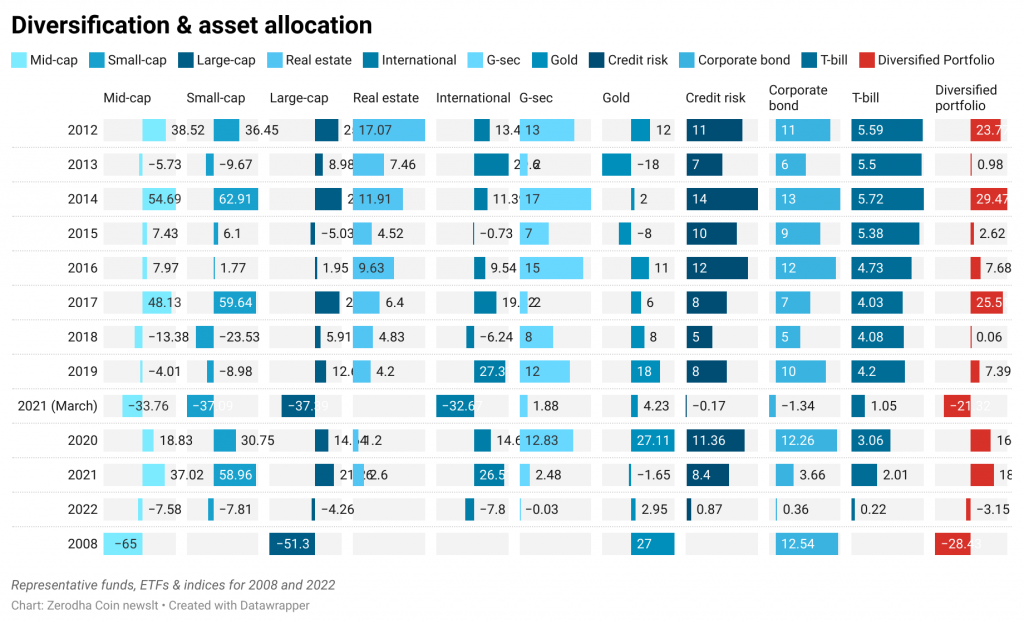

Mint publishes this really nice annual visualization of how various asset classes have performed. I’ve added 2008, 2020 COVID crash, and 2022 YTD returns to it. As you can see, the performance of asset classes varies quite a bit every year. Predicting the best-performing asset class is pretty much a blind guess.

Diversification

But instead of chasing the best performing asset class, what if you held a diversified asset allocation portfolio? The last column is the returns of a hypothetical asset allocation of 60% equity (30/30 large & midcap), 30% corporate bonds, and 10% gold.

You get a solid portfolio and a smoother ride. Even if you check 2008, when the Nifty large and midcap index was down by over 50-60%, the diversified portfolio wouldn’t have fallen as much. You can see the same thing during the COVID crash as well.

“Diversification is protection against ignorance, but if you don’t feel ignorant, the need for it goes down drastically.” —Warren Buffett

True diversification means diversifying across asset classes like stocks, bonds, gold, and inside those asset classes largecaps, midcaps, international equities, govt bonds, corporate bonds, etc. By diversifying, you’re spreading the risks, and this pays off when markets tumble.

Buying 30 different funds randomly isn’t diversification—it’s diworsification. Less the number of funds in your portfolio, the better.

There’s a subtlety to diversification. If everything in your portfolio is going up, that means you probably aren’t diversified well enough. Being truly diversified means that something in your portfolio will suck really badly. That’s the price you pay for lower volatility and lower risk in your portfolio.

To me, diversification is less about returns and more about behaviour since you are spreading your risks across multiple asset classes. This pays off during bear markets when the portfolio tends to fall less. The more volatile an asset class, the higher odds of mistakes because most of us don’t have the ability to stomach a 50% fall.

A diversified strategic portfolio is at all times selling hubris and buying humiliation. It’s not fun while you’re doing it, but it looks great at cycle’s end, when everyone else seems to have been doing the opposite.

The other important thing to remember is that when you check your portfolio and see an underperforming asset class, you’ll be tempted to do all sorts of silly things because losses hurt. This is why it’s really important to think of your investments in terms of your overall portfolio. That’s precisely why diversification sounds nice in theory, but hard in practice. But ultimately, it’ll help you stay the course.

Diversification is insurance against uncertainty, ignorance, and stupidity.

It’s all in your head

“The investor’s chief problem—and his worst enemy—is likely to be himself. In the end, how your investments behave is much less important than how you behave.” — Benjamin Graham

The first stock exchange started about 400 years ago. A lot has changed since then, but human nature has remained the same. We do the same stupid things over and over again. Markets are hard, and they bring out the worst in us. I’m not going to tell you, “don’t get emotional”. That’s the stupidest advice ever. Money and emotions go together, there’s no separating them.

Right now, you might be feeling a little worried―that’s perfectly normal. But worry by logging out of your investing app. Be worried, be emotional—but don’t act on them!

“A mindset that can be paranoid and optimistic at the same time is hard to maintain, because seeing things as black or white takes less effort than accepting nuance. But you need short-term paranoia to keep you alive long enough to exploit long-term optimism. Jesse Livermore figured this out the hard way.” ― Morgan Housel.

I believe more wealth is created by out-behaving than outperforming. By out-behaving I mean, not doing silly things like constantly tinkering with a portfolio, chasing shiny things, and doing the boring things really well like sticking to a plan, keeping a simple portfolio, increasing the savings rate, and rebalancing regularly.

In fact, outperforming is probably way easier than out-behaving because out-behaving is a fight against human nature. Every time your portfolio is in the green, you’re worried that you’ll lose the profits, and every time it’s in the red, you are worried that you’ll lose even more. But out-behaving is in your control, outperforming is not.

This image with 180 human biases is one of my favourite images―not because I remember every bias and constantly live my life analyzing every single decision I make for signs of these biases. Nobody can do that. Even if it were possible, that’s a miserable way to live.

All our biases (open in new tab to enlarge)

I like it because it’s a reminder that we’re full of quirks, and by that, I mean we’re human. It’s kinda stupid how the word “bias” has become such a dirty word. Our biases aren’t flaws, they are evolutionary traits that helped us adapt and survive. But those traits that helped us long ago aren’t suited for investing in today’s world. This is why the whole notion of a “rational investor” is a myth.

As Meir Statman says:

“In standard finance, people are rational. In behavioural finance, people are normal.”

Morgan Housel had written an awesome post a few years ago about Grace Groner and Richard Fuscone. Grace was a simple lady who didn’t marry and worked all her life as a secretary, while Richard was educated at Harvard and was the former vice-chairman of Merrill Lynch Latin America. When Grace died at age 100, she left $7 million to charity while Richard Fuscone filed for personal bankruptcy.

It goes to show the fact that you don’t need a 180 IQ or a Ph.D. to create wealth. You just need to consistently do the ordinary things well to create extraordinary wealth over a long time with a bit of luck, of course. Behaviour matters more than Quant AI/ML strategies.

Being a good investor means having the humility to accept that you are flawed. It’s about building an investment plan to take advantage of our biases and constantly trick ourselves into not doing silly things.

Costly mistakes

Don’t check your portfolio often

If there’s one behavior that seems harmless but can cause the most amount of harm, it’s frequently checking your portfolio. Why? We’re all loss averse―the agony of losses hurt twice as much as the ecstasy from gains. Nobel laureates Richard Thaler, Daniel Kahneman, Alan Schwartz, and Amos Tversky looked at why. They came to the conclusion that it’s because of myopic loss aversion.

It’s a fancy way of saying that people who got more feedback (information) make the most mistakes:

Providing such investors with frequent feedback about their outcomes is likely to encourage their worst tendencies. The subjects in the monthly condition had more information and more freedom than the subjects in the yearly and five-yearly condition, but more is not always better. The subjects with the most data did the worst in terms of money earned, since those with the most frequent data invested the least in stocks (and thus earned the least). This can occur in any domain in which losses are a factor.

In other words, the odds of the market being down are higher on a daily time frame compared to years and decades. We also know that losses hurt twice as much as gains. Loss aversion is a survival mechanism that we evolved to protect ourselves―it helped us avoid predators, conserve food and energy. But, it can hurt us when it comes to investing. The more often you check our portfolio, the more the odds of your portfolio being down. In order to avoid the pain of losing money, you might end up selling something or becoming overly conservative.

The other side of the story is that if you check your portfolio too often, you are more likely to overtrade. You’ll end up losing more money in taxes, transaction costs, and exit loads. It’s good for us because the more you trade, the more brokerage we generate 😅 But we don’t want you to do that, don’t give us your money. Do nothing!

It makes zero sense to check your portfolio 3 times a day if you are investing for 30+ years. Thanks to technology, stock prices, daily NAVs, and live P&Ls, it’s easier than ever to misbehave.

Ignore the news and the noise

Investing is probably the only domain where some ignorance is bliss. Knowing the daily market movements, watching financial news, and reading the latest headlines has zero value unless you are a full-time investor.

“The only function of economic forecasting is to make astrology look respectable.” ― John Kenneth Galbraith

If people could predict stock prices and economies, we would read about them being rich in the news—not them shouting on business news channels 😉 Listening to them is a bit like investing based on astrology.

If you still want to know more about the markets, read some good investing books. We’d suggest Varsity 😉

Use inertia to your advantage

Inertia is a fancy way of saying we’re lazy—we don’t like doing things, and we hate change. While being lazy is bad elsewhere, it can be a good thing in bear markets. Don’t do anything. Automate as much as possible when it comes to investing with SIPs, step-up SIPs, mandates, etc., and go live your life. Just review your portfolio once a year and rebalance it.

Don’t extrapolate the past

“Fear has a far greater grasp on human action than the impressive weight of historical evidence.” — Jeremy Siegel.

Markets rise and fall, and they can fall quite a bit too—this is what you signed up for. Good times don’t last forever, and neither do the bad times—it’s a cycle. So don’t draw conclusions from the past and project them into the future.

{kind=link}

{kind=link}

NiftyBeEs is one of the oldest funds in India―it’s 20 years old. If you had started a SIP at launch, you would’ve generated about 15%. Sounds nice. But you would’ve had to endure a 50% crash, several 20-30% falls, and several years of 0% returns.

Yes, yes, I get the whole past performance is not equal to future, and what if India had become Japan ifs and buts. The point I’m making is that all you can do is control your behaviour and do the basics really well, and let compounding do its job. Your odds of getting rich slowly are far higher than you realize.

What you can control: Invest regularly, increase investments every year, have a sensible asset allocation, and behave well.

What you can’t control: Market direction and India becoming Japan, in which case, everybody is buggered.

Sleep on it

You could read an entire book on bear markets, but you will only know how it feels if you live through one. All the risk tolerances and risk capacities go out of the window. Bear markets are terrible, and they suck. But if you survive a bear market without doing something you’ll regret, you’ll be a better investor than 90% of other investors.

Assuming that markets take a turn for the worse and you’re really anxious about your portfolio, that may be a sign that you are maybe too aggressive. This one’s a little tricky, and there are two ways of thinking about this situation.

- Some people recommend reducing equity allocation by selling equity and rebalancing more into debt.

- Do nothing

If given a choice, I personally prefer doing nothing because we don’t make good decisions when the markets are volatile, even for the right reasons. If at all possible, just ride it out. You can reassess and adjust your portfolio when things are relatively calm.

If you ever feel like tinkering with your portfolio, just sleep on the decision before you do something. The chances are, you’ll realize that whatever you wanted to do would’ve been a mistake.

Investing matters less than you think

In the grand scheme of things, investing is the least important thing in life. Once you have a decent portfolio that allows you to sleep peacefully, it’s just sticking to it. But investors spend every waking hour trying to find new funds and new strategies. Unless you’re a full-time investor, there’s no good reason to constantly waste time on investing.

https://twitter.com/karthikrangappa/status/1484053734338756608?s=20&t=22ONj22CNWnmYXVv5tu39w

Stare at the clouds, watch the grass grow, or watch Netflix—anything is better than obsessing about your portfolio.

Get the basics right

I had written about the basic elements of personal finance a while back. The most important ones:

- Have adequate health and life insurance

- Have an emergency fund

- Save for your retirement

Defense first and then offense. The reason is assuming that you aren’t adequately insured, in the case of an emergency, your investment portfolio becomes your emergency fund. The choice of funds, strategies, etc aren’t all that important as they are made out to be in the grand scheme of things.

Oh, and please don’t stop or pause your SIPs. Don’t use your emergency fund to buy the dip. Just do nothing. Things always seem worse at the moment but if you zoom out the chart of Nifty, you’ll see that the Indian markets always climb the wall of worries. This volatility is the reason why you generate higher returns compared to a fixed deposit.

https://twitter.com/Nithin0dha/status/1486664407920697347?s=20&t=gZ-pGzI-pDt0mU3uT4CFIg

Avoid the saviors

In a bear market, you’ll come across a lot of people who’ll try to peddle you all sorts of products and funds that promise to give equity returns with debt-like volatility. Please don’t fall for them. Most of these products are designed to make money for people selling them, not for you. A sensible asset allocation is the best insurance for all markets.

Good article

Do you send the newsletter through email? I can’t find a way to register it. Or maybe an RSS feed?

Fantastic article 👍

Excellent article giving good advice especially for youngsters

Hey , Nithin reading annual report is a boring thing why don’t zerodha make it short and easily accessible to everyone who doesn’t even know English translate annual report into region language of India it would be great if you do that to bring more quality long investor you done lot of thing related trading please look into about investment and investors..

Well written Bhuvan.

Enjoyed the content and your writing style too.

Please continue to publish more such content.

Best Wishes

Awesome Content. Thanks for sharing this knowledge

Brilliant article and each and every statement is gold!

Very pragmatic and wise article. Asset allocation is the key. Never go overboard on buying the dios, rather stick to the asset allocation. Have a balance of equity, gold, and debt funds. Don’t stop the SIPs. Very well articulated.

Ultimate article by Zerodha . One of the by far best one read till now .

I feel its an Awakening article for every one (for both the Naïve and Experienced0. Thanks Zerodha Team

Thoughts beautiful penned down in a very simple language which a novice can understand. Most of the brokers will never care to comfort you like this. Thanks.

Fantastic 👌

Always a great admirer of Your posts. They are are spiritual and enlightening ❤️

Content like this needs to be appreciated…extremely well written, great references and quite straightforward! Thank you!

Brilliant article.

Great write up and very well narrated…

Well written 🙌

Excellent

Absolutely gem.

Being a new comer to market, after seeing such a deep red today, this is something which made me to sleep better.

I love you team Zerodha.

This article is the best tonic available in this tumultuous time. A soothing balm o. etching nerves .A solid support in bad weather. Thank you for this Gold por of advices

Can’t describe how much i agree with each and every word written in this article. Just wonderful 😁

Fundamentals and principles are presented beautifully in plain vanila language. I have read various indian & international finance, economic, investing articles and books since past years.

Somehow this article put all those essence in a single page

fantastic write up Bhuvan.

Really really enjoyed the writing style, flow of words, light-ness of expression, subtle humor, irreverence. Content, i know and am aware of most of the basics, but really nice to see it brought together at one place; loved the quotes too.

very good writing, (trust me, i read a lot, books, articles; in my view, am qualified to say that, i think).

and so am subscribing to the letter.