RBI: Putting the Ex in Forex

Through a recent circular, the RBI pulled the plug on speculative forex derivative trades in India.

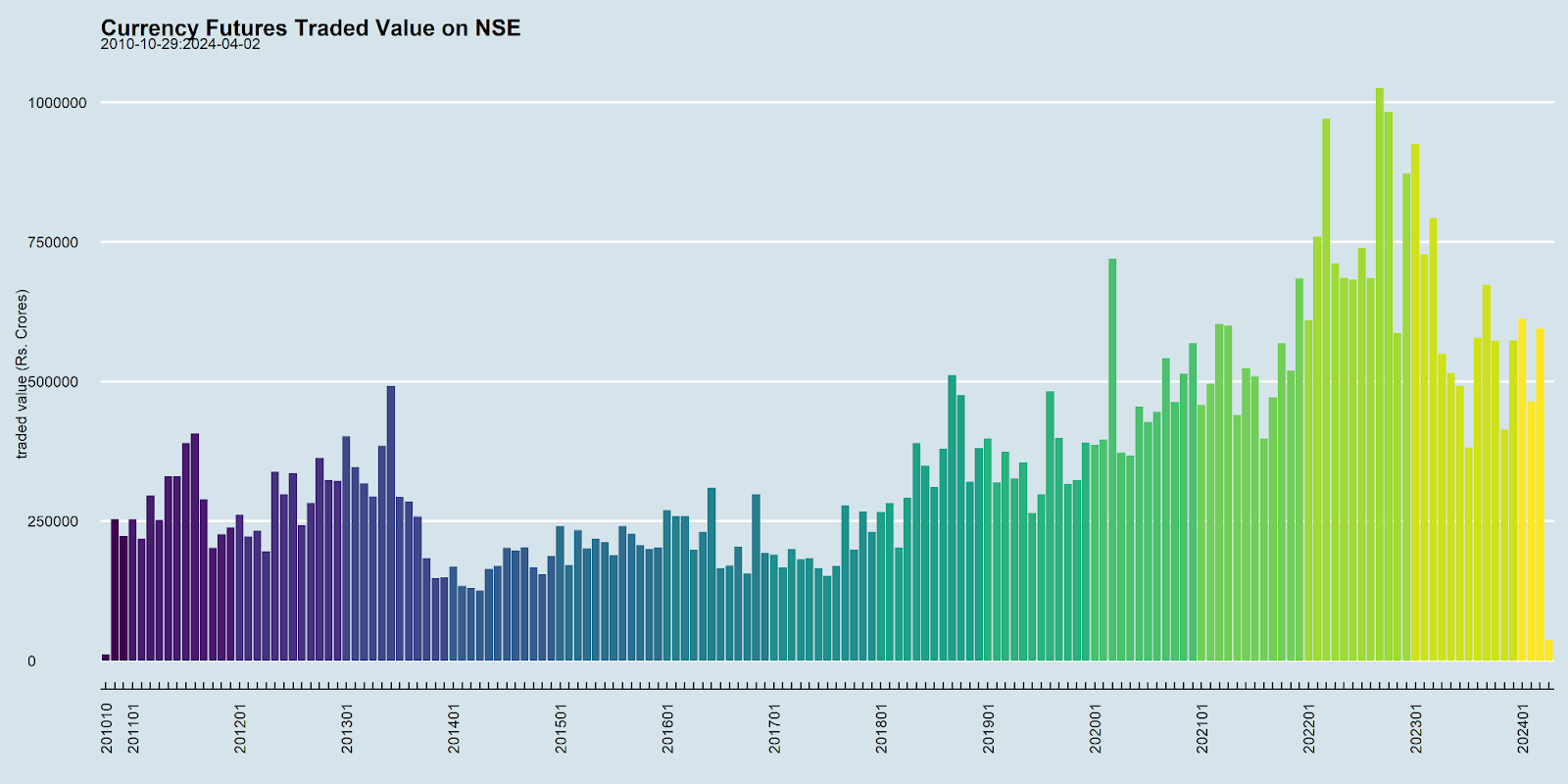

Until now, any speculator could trade currency derivatives on a stock exchange. This is because disclosing an underlying exposure was not required up to a certain limit. Therefore, currency derivative volumes on the NSE were booming. The prices and costs were transparent and provided a direct way to express an opinion on the Indian rupee.

Not so anymore.

The RBI sent out a circular, Risk Management and Inter-Bank Dealings – Hedging of foreign exchange risk (RBI/2023-24/108 A. P. (DIR Series) Circular No. 13), asking exchanges to ensure that those trading in trade INR currency pairs (USDINR, EURINR, etc.) must have an underlying economic exposure to the corresponding currency.

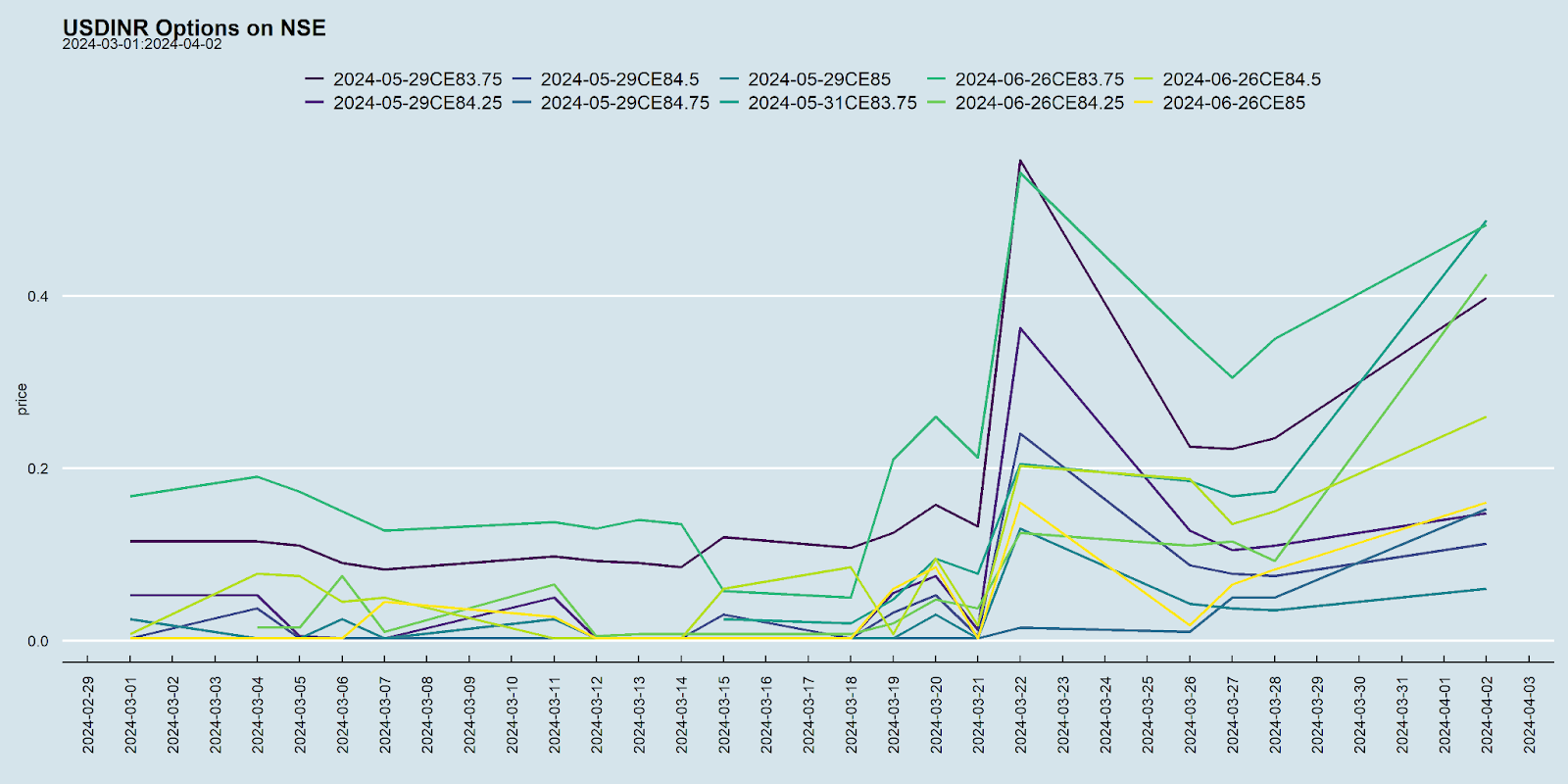

With the RBI actively intervening in the markets over the last few years, the market had gotten used to a low-volatility regime. Most traders were short volatility. The news of this circular rippled through the markets as exchanges directed their brokers to stop clients from opening new positions, and traders rushed to close out their positions, spiking implied volatility.

But is there any issue if the speculators were to vanish? Aren’t derivatives supposed to be used only for hedging?

The challenge is to get a counterparty to your trade at the same time and at a fair price. A hedger looking to sell USDINR might not find a natural buyer at a fair price. And vice versa. So far, this gap was filled by speculators.

Now, with the speculators out of the picture, a hedger is left with only one counterparty: banks.

Besides, now price discovery of the Indian rupee will shift to other venues like Dubai’s DGCX and Singapore’s SGX. Large corporations and HNIs will likely shift their activities away from India. The smaller players will be left at the mercy of Indian banks.

In fact, in 2019, the RBI wanted a “deep and liquid on-shore foreign exchange market that acts as a price setter globally.” They even wanted NRIs to move to the domestic market gradually. Now, even if the circular is rolled back, it might take a while to revive confidence and volumes.

The bond and commodity markets will also see spillover effects.

- For example, most commodities are priced in dollars. A commodity trader not wanting to take the implicit currency exposure might want to hedge it away in the currency market.

- The value of Indian bonds is also derived relative to other bonds in the market. This, too, comes with an implicit currency exposure that bond traders may not want.

Traders in bonds and commodities have indirect exposure to forex risk but cannot use them as underlying to trade in currency derivatives.

The full repercussions of this circular will unfold in days to come.