Same-Weekday Momentum

The paper Da, Zhi and Zhang, Xiao, Same-Weekday Momentum (SSRN) first came out on March 14, 2024 and has raked up quite a bit of interest since then. The authors present an effect where if you formed momentum portfolios by weekday, you end up with better returns than traditional momentum.

For example, to build Monday’s portfolio, you rank stocks based on their Monday returns over the last 12 months. You buy this portfolio on Friday’s close and exit on Monday at the close, simultaneously entering Tuesday’s portfolio. And so on.

If the churn sounds like it will be too high, rest assured that it is. However, the returns make up for it.

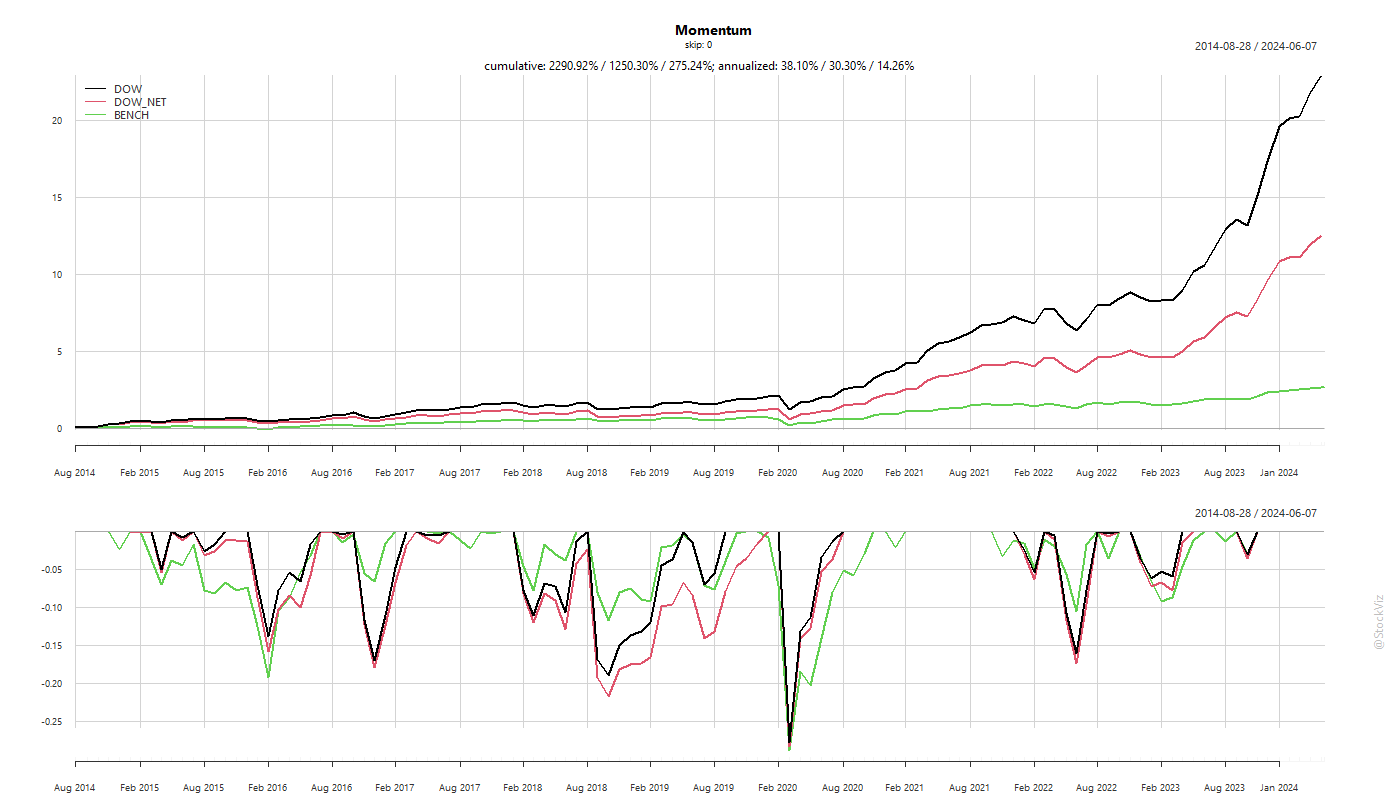

If you assume a drag of 0.5%, consider only the top 200 stocks by free float market cap, and do not have a skip month, here’s Day-Of-Week momentum vs. traditional (“Naive”) momentum:

To see how much the 0.5% impacts performance, here’s the net vs. gross returns:

Benchmark: Nifty 200 TRI

The authors attribute this effect to seasonality in both flows and trading activity of institutions.

Both seasonal flows and seasonal trading are persistent. In other words, if a mutual fund experienced significantly more (absolute) flow on Mondays in the past one year, it’s more likely to experience more (absolute) flow on Mondays in the next month as well. Similarly, if an institution traded more on Mondays in the past, it trades more on Mondays in the future. Moreover, the directions of both seasonal flow and seasonal trading are persistent as well. If a fund experienced more inflow (outflow) on Mondays in the past, it is more likely to experience inflow (outflow) on Mondays in the future. Consistent with the flow persistence, if an institution bought (sold) stocks on Mondays in the past, it is also more likely to buy (sell) stocks on Mondays in the future.

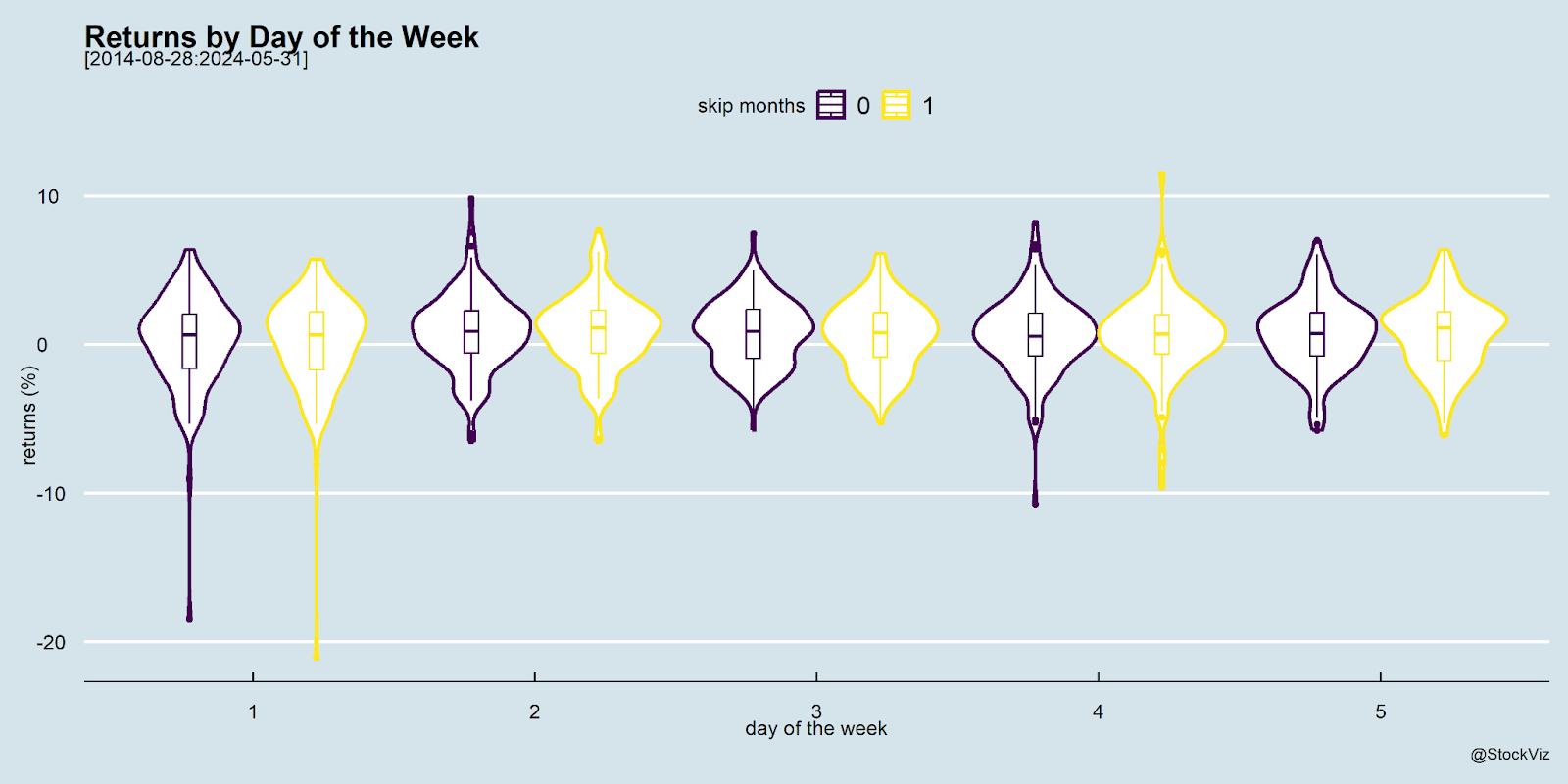

Here’s a plot of returns by day of the week:

Monday’s tend to be a bit volatile, but on average, returns are positive, and there are no huge outliers. Also, not using a skip month gets you better returns than using one.

Does DOW beat NAIVE by a factor large enough to make it worth your while? How far into the future can one expect this anomaly to hold? Well, that is for you to decide.

For those of you who know R and want to play around with the code, there’s something for you on github.