18.1 – All hail the king of Forex

Outside India, the biggest market people trade-in is the Forex futures market. Right from the retail to institutional segment, everybody trades the forex futures markets. If you look at this more closely, you will realize that the biggest currency futures which are traded are –

- Euro against the US Dollar – EUR USD

- GBP against the US Dollar – GBP USD also called ‘The Cable.’

- US Dollar against the Japanese Yen – USD JPY

Till recently, if you wanted to trade any of these international currency pairs, you’d have to open an account with some obscure broker outside India, probably domiciled in Cyprus or Isle of Man, wire funds to the broker’s bank account, and trade based on the rate he relayed. There was no regulatory framework here, which made the whole affair a bit shady.

Now, none of that is required. The National Stock Exchange, under the full regulatory framework, has finally allowed cross-currency futures and options to be traded on the exchanges.

All the above-mentioned currency futures are available to trade on NSE. In this chapter, I’ll try and give you information on how these contracts are structured so that you can trade them effortlessly.

By the way, here is a quick trivia for you – according to BIS survey, about 88% of the International Forex trades happen with USD on one side of which, 50% of the trades are on EUR USD, GBP USD, and USD JPY. So this should give you a sense of how massive these contracts are.

Anyway, let us brush through some basics before we proceed.

When you see a currency pair – say EUR/USD, the first currency is called the Base Currency and the 2nd is called the Quote Currency, and the currency pair is always quoted in the quote currency.

So for example, if you see the price of EUR/USD = 1.23421, then this means 1 EUR is equal to 1.23421 US Dollars.

Have a look at the table below –

| Currency Pair | Base Currency | Quote Currency |

|---|---|---|

| EUR USD | EUR | USD |

| GBP USD | GBP | USD |

| USD JPY | USD | JPY |

Also, here is a typical order book, assume this is for EUR USD,

| Bid Price (price at which you buy) | Ask Price (price at which you sell) |

|---|---|

| 1.2431 | 1.2429 |

| 1.2429 | 1.2427 |

| 1.2425 | 1.2222 |

| 1.2420 | 1.2418 |

| 1.2418 | 1.2416 |

So if you wish to buy the EUR USD, that means you are willing to pay USD 1.2431 for 1 EUR. Likewise, if you want to sell, you are willing to sell 1 EUR to 1.2429 USD.

18.2 – The Futures Contracts

NSE has introduced both futures and options on these international currencies. I think it will be a while for the options will pick up steam; however, I think the near month futures will attract traders on an immediate basis.

The best part is the lot size across all the three currency pairs is fixed to 1000 units of Base currency. Here is how the lot size is fixed –

| Currency Pair | Base Currency | Quote Currency | Lot Size |

|---|---|---|---|

| EUR USD | EUR | USD | 1000 EUR |

| GBP USD | GBP | USD | 1000 GBP |

| USD JPY | USD | JPY | 1000 USD |

The lot size convention is important to remember, and you will understand why a little later.

The tick/pip that will trade on the exchange is 0.0001 for EURUSD/GBPUSD and 0.01 for USDJPY.

There will be 12 monthly contracts available for trading. Near month contracts will expire 2 days before the last trading day of the month.

18.3 A Future Trade

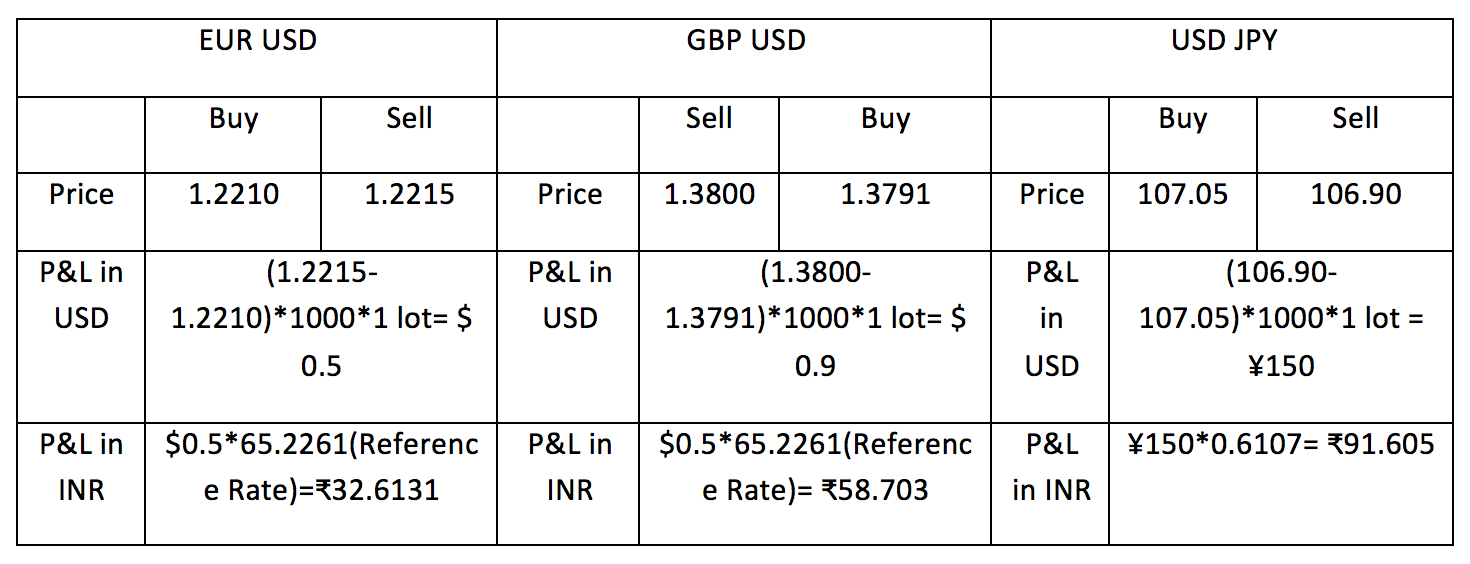

The Profit and Loss for cross-currency contracts will be shown in the quote currency and not in INR like it is for normal equity, commodities and currencies traded in India. Let’s understand this with an example of all the 3 contracts.

The Profit and Loss for the position are converted to the INR using the Reference rate (released by RBI at 12.30 PM) at the end of the trading day. P&L for EURUSD and GBPUSD will be converted using USDINR and USDJPY with JPYINR rate.

For carryforward positions, the daily ‘marked to market’ settlement will be at the daily settlement price (weighted average price of the last half hour of trading)

18.4 The Options Contract

The options contract follow suit to USDINR options, that are already traded on the exchange. Here are the contract specifications.

Option expiry style – European

Premium – Quoted in the quote currency (USD for GBPUSD EURUSD and JPY for USD JPY)

Contract cycle – There will be 3 monthly and 3 quarterly contracts. There will be three continuous monthly contracts, followed by a quarterly contract every 3 months.

Strikes available – 12 In the Money, 12 Out of the Money, and 1 Near the money option. So this is roughly 25 strikes available for you to pick and choose from.

| Underlying | Euro US Dollar | Pound – US Dollar | US Dollar – Japanese Yen |

|---|---|---|---|

| Strike Price Interval | 0.005 | 0.005 | 0.50 |

18.5 Expiry

All near-month contracts will expire 2 days before the last trading day of the month at 12.30 PM and will be settled at the final settlement price.

Let’s look at how the final settlement price is calculated. The cross-currency rate for the pair will be calculated using the reference rate of the individual currency quoted in INR.

| Currency Pair | USDINR | EURINR | GBPINR | JPYINR |

|---|---|---|---|---|

| RBI Reference Rate | 65.2261 | 79.5041 | 89.7055 | 0.6107 |

Futures contracts will be marked to market at the final settlement price, and cash-settled in T+2 days.

The intrinsic value of all in-the-money contracts will be calculated at the final settlement price. Let us understand this with an example.

| Final Settlement Price for GBPUSD | 1.3753 |

| Put Strike Price | 1.3760 |

| Exercise amount per contract(USD) | 0.7 |

| RBI Reference rate for USD at 12.30 PM | 65.2261 |

| Exercise Amount for the contract(INR) | ₹45.65827 |

18.6 Margins

All contracts traded will have an initial margin of 2% of the contract value and an extreme loss margin of 1%. Margin blocked will be in Indian Rupees, but the currencies will be traded in the quote currency (USD or JPY), the margin blocked will be converted to the quote currency. All trades placed before 02:00 PM will block margins as per the previous trading day’s reference rate, and trades placed after 02:00 PM will use the trading day’s reference rate.

18.7 Calendar Spreads

A futures position in one expiry month which is hedged by an offsetting position in a different expiry month is a calendar spread and the same is explained in detail in this chapter. The margins blocked for the spread are fixed by the exchange and are

| Spread duration | Margins |

|---|---|

| 1 month | ₹ 1500 |

| 2 month | ₹ 1800 |

| 3 month | ₹ 2100 |

| 4 month | ₹ 2400 |

Key takeaways from this chapter

- Cross-currency pairs are allowed to trade in NSE for the first time

- Lot size of $1000 for EUR/USD, £1000 GBP/USD and $1,000 for USD/JPY

- The pairs will be traded in quote currency but will be settled in Indian Rupees

- Daily and Final M2M settlement will be based on the RBI reference rates.

- Near month contracts will expire 2 days before the last trading day of the month at 12.30 PM

Will Zerodha Proceed Broking On Precious Metals?

Precious metal = Gold, silver. We already do via MCX.

Hi @Karthik, this is Rangappa from Zerodha. Can we trade cross-currency pairs such as EUR/USD, GBP/USD, USD/JPY, XAU/USD, and USOIL?

No, not available for now. Besides, trading regular USD-INR also needs declaration.

But it is mentioned in Zerodha varsity that cross currency pairs are allowed to trade in NSE.

What is the true picture ?

Also what declaration it required and where?

RBI mandates a declaration now to trade currency Kamlesh.

Kindly arrange a call for me as i am interested forex trading with Zerodha

If you are looking for forex trade with excessive leverage and cross currency trades, then I\’m afraid its not possible with us. You can trade FX that is listed on the exchanges. I\’d suggest you call our support desk for knowing more.

For a option seller, if a OTM put option open (put short/sell) then what happens to the settlement ?

Does it converted to future position?

It expires worthless anyway.

hi , this is the longtime awaited,

need fund swap option between cash and Commodity in Zerodha kite.

kindly conform, when this option is going to enhanced, Investors waiting for the long time!

May I know recent update on Currency trading in India, can normal retailers can trade in currency pair with INR

I guess they can. Nothing changes.

Is Zerodha allowing Cross pairs now ? At least GBP/JPY?

Nope, not yet.

For the past five you are cheating your customers by simply saying that you start cross currency trading soon, which is highly objectionable

Ani, please see the last few comments.

When Zerodha will allow cross currency pairs trading?

Sorry, unfortunately there is no timelines on that.

(in case of currency pairs)What happens if I\’m not able to square-off my future contacts, and they get expired?

If it\’s to be cash settled, then what does the cash settlement means in this case? Do I have to pay/recieved USD(if I take the case of USDINR)?

The contract will be settled by the broker. Yes, it means you pay/receive cash based on the position.

Sir, Which brokers offer Cross Currency trade in India. Is it permitted by RBI ?

The ones listed on NSE is permitted, but not sure which broker provides that.

Hello, I\’m moving back to India very soon. Is trading EurGBP and EURUSD legal in India as of December 2023?

All currency pairs listed on NSE are legal, please do signup with a broker that provides you all the pairs you\’d like to trade.

Is Zerodha Forex trading account can be Login on MT4 Platform?

Nope, that is not related to Zerodha/Kite.

Dear team of zerodha

Cross currency trading available in kite as example eurusd,eurgbp,gbpusd these types,

And how to trade in kite app tell me,

We try to search but not found,

Please help me

We dont have cross currency pairs, Lakshaman.

Hi

Is this still happening. I cannot see cross currency pair?

Has the RBI made it illegal?

Ah no, we don\’t have this yet.

sir ek broker level pe euroinr ki kitni limit hoti hai

Hey can I trade Major currency pairs like USD/JPY etc, on kite or zerodha?

Cross currencies are not yet available on Kite.

Whether cross currency futures trading allowed in zerodha . If yes how do I access them what are pair name or codes used. Give an example for apr 2023 month. Also in case if still not available can you mention when those will be available in zerodha

We dont support that yet, Ganesh.

When will zerodha allow cross currency pair trading…when? When?

No visibility on this yet.

Hi Karthik Sir,

Chapter 18 & Chapter 19, is not added in the downloadable PDF of Module – 8.

Just for your reference.

Would be great if the same is updated to PDF for easy reference.

Let me check this. Thanks for pointing that out.

India tamilnadu

Any chances of getting GBPUSD, EURUSD pairs on Zerodha soon? I heard Angel broking has them

Nope, we dont have cross currency pairs.

Zerosha still resolving issues to start cross-currency trading?

When will cross currency trading will be enabled in our Zerodha?

No specific timeline, Jothi.

Why is currency trading not allowed for non INR currencies? Is there govt restrictions?

No, they are available on NSE to trade.

Still not activated?

No.

Can I join your company to trade mt5

Oh right. I\’m mixing up futures and options here.

Thanks for pointing that out.

Sure. Happy learning!

In section 18.7 about Calendar Spreads, are we assuming that the 2 contracts have the same strikes, i.e., they are purely horizontal spreads and not diagonal?

We are not talking about strikes here, right? These are future contracts.

It\’s been so long but i still can\’t find eur/usd on kite. What\’s wrong?

Anyone from Zerodha team can tell me if cross currency trading started on kite ? If not any tentative timelines ?

No, that dint happen Amit.

Normally What is the spread between USDINR pair in Zerodha?

The spread is on NSE where the paid is traded. The spread is about 10 to 15 paisa, you can check here – https://www.nseindia.com/currency-getquote?symbol=USDINR#inr-contracts

Can I trade cross currencies on kite?

Nope, not available on Kite.

Is ther any trading terminal for forex by zerodha

You can trade INR-denominated pairs on Kite.

Can we trade gold against USD…

That is XAUUSD..??

Not on NSE.

Now a days, I don\’t see EURUSD, USDJPY getting listed in Zerodha? are they stopped?

We never had it on the feeds.

It is already 4 years and still NOT able to trade EURUSD on Zerodha ! Anyone any idea of any Proper broker where I can like hdfcsec or icicidirect ?

Hello Sir, can I trade currency pair on your platform and also is Binary Option (FTT) trading available on your platform?

No, you cant trade Binaries on Kite. But you can trade currencies that are available on the National Stock Exchange.

Seems it\’s not yet, but any idea by when it can be

No timeline yet, Senthil.

Does zerodha allow trading in cross currency ?

Not yet.

Does zerodha allow trading eurusd, gbpusd, usdjpy

Nope, not yet.

When is the FOREX trading likely to start at KITES, we are working on foreign sites, which could by risky in future.

Ashish, you can trade currencies on Kite (USD INR, GBI INR, JPY INR).

why Trailing stop loss feature is removed ? we need it as soon s possible.

When should we expect cross-currency trading to start in Zerodha? Every other broker is providing the currency pairs available for trading. Request you to please start this facility at the earliest. Don\’t want to switch the account.

Ankur, unfortunately we cant put a timeline to this.

Other then INR I can\’t see other combination like eurusd n all

Only INR denominated pairs are available on NSE.

I want to do forex trading but through a regulated broker. Please let us know whether or not Zerodha or any other broker in India, who is approved by SEBI, has introduced trading in cross currency pairs in which trading has been allowed by RBI. Please reply.

These are currencies available for you – https://www1.nseindia.com/live_market/dynaContent/live_watch/curr_der_stock_watch.htm

Hi,

Please check the definition of \’Bid\’ and \’Ask\’ price you mentioned in currency pair in this article in section 18.1. As per my understanding the Bid price is the price at which you sell and ask price is the price at which you buy a currency pair.

Please correct me if I\’m wrong here.

Regards,

Om Dubey

Let me double-check this, Om.

Are the pairs active now? I cant seem to find them.

It is Sept 2021 now.

No, have not updated it. The technique is still valid though.

Give details about USD/INR pair and any other INR related pair

This chapter gives you the necessary details, Vitthal 🙂

Hi Sir,

The charts for forex has very limited data. It does not show Continuous option as well which is there for Nifty and all? The candlestick bars in Daily are till 2020 only? Zerodha does not have ample data for forex?

True, we don\’t have continuous data for currencies. This is on the list of things to do.

Please confirm below pair trading allowed from India?

XAUUSD

GER30

AUDUSD

USD100.spot

No, these are not available.

it is 2021, but i still cant find eurusd on kite

Sir

Please complete your answer sir.

Please tell me the books of segment ipo,currency,earn monthly money on trading like books.

And for long term invest

Sir your guidence in varsity is very heplful sir

Thank you

In today cross currency pairs are available in zerodha. And how we can add symbol in our watchlist. And if I want more cross currency pairs, so which app I want to give oppurtunity to trade. Please tell me sir

And one last question which books I reàd on forex and understanding investings of long term.

Its not available with us yet.

Whether Cross currency trading is available in Zerodha? If yes, how to bring it to watchlist? If no, why it is not included?

No, its not available for now.

Hello Zerodha,

Currently Sharekhan offers EURUSD GBPUSD USDJPY on NSE for Trading. After New SEBI margin rules for Futures and Options, these are the best instruments for traders which requires very low margin, only Rs.2000 to Rs.3000 per Lot. Also there is very good Trading opportunities in these pairs.

Are you planning to help Traders by launching these instruments?

This is on the cards, but will take some time.

Hi!

Thanks for the information. I would like to ask –

Can we trade in GBP/USD from India?

Is it legal to trade from India?

Yes, NSE offers this, although not available with Zerodha.

Please update chapter 18 & 19 in the pdf format as well.

Thank you.

Noted.

Activate forex trading

Can we trade cross currency now in zerodha?

Nope.

Is cross currency trading allowed on zerodha?if not, when this will be allowed?

Not yet, Ashish.

Thank you for the response.

Good luck!

As per the bulletin as of Feb 2018 here (https://zerodha.com/marketintel/bulletin/54184/cross-currency-derivatives), cross currency pairs would be allowed for trading. It is almost close to 3 years now but the pairs are not yet enabled for trading. Could you provide an update on this? Also, for some reason, I am not able to add these pairs to Kite. Please let me know the correct symbols for these pairs on Kite.

These are not enabled on Kite. By the way, there is no liquidity in these contracts.

Has Zerodha started the facility of cross currency trades?

No sir, not yet.

Any updates on cross currency pairing ?

No change yet.

Hello, Can any one explain brokerage & taxes calculations for cross currency. ie Brokerage is fix per lot 10 or 15 Rs

We don\’t have cross-currency as of now, Sanjay

i wish Zerodha also start trading in Cross Currency like Fyers platform.

Hopefully soon.

Has cross currency trading on zerodha started?

Not yet.

Can you recommend any broker in India that allows cross currency

Not sure, maybe you should check Motilal.

What is the position limit of usd/inr pair?

10,00,000 USD I think. Check this – https://www1.nseindia.com/products/content/derivatives/curr_der/position_limits.htm

when can we expect cross currency trading, would it be 24 hrs ?

and is trading forex through online brokers like ig,xm octafx legal in india? if not why rbi/sebi isn\’t taking any actions , how these online forex brokers are structured ? so i have read they operate from cayman islands or some other , so the profits recieved through these brokers is considered illegal ?

hope my questions will be answered

thank you

It wont be 24hrs, since these are offered by the exchanges. All other trading platforms are not legal in India.

What are the position limits?

Limits on on much a trading member is allowed to carry in terms of positions. Check this – https://www1.nseindia.com/products/content/derivatives/equities/position_limits.htm

Any planned timeline for enabling cross-currency pairs in Kite? I have been using Kite for all trading, primarily currency derivatives and had to enroll with another provider, just for the cross-currency part. Almost all other brokers offer this. Any idea by when it would be available?

Unfortunately, no timeline on this Rahul.

Can we open account with international forex broker? Like FBS and other overseas brokers.

Please dont, this is not legal in India.

Can I trade cross currency in Zerodha? If yes, then what will be the timings in which I can trade?

Not yet.

Hello Karthik,

I am fan of you and learnt more about the market through this course and I completed all modules and taken notes of each module.

Then coming to the point :

I have found an inconsistency in your article. Please clarify If my understanding is wrong or You had made a typo.

In the Lesson 2 – \”Reference Rates & Impact of events\” under section 2.1 you have given the following :

\”For example if you want to buy the EUR/USD – you will have to buy the pair at the ‘Ask’ price i.e. 1.1270. When you buy the pair, technically you are long EUR and short USD\”

Here in the above lesson under 18.1, you have given :

\”So if you wish to buy the EUR USD, that means you are willing to pay USD 1.2431 for 1 EUR. Likewise, if you want to sell, you are willing to sell 1 EUR to 1.2429 USD.\”

So if I want to Buy the EURUSD pair, do I need to pay \”Bid\” price or \”Ask\” price ? Please clarify.

I\’m glad you liked the content. Sorry about the confusion. When you buy, you look at the offer price or the ASK price. When you sell, you look at the bid price.

Is cross currency active now on Zerodha?

KINDLY LET ME KNOW TH DUE DATE IF POSSIBLE

No sir, its not.

Sir,

Whether trading in OCTAFX is legal? There are so many videos on youtube saying it is legal to trade in OctaFX because it requires to deposit money in Indian banks. Please clear the doubt

Also is there any LOOPHOLE in the RBI or FEMA regulation so that we can trade-in forex using an international broker as you have

written in the above tutorial that \”if you wanted to trade any of these international currency pairs, you’d have to open an account with some obscure broker outside India, probably domiciled in Cyprus or Isle of Man, wire funds to the broker’s bank account, and trade based on the rate he relayed\”

can you name some of these brokers??

This is not allowed and considered illegal. Best to avoid this, Prabhas.

Sir

I am searching the answer to my question but did not get any satisfying answer, please clear my doubt

My question is

\” Is there any legal way to trade foreign currencies 24*7 using some foreign brokers?? I have seen the RBI regulations, it says margin trading using foreign brokers is not allowed, also we can not deposit money directly or indirectly to their account.

is there any other legal way??

No, it is not permitted in India. You can only trade the frex listed on the Indian exchanges under the CDS segment.

I\’m finding it difficult to understand Bid & Ask, I remember reading it in one of the previous modules but the table of bid & ask in this chapter seems to contradict that information. The bid price is the one that other market participants are willing to buy at, which means I (the seller) will have my sell order easily executed if I sell at those prices. The ask price is the one that other market participants are willing to sell at, which means I (the buyer) will have my buy order easily executed if I buy at those prices.

Please correct me if I\’m wrong.

I\’ve explained that here, check section 9.6 – https://zerodha.com/varsity/chapter/the-trading-terminal/

Is there any realistic timeframe like 1 month, 1 year etc. where we can expect cross currency trading in India?

If you need help with the email alert, I can help you.

Thanks, Jay. Our team is aware of this. We will announce when its done.

Hi

Is cross currency active now on Zerodha?

Also please provide an email alert to comment replies.

Thanks

No, not yet. Email alert may not be possible.

Dear Zerodha

Have you any latest news on when cross currency trading will start on zerodha…everybody asking from 2 yrs…

Any update??

Sorry, I really don\’t have an answer for this at this point.

What if we trade other forex pairs rather than EURUSD, GBPUSD, USDJPY using foreign brokers. Will there be some legal action against the person or not.

You are bound by the RBI\’s LRS scheme. I\’d suggest you avoid using these portals as most of them are quite dodgy.

karthik and his team have been fooling with zerodha\’s clients since the starting of 2018.Zerodha has no plans of letting cross currency pairs to be traded on kite or any platform.

Cross currency pair still not available on zerodha kite ?

When it is expected to be available ?

Unfortunately, we cannot assign any timeline on this. All I can say is that this is on the list of things for us to do.

when we will get the cross currency pairs to trade on zerodha is there any other place to trade cross currency legally in india

Hopefully soon Sir.

I AM NOT ABLE TO SEE ANY CROSS CURRENCY OPTIONS IN MARKET WATCH.. ONLY INR TRADING CURRENCY OPTIONS ARE AVAILABLE IN KITE. CAN YOU PLEASE GUIDE

Cross currency is not yet available on the platform.

Hey…

I cannot find cross currency pairs in zerodha platform ie. Eurusd gbpusd usdjpy.

Are they available for trading or not?

Can you please clear when it will be added…and hopefully we can also trade those pairs.

Thank you

Hitesh

Fyers launched cross currency trading. It\’s true!!

Retail traders are moving to them in hoards those who want currency trading.

Zerodha guys see the competition from Fyers. I say at least now launch cross currency otherwise you will loose big commission income on trades in currency trading. Also reduce kite API fee and divide it into 3 options who wants just API and who wants only streaming data. Or 3rd both API+ Data . So 3 options on kite API side subscription.

Thanks, Saurabh. We are looking into the cross currency bit. Will pass your feedback to the API team.

Any Update? Its 2020.

Much awaited cross currency trading is now available on the discount broker Fyers, when will we get it on Zerodha?????

Any updates on cross currency pair trading?

Nope.

I cant find EURUSD OR GBPUSD OR USDJPY IN marketwatch so how to trade ?

Cross-currency pairs are still not available on the platform yet, Vinay.

If not then what are other platforms we can trade cross currency 24*5 right now?

None in India.

Will we be able to trade cross currency 24*5?? As it is in spot market?

Nope, that not possible.

Knock knock ! just checking out if any progress is at home? 😀

Rahul, no, unfortunately, there is no progress on this 🙁

Hello Karthik Sir,

Sir Earlier Spot Currencies Of EURINR & USDINR Were Available On Pi Application.

But Now, Its Not Showing. How To Trade in Currency Contracts Without Spot Currency Pairs And Their Data?

Please Focus Also On CDS Market. No One Is Taking Seriously To CDS Market.

I\’m not sure if this is true. Currency spot data was not a part of the feeds. Currency trading is purely based on Futures and the associated fundamentals.

@Owes – Don\’t be, good thing takes time. Have some faith in Zerodha!

Humbled 😉

@Karthik – Please tell me cross currency will be active from tomorrow. Nation wants to know 😛

I really wish I could commit a timeline, Rahul. Unfortunately, I cannot.

I m feeling cheated after joining. The cross currencies are listed every where on Zerodha website while it is not available.

Hello team Zerodha it\’s July 2019 when you\’ll start cross currency it\’s been a year now at least provide some progress Info…

Hopefully towards the end of this year.

I hope you read my reply because I\’m deleting your vulgar comment, Uday. Your comment is a reflection of your low life.

If you really want to trade and make money, there are 1000\’s of other instruments to showcase your \’trading skills\’. Try cutting it there and instead of crying about whats not available. A skilled trader needs an instrument which moves and has liquidity and not a platform to crib and cry.

Hi,

When Cross Currency pairs are available for trading… So disappointing. Why it takes one year…

When Currency Spread Contracts are available for trading?

Waiting Waiting Waiting!!!!!

I understand, but unfortunately, it is taking way too long.

why eurusd gbpusd is not avalible to trade in zerodha ?

We have not taken this live for various reasons, Nishant. Hopefully sometime this year. Thanks.

Why does this post even exist if no one can trade cross currency pairs in Zerodha as of yet?

Any timeline for the same?

Rishi, we put this up for educational purpose, but unfortunately, I cannot commit a timeline on this.

Not able to even add cross currency to view rates in kite why???

It is not yet available with us.

Any news regarding cross currency trading?

Nothing yet for now.

Sir, I am unable to open eur usd chart in kite Android app. Please help.

It is not available yet, Sarup.

hi atleast u can add scrips in watchlist would be better ,instead of trading we would test our hypothesis and back test our stratedgies and customize our self ,though i know there are free sources for cross currency charts but i want it in kite ,think about it ,karthik sir

Sheik, thanks for the inputs. I\’ll certainly pass the feedback to our team.

2019 now started. Can we trade in cross currency on Kite now?

I\’m hopeful too.

Enough is enough we r waiting long How long we wait for cross currency .

When will Zerodha Introduce CROSS CURRENCY PAIRS (eurusd, gbpusd…. ) ?

Hopefully next year, Rohit.

Hello Karthik,

First of all, this is so brilliantly simple way of explaining complex various markets instruments. I liked it a lot because like many, I\’m a strong believer of breaking things into SIMPLE…

Could you please add some notes on FX products like FX spot, fwd, swap, NDF and options with examples …

Only if you have time!

Thanks v much…

Thanks, Kalpesh! I\’m really glad you liked the content.

Frankly, I\’ve never traded these products so I\’m not sure how it works, hence I don\’t think I can write about it. Btw, as far as I know, these are institutional products available to banks and other establishments.

Good Morning Sir.

I m using my Demo account on XM Broker . but i don\’t want to open real account in it.

can i open real account in zerodha and trade in eurusd.

We dont offer cross currencies yet.

Are cross currency pair like eurusd valid to trade in our country.

It is available on NSE and you can trade. However, we don\’t have this yet on Zerodha.

Suppose today i bought 1 lot of EURINR at 60.00 and i want keep my stop loss at 59.80 so i place a counter order in amo ie. Sell order with stop loss market order and my triger price is 59.80

Suppose on next day market open gap down at 59.50 in that case will my order will get executed at 59.50 (for sure ) or it will get executed at lower than that .

Yes, since this is SL-M, the order will get executed at 59.5.

How would the brokerage on cross currency pairs, be charged?

It will be Rs.20/- per executed trade. Check this – https://zerodha.com/charges

Even small brokers like 5paisa has cross currency trading. Feels strange zerodha is still working on it.

HDFC SEC and other brokers have already started cross currency a long time back….. 8 months waiting for Zerodha to start is not acceptable…..no matter what the reason is for the delay. If you guys arein the top 3 brokers in the country…..pls live up to the expectations ?

All I can say is that we are working on it, Gerard.

Karthik, would have appreciated if you would have replied with a timeline. But, I guess its not in your control to give me an answer.

Can Nithin help?

Glad you understand, Gerard. Thanks. We are dependent on exchanges for few answers, so it\’s beyond anybody\’s help.

Karthik, this one is out of topic. How do get volume profile incorporated on the PI platform. Kite has it……but trading on PI is a better experience overall. Can you help pls?

Hi sir ,

still cross currency not added in kite.

I understand since it is newly introduced ,u may have to test and backtest for our efficiency

I only wish to know rough estimate still how many weeks it may take ,I heard some rumours that u will introduce on november or on diwali

There are lots of bug fixes here. Without clarity on the issues, releasing the product can be a problem for both you and us 😉

cant find scrip in search ,cross currency pairs ,what will be the problem

Maybe you are searching for it the wrong way. Can you please call the support desk?

sir, any person can trade in forex market

please provide forex broker list so that i can start trading in forex market

You can trade forex (on NSE) with Zerodha.

Hi Team , Karthik

Well I did not want to promote any broker on this platform but since we are speaking about this subject ,good to know information Zerodha needs to know about its competitors –

1-Discounted broker offering cross currency pair trading – Samco , I have been placing trades with them ,since Zerodha does not offer the same

2- Non discounted Brokers offering the plaform = Karvy , Motilal Oswal

Thanks Jay. Like I\’ve said earlier, we are working on this, hopefully, we should be able to offer this to clients really soon.

Hi , I was informed by the zeroda call center agent on calling this no – 08049132020 . ( I got this number from zeroda website )

that cross currency pair trading has started on Zerodha ,I asked the agent 2 times and she replied and assured yes it has started , however after I opened ac online I was informed , cross currency pair has still not started for trading .The zeroda employee that contacted me from Andheri office Mumbai told me cross currency trading will begin from November , Can I please get a true picture for the same , as the only reason I opened ac with zeroda is to trade cross currency pair . Also as the agent LIED AND gave incorrect information to me or provided me incorrect info , now due to No Access to cross currency trading I would like to close the account ,Please Assist , as I was misold , also how can I get refund of charges paid while account open

Sorry to hear this, Jay. I\’m checking on this. But yes, we are not yet live on cross currency, hopefully soon.

Like in Markets – Someone\’s Loss is Another\’s Gain

Likewise clients unable to trade on Zerodha platform for cross currency pairs are migrating to another discounted brokerage firm offering to trade on cross currency pairs , Clients cannot keep waiting missing on trading opportunites due to Zerodha\’s delayed launch .

I understand, Jay. As far I know there is no other broker offering this yet, mainly with the issue related to P&L. We are talking to exchange to get this cleared. Thanks.

you have false information. i know many brokers who are providing trading in cross currency pairs.

I\’m sure, Atul. I\’m not disputing this.

Hi Jay,

Apologies for the inconvenience caused, can you please provide us your client id.

from where i can check RBI reference rate..and same is updated on site….

Check on the RBI\’s website, its available on their homepage.

thanx kartik for info but i am facing difficulty while calculating the settlement price

like on 04/09/2018 i have short on contract on EURUSD FUT 26SEP 18 and kept open on next day (05/09/2018 ) my opening price reflecting as 83 and at EOD again settlement price reflect as 83.54 ….on nse site prev close reflecting as 1.1643

Can u please tell me how the closing/settlement price derived or check post closing and opening market

It gets a little tricky with Cross Currency Raj, you will have to take the change in EUR USD plus the change in the reference rate of USD INR.

Is possible to trade on currency pairs for 24 hours or only in indian trading time

No, this is not possible.

Can you suggest me some good of shore brokers for cross currency trading please??

Unfortunately, I\’m not aware of any, Raj.

Hi Karthik ,

What will be the brokerage charges for USDINR & also for cross currency in futures

It is 20. Check all our charges here – https://zerodha.com/charges

Your intention is very clear Never

When Cross Currency Trading will be available? We have been hearing it from April 2018 that it will be available in Zerodha soon. Is there any specific date or time period?

Never will be start

Kamlesh, the intention is to offer it as soon as possible to clients. I hope you trust us that we are doing our best in this regard. Thanks.

P&l=((order close price-order open price)/ticksize)*lotsize*no.of .Lots

Is it correct

No, its the difference the price at which you buy and sell multiplied by the number of shares (or lot size).

u should start as early as cross currency future. all broker provide this service even small ticket broker also prois vide.

zerodha is now in top 10 but still in zerodha we unable to trade in cross currency.

We are working on it, Nilesh. Hopefully soon.

There is cross currency pairs traded in zerodha even though it has been launched officially in Feb. Support tem always reply by saying they are working on it

Soon, Varun.

Sir,is it worth trading in usd/inr pair??

Yes, why not. As long as you know how to set up the trades. Good luck.

Hello,

Order Window : –

Default qty which pops up in the order window is 1, is it the lot size of 1000? or do I need to input 1000 in the qty field ?

Margin:-

So total of 3% (2+1) of Margin of the contract value will be blocked in USD value and converted to INR as per RBI 12.pm daily rate?

For eg – If I buy 1 contract – EUR/ USD -> 1.1664 * 1000 = 1166 *3% = 35 USD (rounded off 34.98)

35 USD * 68 ( for eg RBI rate @ 12 pm) = 2,380 INR

So more or less this is how the base of margin calculation would be?

If you could have given an example with screenshot in your tutorial would have helped.

For CDS contracts, 1 quantity by default means 1000 quantity(1 lot). So you don\’t need to multiply by 1000.

Your margin calculation is pretty much correct. Accurate margin requirement are updated on the Margin Calculator page daily

@ Zerodha

My earlier perception was that you guys were really committed towards providing best customer services, something which hardly any Indian company provides. I don\’t know how other brokers are doing but that\’s not what I see when I deal with you.

After trading with Zerodha for almost a year now, the perception has completely reversed. Zerodha is no different from other companies and don\’t have a strict adherence to timelines. Copy-paste replies have become so common. Email replies are completely void of any depth, clarification, or smartness. They also seem to be content with their own relative comparison to other brokers in which they are doing the best to provide good service to their clients apparently.

These instances changed my view on their customer service:

1) Crux – roll-out assurances being given for almost a year now and yet every time you speak to them, they will say that it\’s gonna be rolled out soon, probably by end of this week. Never a definitive timeline or any official announcement comes out.

2) Cross-Currency Trading – Evident above that they have maintained the same reply of \”very soon\” for last 3 months

Common zerodha, you can do better!

Harsh, I understand your concerns. Trust me we are working towards delivery of everything promised. It\’s just that the scale we are in, things get highly complex and things take time. I\’m hoping you will continue your support and many thanks for your patience.

Hi Karthik,

Exchange launched on Feb 27, Zerodha has enough time to launch cross currency pairs.

you guys are outstanding in term of technology implementation to trading platform

not understand its taking more than 4 month to add cross currency scripts

There are few vendor dependencies here, Varun. Hopefully soon is all I can say. Thanks for understanding.

i want to trad in future currency .whatb is the minimum amount to open account?….

Anand, we charge 400 for Trading and Demat account. You can open the account online here – https://zerodha.com/?ref=varsity

why zerodha is not starting eurusd trading….its been more than 3 months…only assurances very soon very soon

Uday, this is on the agenda. Thanks for your co operation.

why less volumes are traded in cross currency compare to INR pairs

Not much liquidity, Manoj.

Any update of cross currency trading availability?

No visibility yet, Vijay.

Come on Zerodha, please start trading in cross currency pairs as soon as possible. The volume in EURUSD is good for trading.

Very very soon, Ashwin.

can u tell us when approximately cross currency trading will be possible?

No timelines yet, Prashant.

is only zerodha not allowing customers to trade cross currecny ?? any other broker has strated it or not??

I\’m not sure about other brokers, Prashant.

Motilal Oswal and karvy are havin options to trade cross currency

We will also have soon, Jay.

All my orders related to EURUSD are getting rejected. They are showing error message of \’RMS:Blocked for EURUSD FUTCUR EQUITY cde_fo Remarks: Blocked for Trading block type: ALL\’. What does it mean ?

Thank you,

Ashwin, you need to ensure that your account is enabled for Currencies. Can you call support for this? Thanks.

I am able to trade other currency pair futures such as USDINR, EURINR , etc . It is showing only on cross currency pairs.

Cross currency will take a bit of time, Ashwin.

Can I expect that Zerodha will start trading in cross currency pairs within 2-3 months or it is going to take much more time ?

I cannot comment on the timeline, Ashwin. But please be assured, we are working on it to make it happen soon. Thanks.

Zerodha never start Cross Currency trading

Soon, Mithun. Thanks for your cooperation and patience.

When zerodha going to allow trading in these very liquid pairs?? Could you explain why it is not being available for traders?

Liquidity is the problem with the whole market, and not broker specific.

Sir, can i trade online on spot ,in cross currencies. I don\’t want to do a future trading in currency market.

No, this is not possible, Jay.

Your company only profiting but not customer. Every thing is imagine creature. Price for Pi software, Price for account opening, price for every thing but not profited. Software also worst. I paid brokerage, you should provide everything but . I am not satisfied.

Sir, for you to profit or not really depends on how you trade.

If Base currency is improving then price of pair will go down ?

USDINR = x if USD is becoming stronger then ? If INR is improving then ?

Similarly for cross currency pair how movement takes place ?

Its explained here – https://zerodha.com/varsity/chapter/the-usd-inr-pair/

Hi karthik,

Taxation part looks quite outdated now, needs update now.

Will look into this. Thanks for pointing.

what books do you recommend for a beginning traders..

do you think an average trader can achieve financial freedom over a long term…

please advise only if you have time…or else no hard feelings….

Try and get hold of Alaxender Elder;s \’Trading for a living\’ book. An average trader cannot achieve financial freedom by trading, at the most he will entertain himself by placing few trades here and there. You need to go beyond this. One needs to elevate himself and achieve a higher degree of understanding of markets. This happens by constantly learning and practicing what you\’ve learned.

Good luck.

Thanks for your valuable advice…..

Good luck, Mohamed!

Yes Yes Yes. So true. It needs a vast amount of knowledge and patience. Making profit will just be a matter of time then.

Besides, I love this article.

https://www.moneycontrol.com/news/business/are-you-a-day-trader-if-yes-here-are-top-7-factors-to-consider-for-wealth-creation-2539783.html

Glad you liked the article, Arijit 🙂

Has zerodha allowed trading in cross currency, because my orders are being rejected.

No, not yet.

Good Morning karthik sir..,

how long will it take zerodha to allow cross currency trading..??

Hopefully soon, Mohamed.

When will enable cross currency trading in our Zerodha?

Unfortunately, I cannot give a timeline for this. I\’m hopeful this will happen sometime soon.

Hopefully Zerodha will allow trading in Gold Option & Cross Currency after their client leaving from him.

Thanks for the nice article.

Where to get previous EUR/USD chart data on Kite. for TA ?

On Kite, chart data for cross- currencies is only available from 27 Feb 2018(launch of cross-currency trading).

For TA(if you need chart data older than 27 Feb), I would recommend you use international forex charts that are freely available.

Thanks Faisal.

One more thing, currently I am checking realtime EUR/USD data on tradingview site. But when I compare the EUR/USD rate on tradingview to Kite, I can see some differences. There are 6 digits in trading view as compare to kite which have 5 digits price.

Moreover, there is approx. 6 pips difference between tradingview & Kite price, is it because on tradingview the chart is spot & on Kite the price is future ?

Please help here.

These are few arbitrage opportunities and I\’m guessing they will go away when liquidity picks up in the Indian Markets. Also, a large part of this can be attributed to the involvement of RBI\’s reference rate.

Its almost 8 months now….and Zerodha is yet to start the cross currency trading???? Does it take so long to do testing….. No one in Zerodha has got a clue as to when it is going to start. Hopefully, Nithin Kamat may know.

I understand. All I can say is that there are few complexities involved which we are trying to sort out. We will put this up only after these things are sorted, else it will be a problem for both you and us.