Small and Medium REITs Explained: A New Investment Option for Indian Investors

SEBI’s recent regulations on small and medium REITs (SM REITs) have sparked interest among investors who are eager to explore new avenues for real estate investment. After all, real estate is one of the favourite asset classes for Indians.

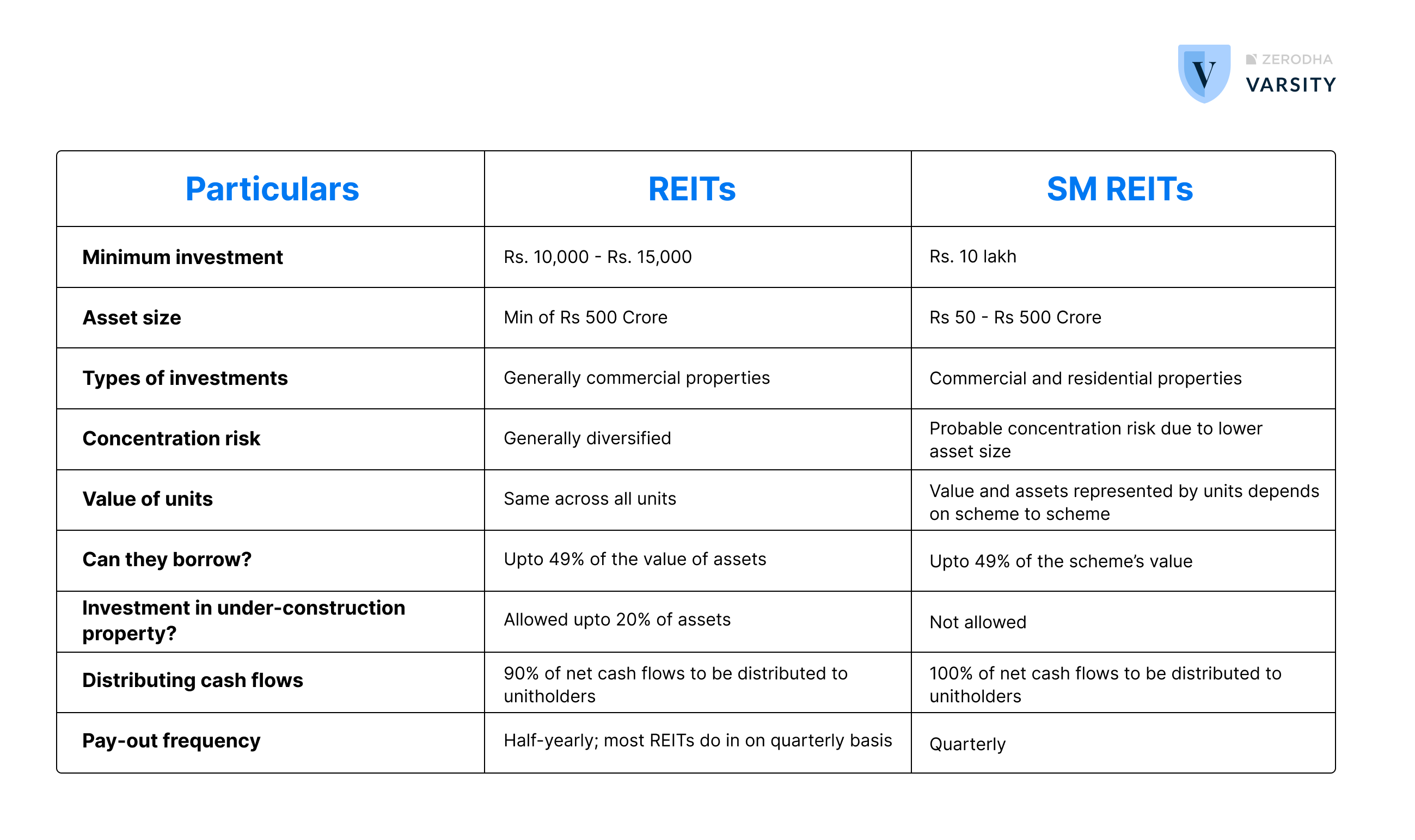

SM REIT (real estate investment trusts) is simply a younger version of the traditional REIT we see in the market now.

For starters, REITs own a pool of real estate properties. They collect rental income from these properties and distribute it to investors as dividends. Whenever there is capital appreciation on the properties, the value of your investment goes up. It’s a way for people to invest in real estate without buying or managing properties themselves.

To learn more about how REITs work, watch it here in English and in Hindi.

In this article, let us see how SM REITs differ from existing REITs.

Understanding SM REITs

Type of investments: While traditional REITs primarily focus on commercial properties, SM REITs apparently have the flexibility to invest in both commercial and residential real estate properties. The number and value of properties that SM REITs invest in could be much lower than what traditional REITs invest in. Hence, there is a scope for more concentrated bets under SM REITs.

Talking about investments in residential properties, in India, the yield on such properties has been currently at 2%-3% per annum on average. We must wait and see if SM REITs with such low yields will take off. Further, how the demand from SM REITs would impact the housing prices will be an interesting aspect to watch out for.

Due to the nature of investments, the regulator wants only investors with a high-risk appetite to invest in SM REITs by fixing the minimum investment amount at Rs 10 lakh. On the other hand, the minimum investment amount in the existing REITs is Rs 10,000 to Rs 15,000.

Various investment schemes: An SM REIT could divide its entire portfolio into various schemes, each investing in different types of properties. So, the unit you hold in one scheme and the unit I hold in a different scheme of the same SM REIT could represent different assets. This is not the case with existing REITs offering uniform value across all units.

Regulating fractional ownership platforms: SEBI’s regulations also address the growing popularity of fractional ownership platforms in the market. Many fractional ownership players and platforms are registered or unregistered in the market today. They divide the property value into multiple shares/units, each at a fractional cost of the entire property value. While these platforms enable easy access to real estate investments, they often lack regulation and pose challenges for investors. By formalizing such structures under SM REIT regulations, SEBI aims to enhance investor trust and ensure they are under regulatory oversight.

The current fractional ownership platforms are asked to be listed within six months from the time of the introduction of the regulations.

SM REIT’s Structure

“Never invest in a business you cannot understand,” said Warren Buffett, referring to stock market investing. Similarly, it is equally important to understand how an asset class works before putting money in it. Here’s the step-by-step procedure on how the SM REIT works –

- Registration first: The SM REIT needs to be registered with SEBI.

- Pooling resources: Investors like you and me invest money in SM REIT, receiving units in return. The SM REIT can also borrow money (debt) up to a maximum of 49% of the scheme’s value.

- Transfer to SPV: The pooled funds are then transferred by the SM REIT to a special purpose vehicle (SPV). Think of this as a separate entity holding the actual properties.

- Buying properties: The SPV must invest at least 95% of its assets in completed and revenue-generating real estate projects. They are not allowed to invest in under-construction properties, which are considered risky.

- Rental Income: The SPV collects money from rent or property sales.

- Distributing income: The SPV distributes at least 95% of the cash flows back to the SM REIT.

- Pay-out time: The SM REIT has to distribute 100% of the remaining net cash flow to unitholders every quarter.

Risks

Here are some of the key risks of investing in SM REITs or with any REIT in general –

Concentration Risk

SM REITs invest in a single property or a small portfolio, making them easier to analyze. But it comes with higher concentration risks. Unlike traditional REITs, there’s less diversification across geographies and properties.

Low Occupancy Risk

REITs’ revenues rely heavily on rental income. Low occupancy rates pose a serious risk, impacting cashflows. Before investing, check current occupancy rate, projections, & past data. A single vacant property in SM REITs could hugely hit revenues.

Tenant Risk

What if the tenant defaults or terminates early? SM REITs may depend on one or a few tenants for revenue. Assess the tenant’s financial health, the sector they operate in, and future outlook. Extended vacancies mean lost income and frequent renewals.

Valuation Risk

Check if the price you pay aligns with the NAV (net asset value) of the underlying properties. REITs disclose the NAV of a unit, calculated using an external valuation report. Higher valuations can impact your returns. So, check the credibility of the valuer.

No Track Record

SM REITs are new in India and have no track record for studying long-term performance or risks. Without past data, investors must exercise extra caution. Also, they might not suit all portfolios—invest only if you have the risk appetite.

Disclosures

Basic conditions for small and medium REITs (SM REITs) include assets ranging from a minimum of Rs 50 crore to less than Rs 500 crore and 200 unitholders.

When it comes to disclosures, the offer document must reveal details of the properties about to be purchased and expected lease rental income for each property along with comparable lease rental income of other similar properties. The net asset value (NAV) of the scheme must also be disclosed by exchanges based on the latest valuation report as of March 31st; NAV represents the estimated market value of all assets held by the scheme.

The regulator also mandated mandatory holding of units to ensure that the SM REITs’ interests align with the unitholders. This is what is referred to as ‘skin in the game’. The SM REIT must hold 5% of the units for the first five years; if debt is involved, it must hold 15% of the units. These limits decrease gradually after the fifth year, and after the 12th year, SM REITs are only required to hold 1% of the units. Similar ‘skin in the game provisions’ also apply to regular REITs.

Final word

SM REITs will be a new investment avenue available for Indian investors soon. As of today, no SM REITs are listed on the exchange yet.

However, when it does, investors have to pay caution. Being a new investment class, its nitty-gritty will be known only after we see it in its full form. The flexibility to invest in lower-yielding residential properties and to borrow (up to 49% of the scheme’s value) make them a risky asset class. Thus, you must ensure it matches your risk appetite, especially with a high minimum investment of Rs 10 lakh and initial low trading activity that could impact liquidity.

The mandated disclosures that include offer documents with details of properties to be invested in, expected yields with comparative analysis, and periodic Net Asset Value (NAV) updates could come in handy during your analysis.

As we conclude this article, never forget Warren Buffett’s two rules of investment – Rule no 1: Don’t lose money; Rule no 2: Never forget rule number 1.

I am interested in investing in Commercial Real Estate

Are the SM REITs can Invest in Hotel property as well ?

Thank you for sharing the details. Eagerly waiting to see when it would get listed and how it performs in Indian market.

Thank you maam for covering Under rated topics