Perils of using the Last Traded Price (LTP)

You have created an excellent option strategy, and backtesting shows that it can be profitable. However, the strategy didn’t hold when you applied it in the real market. What could have gone wrong? Did you use the Last Traded Prices (LTP) in your backtest?

Most option backtesting tools design trading strategies using the last traded price.

For LTP to be useful, the option you trade in should be an at-the-money (ATM) option with ample liquidity. Typically, the closest expiry ATM strikes will be the most traded.

Trading activity drops almost exponentially for options with strike prices away from the spot price or farther from expiry. In such illiquid option chains, the last trade could sometimes be made hours before.

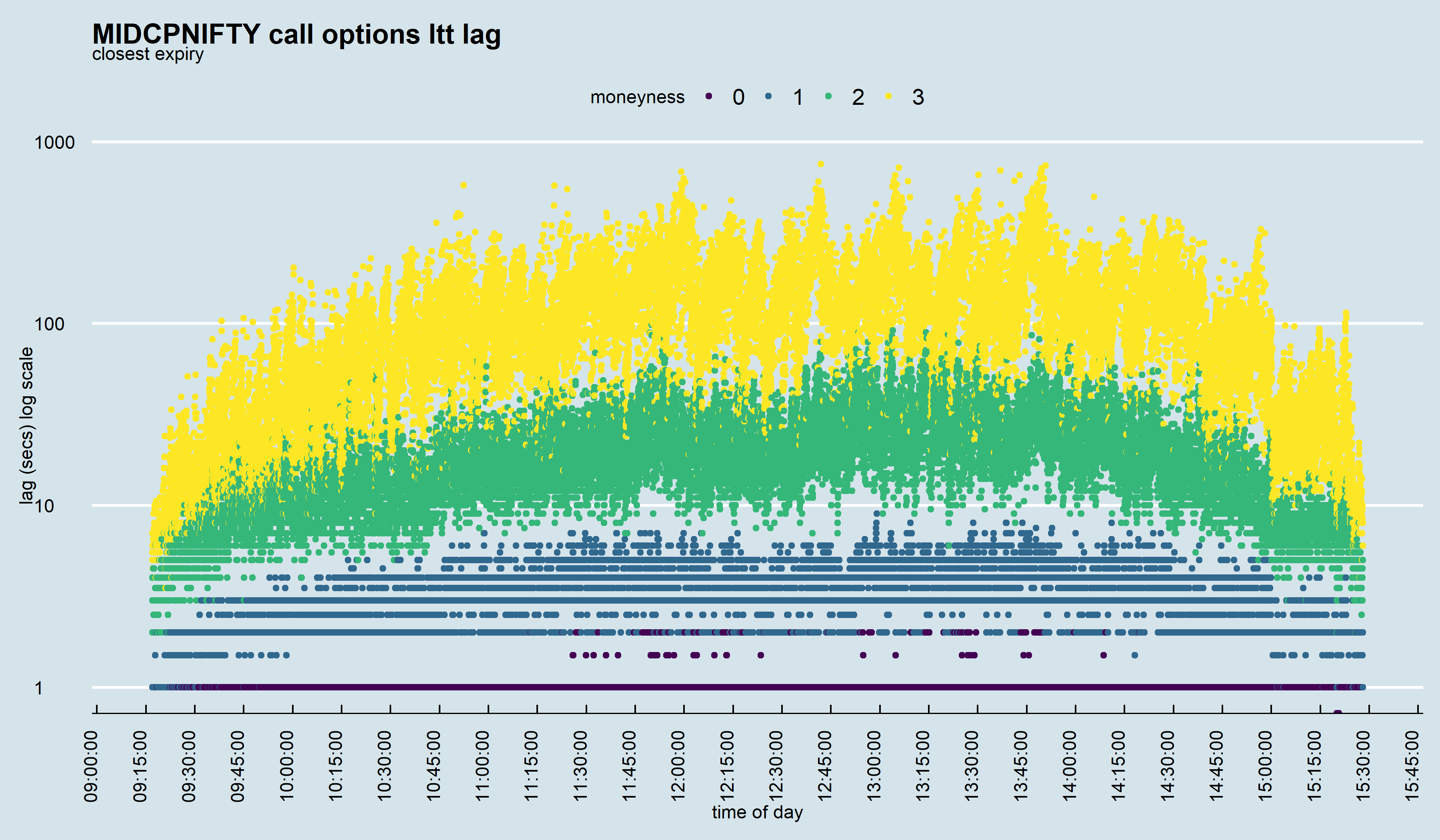

For example, look at this intraday cluster chart for the MIDCPNIFTY call option chain. You will see a similar outcome for a put option chain, too. The chart shows the time to execute a trade on the Y-axis vs the time of the day on the X-axis. Purple dots represent ATM strikes, the blue and green dots show ITM strikes, and the yellow dots show deep ITM strikes.

You can reliably use the last traded price only on the ATM strike of the closest expiry option contract. For the blue dots, which are near the ATM strikes, the time lag between now and the last traded time stamp is mostly under 10 seconds. As moneyness increases, the time lag also increases along the Y-axis. The yellow dots are deeper in-the-money-options. Their time lag ranges from 100 to 1000 seconds.

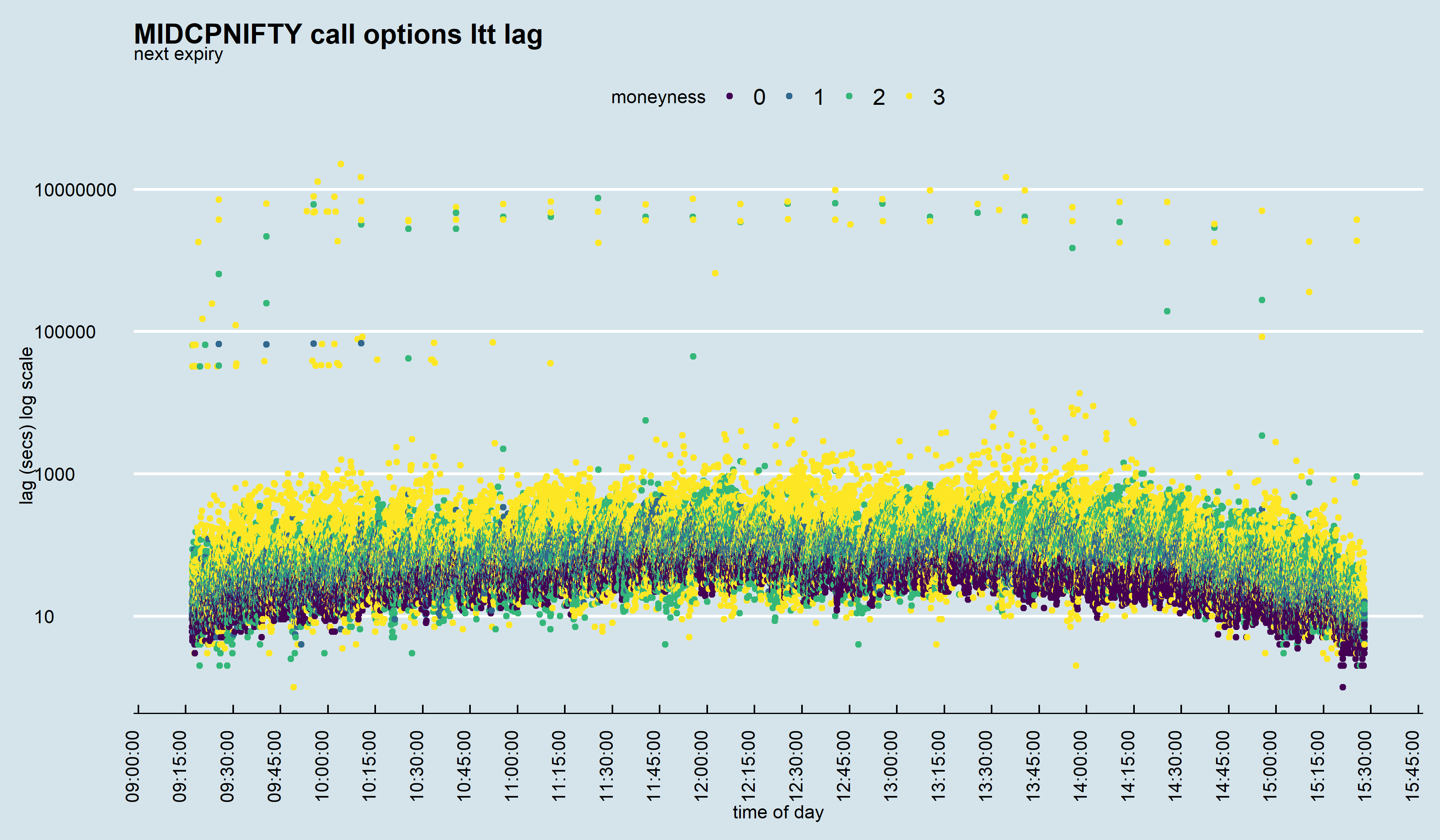

Now look at this MIDCPNIFTY option chain with next-month expiry.

As you can see on the Y-axis, the time lag has gone up for all strikes. Some dots even have a million seconds lag. Clearly, LTP can be of little help here.

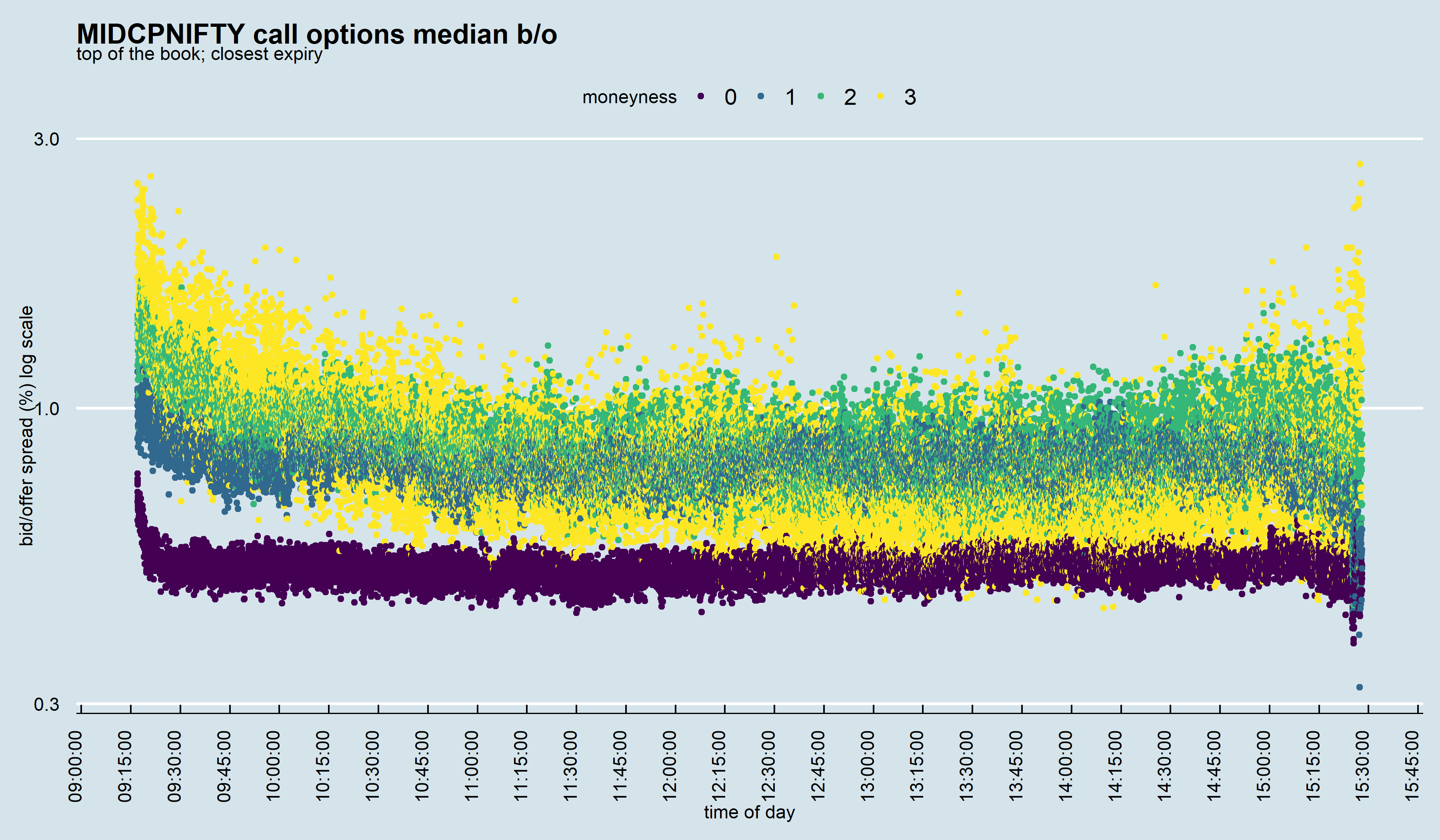

To get a realistic feel for how a strategy might perform in the real world, you should use the bid/offer spread. Trading strategies that look good with the Last Traded Price (LTP) might fail with the bid/offer (b/o) spread.

Look at the chart below. The bid/offer spread is wider for ITM options. Wider spreads mean your trades based on LTP could take longer to execute or not get executed at all.

The peril in using LTP is that you might be misled into thinking that the “market is wrong,” but it’s your data that is lagging. Most of these perceived dislocations don’t actually exist if you use the quote data.

The other problem with illiquid options is that, very often, it is tough to realize profitable trades on paper, given the haircut that the bid/offer spread imposes. Your alpha must be consistently large enough to cover not only the transaction costs but also the bid/offer spread.

There are no shortcuts to knowing market internals.