2.1 – Warming up to risk

For every rupee of profit made by a trader, there must be a trader losing that rupee. As an extension of this, if a group of traders consistently make money, then there must be another group of traders consistently losing money. Usually, this group making money consistently is small instead of the group of traders who consistently lose money.

The difference between these two groups is their understanding of Risk and their techniques of money management. In his book ‘The Disciplined Trader’, Mark Douglas says successful trading is 80% money management and 20% strategy. I could not agree more.

Money management and associated topics largely involve the assessment of risk. So in this sense, understanding risk and its many forms become essential at this point. For this reason, let us break down the risk to its elementary form to get a better understanding of risk.

The usual layman definition of risk in the stock market context is the ‘probability of losing money. When you transact in the markets, you are exposed to risk, which means you can (possibly) lose money. For example, when you buy a company’s stock, whether you like it or not, you are exposed to risk. Further, at a very high level, risk can be broken down into two types – Systemic Risk and Unsystemic Risk. You are automatically exposed to both these categories of risks when you own a stock.

Think about it, why do you stand to lose money? Or in other words, what can drag the stock price down? Many reasons, as you can imagine, but let me list down a few –

- Deteriorating business prospects

- Declining business margins

- Management misconduct

- Competition eating margins

All these represent a form of risk. In fact, there could be many other similar reasons, and this list can go on. However, if you notice, there is one thing common to all these risks – they are all risks specific to the company. For example, imagine you have an investable capital of Rs.1,00,000/-. You decide to invest this money in HCL Technologies Limited. A few months later, HCL declares that their revenues have declined. Quite obviously, the HCL stock price will also decline. Which means you will lose money on your investment. However, this news will not impact HCL’s competitor’s stock price (Mindtree or Wipro). Likewise, if HCL’s management is guilty of misconduct, then HCL’s stock price will go down and not its competitors. Clearly, these risks are specific to this one company alone and not its peers.

Let me elaborate on this – I’m not sure how many of you were trading the markets when the ‘Satyam scam’ broke out on the morning of 7th January 2009. I certainly was, and I remember the day very well. Satyam Computers Limited had been cooking its books, inflating numbers, mishandling funds, and misleading its investors for many years. The numbers shown were way above the actual myriads of internal party transactions, all these resulting in inflated stock prices. The bubble finally burst when the then Chairman, Mr Ramalinga Raju, made a bold confession of this heinous financial crime via a letter addressed to the investors, stakeholders, clients, employees, and exchanges. You have to give him credit for taking such a huge step; I guess it takes a massive amount of courage to own up to such a crime, especially when you are fully aware of the ensuing consequences.

Anyway, I remember watching this in utter disbelief – Udayan Mukherjee read out this super explosive letter, live on TV, as the stock price dropped like a stone would drop off a cliff. This, for me, was one of the most spine-chilling moments in the market; watch the video here –

I want you to notice a few things in the above video –

- The rate at which the stock price drops (btw, the stock price continued to drop to as low as 8 or 7)

- If you manage to spot the scrolling ticker, notice how the other stocks are NOT reacting to Satyam’s big revelation

- Notice the drop in the indices (Sensex and Nifty); they do not drop as much as Satyam.

The point here is simple – the drop in stock price can be attributed completely to the company’s events unfolding. Other external factors do not have any influence on the price drop. Rather, a better way of placing this would be – at that given point, the drop in stock price can only be attributable to company-specific factors or internal factors. The risk of losing money due to company-specific reasons (or internal reasons) is often termed “Unsystemic Risk”.

Unsystemic risk can be diversified, meaning instead of investing all the money in one company, you can choose to invest in 2-3 different companies (preferably from different sectors). This is called ‘diversification’. When you diversify your investments, unsystemic risk drastically reduces. Going back to the above example, imagine instead of buying HCL for the entire capital, you decide to buy HCL for Rs.50,000/- and maybe Karnataka Bank Limited for the other Rs.50,000/-, in such circumstances, even if HCL stock price declines (owing to the unsystemic risk) the damage is only on half of the investment as the other half is invested in a different company. In fact, instead of just two stocks, you can have a 5 or 10 or maybe 20 stock portfolio. The higher the number of stocks in your portfolio, the higher the diversification, and therefore the lesser the unsystemic risk.

This leads us to a very important question – how many stocks should a good portfolio have so that the unsystemic risk is completely diversified. Research has it that up to 21 stocks in the portfolio will have the required necessary diversification effect and anything beyond 21 stocks may not help much in diversification. I personally own about 15 stocks in my equity portfolio.

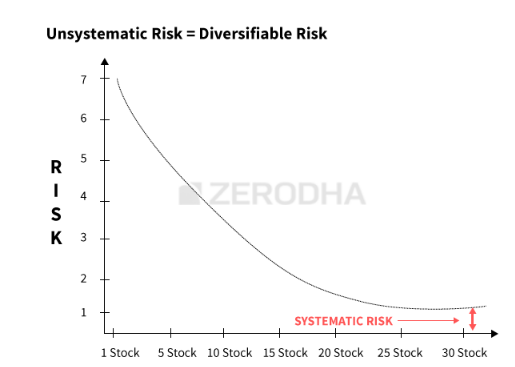

The graph below should give you a fair sense of how diversification works –

As you can notice from the graph above, the unsystemic risk drastically reduces when you diversify and add more stocks. However after about 20 stocks, the unsystemic risk is not really diversifiable, this is evident as the graph starts to flatten out after 20 stocks. In fact, the risk that remains even after diversification is called the “Systemic Risk”.

Systemic risk is the risk that is common to all stocks in the markets. Systemic risk arises from common market factors such as the macroeconomic landscape, political situation, geographical stability, monetary framework etc. A few specific systemic risks which can drag the stock prices down are:–

- De-growth in GDP

- Interest rate tightening

- Inflation

- Fiscal deficit

- Geopolitical risk

The list, as usual, can go on but I suppose you get a fair idea of what constitutes a systemic risk. Systemic risk affects all stocks. Assuming, you have a well diversified 20 stocks portfolio, a de-growth in GDP will indiscriminately affect all the 20 stocks and hence the stock price of stocks across the board will decline. Systemic risk is inherent in the system and it cannot really be diversified. Remember, ‘unsystemic risk’ can be diversified, but the systemic risk cannot be. However, systemic risk can be ‘hedged’. Hedging is a craft, a technique one would use to get rid of the systemic risk. Think of hedging as carrying an umbrella with you on a dark cloudy day. The moment, it starts pouring, you snap your umbrella out and you instantly have a cover on your head.

So when we are talking about hedging, do bear in mind that it is not the same as diversification. Many market participants confuse diversification with hedging. They are two different things. Remember, we diversify to minimize unsystemic risk. We hedge to minimize systemic risk and notice I use the word ‘minimize’ – this is to emphasize that no investment/trade in the market should be ever considered safe in the markets.

Not mine, not yours.

2.2 – Expected Return

We will briefly talk about the concept of ‘Expected Return’ before we go back to the topic of Risk. It is natural for everyone to expect a return on the investments they make. The expected return on investment is quite straight forward – the return you would expect from it. If you invest your money in Infosys and expect to generate a 20% return in one year, then the expected return is just that – 20%.

Why is this important, especially when it sounds like a no-brainer? Well, the ‘expected return’ plays a crucial role in finance. This is the number we plugin for various calculations – be it portfolio optimization or a simple estimation of the equity curve. So in a sense, expecting a realistic return plays a pivotal role in investment management. Anyway, more on this topic as we proceed. For now, let us stick to basics.

With the above example – if you invest Rs.50,000/- in Infy (for a year) and expect a 20% return, then the expected return on your investment is 20%. What if instead, you invest Rs.25,000/- in Infy for an expected return of 20% and Rs.25,000/- in Reliance Industries for an expected return of 15%? – What is the overall expected return here? Is it 20% or 15% or something else?

As you may have guessed, the expected return is neither 20% nor 15%. Since we made investments in 2 stocks, we are dealing with a portfolio, and hence, in this case, the expected return is that of a portfolio and not the individual asset. The expected return of a portfolio can be calculated with the following formula –

E(RP) = W1R1 + W2R2 + W3R3 + ———– + WnRn

Where,

E(RP) = Expected return of the portfolio

W = Weight of investment

R = Expected return of the individual asset

In the above example, the invested is Rs.25,000/- in each, hence the weight is 50% each. Expected return is 20% and 15% across both the investment. Hence –

E(RP) = 50% * 20% + 50% * 15%

= 10% + 7.5%

= 17.5%

While we have used this across two stocks, you can literally apply this concept across any number of assets and asset classes. This is a fairly simple concept, and I hope you’ve had no problem understanding this. Most importantly, you need to understand that the expected return is not a ‘guaranteed’ return; rather it is just a probabilistic expectation of a return on investment. In his paper ‘An introduction to risk and return concepts‘, Franco Modigliani has also explained this in the most defined way possible.

Now that we understand expected returns, we can build on some quantitative concepts like variance and covariance. We will discuss these topics in the next chapter.

Key takeaways from this chapter

- When you buy a stock, you are exposed to unsystemic and systemic risk.

- The unsystemic risk concerning a stock is the risk that exists within the company

- Unsystemic risk affects only the stock and not its peers

- Unsystemic risk can be mitigated by simple diversification

- Systemic risk is the risk prevalent in the system

- Systemic risk is common across all stock

- One can hedge to mitigate systemic risk.

- No hedge is perfect – which means there is always an element of risk present while transacting in markets

- The expected return is the probabilistic expectation of a return

- The expected return is not a guarantee of return

- The portfolio’s expected return can be calculated as – E(RP) = W1R1 + W2R2 + W3R3 + ———– + WnRn

Thank you for all the wonderful resources. You mentioned that having 21 stocks in a portfolio minimizes unsystematic risk and that investing beyond 21 stocks does not offer additional benefits. Could you please tell me the name of the research paper or report that supports this claim?

You can follow the discussion here, there are several links to papers – https://forum.bionicturtle.com/threads/non-systematic-variance.9294/ . I think 20-30 is a good number. Please do let us know if you find any other interesting data around this. I\’m sure the community will benefit.

Hi sir, Can you tell me how the unsystemic risk works when you buy nifty 50 ETF ?

Because there are 50 companies, the risk is diversified across all of them. Diversification is the only way to deal with unsystematic risk.

Hello Kartik, can we measure systematic and unsystematic risk?

You can measure Risk in general and calculate Beta. Beta can be taken as a proxy for market risk.

What about equity risk premium as a measure of expected return please add it.

And also weights of cost of capital as debt and equity components as measure of expected rate of return.

We have covered this in detail in the financial modelling module, request you to please check that.

Systemic risks can be diversified by having different types of asset clauses right!

Yes, thats right. But each asset will also bring its own set of systemic risks.

dear karthik sir i don\’t why i have been neglecting this content these many days.i am feeling so stupid at this point that why i have not did this before a year when i started my journey thank you for this amazing masterpiece i hope many other content will be coming in future on this note i just want to know is knowing buyer and sellers psychology is important if yes how should i learn this are they any course or books(if there are any kindly recommend me some good books) where i can master this.so once again thank you so much

Thanks for the kind words, Abhiskek. I\’m happy you liked the content on Varsity! We have a youtube channel where we put in a lot of content as well. Do check that – https://www.youtube.com/@varsitybyzerodha

Is the graph just for explanation or is it mathematically derived

Sorry, which graph are you referring to?

impressed with the portfolio returns formula. thank you.

Happy learning!

I am both long term invester and short term invester.My long term is up to 5 years and more and short term investment may be from 5 days to 6 months. I want to know about hedging a portfolio of my short time investments.

Check this, Pawan – https://zerodha.com/varsity/chapter/hedging-futures/

Sir,

Can we Hedge our Portfolios by selling calls and going long on Puts?

Like a (Hedging blue chip stocks strategy)

Yeah, you can.

Back to corporate finance 😀😁

Happy learning!

Can you please clarify, if SYSTEMIC RISK and SYSTEMATIC RISK are same or different? Need clarity on both the words.

I have read Mr. Prasanna Chandra\’s book and he has mentioned unique risk as UNSYSTEMATIC RISK which is stock specific risk and market risk as SYSTEMATIC RISK which is attributable to economy-wide factors.

Its what Mr.Prasanna Chandra says, I need to change 🙂

Gem article .Lucid interpretation.

Happy learning!

are these based on CAPM ? if you explain the CAPM with detail it could be better

I\’ll try and explain CAPAM in the financial modelling module.

Very informative. I own 9 stocks with 9-12k investment on single stocks. I wait for 5 % return and then sell. And then I reinvest on another stock. I usually wait until 3 months timeframe for return of 5 %. If the stock in not performing, I square off my position.

I am not sure if my approach is good or not. But if we roll over 5% 3-4 times in a year, I am sure this will yield 15-20% return in my portfolio.

Seems good, Praveen. But you have to back test this and get a sense of how the returns move.

sir, you mentioned about satyam computers, did satyam computers had derivatives? What happened with those? Does exchange closes them? If exchange closes them, how will we come to know about that? just like you mention story of your colleague who made 26lac on budget announcement day in previous module, that day exchange was closed at around 10AM

Yes, Satyam had F&O contracts. It was a free fall, and at that point, there were no execution range or even circuit breakers.

Great piece 👌

Happy learning!

Hi Karthik,

Is it systemic risk or systematic risk.? As I see in Investopedia both are different.

In the fourth chapter beginning, you have mentioned systematic risk whereas in this chapter you have mentioned systemic risk

Its systematic and unsystematic risk 🙂

Sir, I want to be a trader. In that case, the expected return formulae remain the same? Doesn\’t it depend on time? Also, I\’m a beginner here, could you please suggest where can I learn about stop loss and when and how to exit a trade, in varsity?

These topics are scattered across Varsity, but I\’d suggest you read the support and resistance in the Technical analysis module.

Hello Sir,

Is it possible for you to post change logs of chapters you have edited?

For example If I have read through your module after which you have made a change. I\’m not sure what change you have made and it results in me reading the entire chapter again and often I do not even find the change.

Or maybe adjust the changed text in red or something?

Thats a good suggestion, thanks. Will try and do that going forward.

Fantastic content. Thank you!

Happy learning, Abha.

Dear Karthik,

Fantastic work. Greatly appreciated for the informative easy to understand lesson.

Can you please tell me how can I download module 11 & 12 in pdf form as I am unable do so despite several attempts.

Thank you

Varadarajan

No PDF for these modules yet, will try and upload for Module 11, 12 we don\’t intend to publish the PDF.

Great content Karthikji…

Simple and easy to understand explanation of each topic.

I think varsity content is a must read for every beginner and advanced trader/investor.

Zerodha is doing great by providing this content free of cost so that anyone who wants to learn share market can be benefitted.

Keep up the good work…🙂👍

Glad you liked it, Manoj. Happy learning 🙂

the explaination is very good in the book , examples are very very helpfull to understand

Happy learning!

Hi Karthik, great stuff.

You have set a very high benchmark at the Varsity. You make everything sound simple, lucid and understandable.

Just one suggestion. I think the words systematic risk and unsystematic risk should be replaced with systemic risk and non-systemic risk respectively.

Prakash

Thanks, Prakash for pointing this out (and the for the kind words). I will make the change 🙂

Please tell about risk in trade of all kind segment

Have discussed this across multiple chapters in Varsity.

Thanks for your efforts for putting all the topics in interesting and simple manner. I am new to this and your material really teaching me and imparting my confidence.

Happy reading, Surabhi 🙂

Trading in cash segment may not be a zero sum game.

F&O are definitely a zero sum game.

Sort of 🙂

interestingly, i found another one- systemic risk, also not diversifiable; due to big exo- factor eg corona, or very big endogenic factor in a co. too big to fail

Yeah, these are all market risk.

Thank u Sir for ur continuous support.

Plz suggest a list of books for beginners.

I read Rich Dad Poor Dad ( focused on builting asset )

I tried reading The Intelligent Investor. It went bouncer!!! 🙂

Do check out One up on Wall street, its a really nice book.

I wish to place an order to buy some stocks of a company before market opening. Can I do it now in advance? I am new to stock market. Kindly suggest

You can place an AMO order.

I don\’t know…..kite app buying and selling problem

There is no problem, Pravin.

I beg your parden…

Module is excellently written, but kindly replace the word \”Systematic risk\” with \”Systemic risk\”

(Systemic – Embedded within and spread throughout and affecting a whole system, group, body, economy, market, or society.)

Ah, must be an inadvertent mistake, thanks. Will fix it.

did you short the satyam stock, did you make profit

No sir, I dint.

What would happen in case of like satyam scam .

Price was trading 130 after coming this news there is no buyer would we stuck there and wont be able to exit.?? What would happen in that scenario

2 Is that good idea to short a stock whenever kind type of news come

Thats an extreme case, Gautam and the reactions would be too wild. Yes, you will make a profit if you short.

Hello Karthik Sir,

In this para, \”Mark Douglas, in his book ‘The Disciplined Trader’, says successful trading is 80% money management and 20% strategy. \” Why you said this – I could not agree more ?

Thats because great strategies can go kaput when implemented with bad risk management practices. Suggest you read the book \”When the Genius failed\” to understand this better.

Ok, Means successful trading is 80% of money management and 20% strategy only if trader applied best risk mgmt practices along with strategy, it doesn\’t matter whether strategy is best or mediocre .

and thanks for the book recommendation, I will surely do that.

Yes, Sir. What really matters is risk management.

Hello Sir,

why we retail investor are not allowed to see total placed orders for any particular stock ? ( we can see only first 5 placed orders) where we can know actual trend of market.

Do you think big players or operators are playing with poor investors ?

for some shares only buyers are there and not single seller , vise versa only sellers are there and not buyers , getting continuous in upper / lower circuit.

i am sorry if it is not right place to ask this kind of things.

Thanks for your education.

Everyone gets to see the same order book, Nihal i.e the top 5 bid and ask positions. Shares hit circuits because of demand and supply situation.

Great explanation Karthikji. I remember that I had read the systematic & unsystematic in your module on Futures trading too maybe in a Chapter on Hedging. There you had taught us how to hedge our portfolio depending on weightage, against contract value etc using Nifty 50. I learn & make a notes in my own words that is y remembered accurately. Thanks for recalling again & a great chapter again from you 🙂

Thanks for the kind words, Harsh! Happy learning 🙂

i have a trading account of around 10 thousand rupees.. i do mostly day trading and want to generate a return of 0.5% daily on Rs. 10k

Hence, should i divide my account to 20 parts (i.e., Rs. 500 for each trade) and maintain a reward risk ratio of 1:1? However, i am aware that I will have to place atleast 20 trades everyday to generate the 0.5% return on my account value? is this the right way?

This is not the right approach to trading. Its almost impossible to generate 0.5% on a daily basis.

You have mentioned that using **Diversification** we can reduce the un-systematic risk. But as a Swing Trader ( I hope i am going to be 😛 ), how diversification is relevance to me? If i am going to trade on a daily basis and the trading period is within a week, is it practically possible to maintain 15 – 21 positions in the portfolio (Imagining going through nifty50 company charts everyday to maintain a well diversified portfolio for short period stocks looks scarrrrrry)?

Not scary if you can somehow automate your stock selection process. I used to run a swing trading portfolio few years ago – the idea was to select stocks based on momentum and hold for a month. But what helped me was the selection process was programed. I will be discussing this strategy in the Trading system\’s module.

1. Sorry that i could not understand what \”hedging\” really is? It is mentioned that hedging is a craft like carrying umbrella. But in real terms, what is that? Does that mean, i should cancel some of the open positions in my portfolio or ??

2. For the calculation of expected returns, It is mentioned as ,

= 50% * 20% + 50% * 15%

= 10% + 7.5% //////////// step 2

are we missing divide by 100 here? otherwise the step 2 should be ,

= 1000% + 750%

so the formula should be W1R1/100 + W2R2/100 +… +WnRn/100 ?

I\’d suggest you read this chapter to understand all about hedging – https://zerodha.com/varsity/chapter/hedging-futures/

For the expected return of the portfolio- you multiply the investment weight with the expected return of the asset. So if you have invested 50% of your capital in an asset which is expected to return 20%, then the effect on this asset on your overall portfolio is –

50%*20% or 0.5*0.2 =0.1 or 10%.

@trading is 80% money management and 20% strategy,

I think what Mr. Douglas mentioned in that book was, \” I sincerely feel that success in trading is 80 percent psychological

and 20 percent one\’s methodology\”! Isn\’t psychology different from money management??

When pdf file of this chapter will be available?

Before this year ends, for sure.

Sir please see

my knowledge English not

Help varsity Hindi language send my mail

Please please sir

help

Unfortunately, only English for now, Netram. Will try and do Hindi sometime later. Thanks.

CAN I GET A HINDI VERSION OF ABOVE MODULE?

Unfortunately, we don\’t have it at the moment, Anand.

One question about diversification as explained by you and also by some expert that 15 –20 stock is best for portfolio.i have questions after reading this unsystematic risk as if we increase no of investment in more company more than 20 then if case happen like satyam then we can minimize our loss.

Is it correct?

Thanks

Hiran

True, this is where the diversification can help!

sir iam unemployee i did itraday in commodity. i got loss Rs 8000.i did no di any itr till now do i do or not necessary. will i get any scrutiny from it dept ?

Its a good practice to file your returns, even if you\’ve made losses.

U say 21 stock is ideal portfolio , why is this number considered to be apt ??

Above 21, the effect of diversification (and hence the mitigation of systematic risk) is not much, Ankit.

I have this doubt:

Suppose everyone heard about the news and started selling stocks of Satyam.

They who will buy it?

Won\’t be there a stage where no buyers and only sellers?

Happens, this is when the stock hits an upper or lower circuit.

First of all, let me thank you for the wonderful service and education you guys are providing to your customer. Here, I have a small suggestion, if you can put all the varsity content in kindle format that would be really helpful.

Thanks for the kind words, Amresh! That is an interesting suggestion, will try and do that 🙂

Such a great content…….You explain every thing with an example , in a very simple language…..kudos to you……can you write on financial modeling also….I think that can really help us to understand the actual decision on which professional investors invest….thanks

Financial Modelling is a part of the agenda, will try and do that soon.

Dear Karthik, Amazing stuff…. I have read many books written by well known international authors on fundamental and technical analysis, but the way you have explained the trading concepts in your modules with case studies and very simple examples are truly amazing.

Thank you so much for the great work and dedication to help others understand and excel. It is very hard to find people like you in todays world !!!

Thanks for the very kind words, Mohsin. I\’\’m glad that the material helps 🙂

Happy learning.

There is no download link for Module 5 & 9. Please provide it to download PDF file.

Module 9 is work in progress, PDF will be available after that. Module 5, this week.

CARTHICK RUN-GAP@

Bro plz dont be lazy & complete the last Part I mean Trading Strategies and System & plzz add PDF for Trading Psychology and Risk Management.

You are doing great job .

Zerodha is not the place for lazy folks!

Putting up good quality content takes time, bro 🙂

In the risk versus number-of-stocks graph, what is the numerical / mathematical definition of risk? I think for completeness, the definition of risk should be discussed.

Risk, measured in terms of standard deviation represents the average deviation of the stock returns. We has discussed this in detail over the subsequent chapters.

shouldn\’t it be systemic and non-systemic risk instead of systematic and non-systematic?

No, I guess systematic and un systematic.

sir, is it possible to backtest supertrend crossover…. if yes what is the code..? im failing to write the code… i tried ….

Suggest you post this query here – https://tradingqna.com/c/algos-strategies-code

Hi Karthik,

Just a query, as there is way to calculate Expected Return (for Portfolio), is there way to calculate \”Affordable/Bearable Loss\” (depending on the Stop Loss we intend to place for each stock) on the overall portfolio?

What would be change in Expected Return figure arrived at beginning, if say I have made exit after booking loss on some of the stocks in my portfolio?

Thanks & Regards

Santosh S

Value at Risk is the answer 🙂 I\’ll be talking about in the subsequent chapters. Please stay tuned.

Thanks 🙂

Welcome!

sir, YOU and whole ZERODHA team is doing a great job ….which is priceless…. you are spending lot of time to educate others that also for free, and also replying to all the queries just amazing….. Zerodha is like \’BJP\’ , where Nithin is\’Modi\’ and you are \’Arun Jaitley\’……..

im just 20 years of age and i have learnt so much from you about the market…. My Belief in Trading is that \”control yourself, because you cant control the market\”…. You are the best Teacher i have ever seen…. Thank You so much sir……..

Thanks for the kind words, Akash. We are just doing what ours hearts think is right, and hopefully it should have a positive effect on people 🙂

Good luck and continue learning!

Thank you sir….

Welcome!

your client numbers are increasing in a compounding rate… which shows the positive effect….

We are humbled 🙂

Recently I joined ZERODHA , I am not understanding Which Indicators to be added for DAy Trading

Many indicators work. I\’d suggest you start with a simple moving average.

great explanation sir…on that video of satyam scam while stock price falling , 5 points went up in between n held the price for sometimes !! n chart made a pattern too !! who were they buying ? what was their trading psychology….( is it investors/traders who were trying to average ) can u pls reply it gives some ideas…

It was by market participants who did not fully understand the gravity of the gravity of the situation. My guess would be traders playing for short retracement/bounce….trying to take a contrarian call.

thank you…..

Welcome!

hi

when we can expect module 10 trading strategies and system.i am eagerly waiting for it..also please recommend some good books related to it

After the current ongoing module, which is roughly about 3 months from now.

Hi Karthik,

Futures, i am long on a specific stock today of 2000 lot, and stock is trading above resistance and above all moving averages, how the hedging could be done in this case.

Regards,

MSP

Buying an ATM put of the same stock will help.

plzzzzzzzzzzzzzzzzzz

update stretegies section cant wait more..

Which strategies are you referring to?

Sir, in your module on options strategies, you mentioned that there are some 300-400 option strategies in the public domain. Where can I find the complete list? I\’am just curious

They are all scattered around on the internet. Unfortunately, no one has collated them in one single place.

Karthik and team zerodha, you guyz are doing an awesome job putting up the best pieces of information and advice on stock markets. Eagerly waiting for all the next chapters in this and all future modules…. 🙂

Thanks for the kind words, Gurpreet! Will try and put the chapters soon.

Why are you so slow in putting up new lessons? 🙁

And why no pdf of previous module?

:_(

Sorry Maddy, I find it a challenge to structure and simplify content. Hence I tend to take time to put us stuff. Note, these are original content, NONE of the content in Varsity is plagiarized, I can assure you that. There are times when I write stuff, scrap it completely because I\’m not happy with it and I rewrite. Such things consume time.

Will put up the PDFs soon.

I have no words to express my gratitude. The varsity articles are gems, off course.

Can you suggest some book/pdfs esp with trading (no investing) perspective.

Want to learn trading asap

TIA

Have you looked at Steve Nison\’s Japanese Candlestick patters? A good start for a beginner.

We tend to always think that Risk is synonyms with loss/negativity. While in reality we have two sides of the coin – negative risk as you have explained and there is positive risk, and both have different methods of handling, which I am sure you might cover in module further.

Yes, of course. I\’ll try and do that in the subsequent chapters!

Hi Sir

Sir I have general question regarding Risk

I have read some comments on Internet of experts

Some say that selling of OTM call options has least risk if right strike price is chosen

Is it true?

Ankit, to some extent it is true, but not always. Strike selection should be a result of your assessment of market condition.

Please share the list of 15 stocks.

Very nicely defined unsystematic & systematic risk. expecting more topic to be covered in one chapter. eagerly waiting for next chapter.

Will put it up soon.

Excellent explanation.. Thank you.. please make a pdf for this..

Hoping so

Thank you

Yes, it will be ready by next week.

Cude it available in Kannada

Sorry, dint quite get that.