Cash is King but the Future is Basis

When you hear about markets making new highs or the “nifty” went up 100 points, it typically refers to the NIFTY 50 index. An index is an aggregate measure – a shorthand to convey information. For example, the NIFTY 50 reflects the price returns of 50 of the largest stocks (+ their DVRs). So, instead of listing out 50 stocks, you can just say what the NIFTY 50 did.

An index is, therefore, a theoretical construct. i.e., you can’t trade an index. You can only trade things built on top of it – futures, options, index funds, ETFs, etc…

Let’s say, you are bullish on the short-term prospects of the NIFTY 50 index and want to buy it. You can do so through NIFTY futures. However, you will immediately notice that the price of the futures is higher than the index level.

Enter the basis.

Basis, the difference between the price in the index and the price of the futures contract exists because of the time value of money. The index tells you the price now. Whereas, the futures contract is about the, ahem, future.

For every buyer of a futures contract, there is a seller. So, when someone sells you the contract, he’s on the hook to either deliver the goods at expiry or make good on the difference between the prices at which he sold and where the futures contract expired. Typically, the seller doesn’t want to be “naked” short – they don’t have an opinion on whether NIFTY is going up or down. A simple way to neutralize the position is to just buy an equal amount of the NIFTY 50 index fund or ETF and hold it till expiry. However, in order to buy, the seller needs to pay upfront. There is an opportunity cost that comes with locking up those funds till expiry. The basis is the price of this opportunity cost.

Quite simply, FV = PV x (1 + rf)t where rf is the risk-free rate and t is the time to expiry.

The situation gets a bit muddled if there are dividends issued by the stocks in the index. While the equity holder is entitled to the dividends, the futures holder is not. So, until the ex-dates, when the underlying equity prices are adjusted down, the basis can be lower than what is typical and sometimes even negative if the dividends are large enough.

Another way that someone who is short the futures can hedge is by “borrowing” the stock in the SLB (Stock Lending and Borrowing) segment. Here, one can pay a market-determined interest rate and borrow stocks to neutralize their short positions. And it’s worthwhile mentioning that the owner of the stock gets the dividends, not the borrower. Sometimes, some stocks can end up becoming hard to borrow either because large holders of that stock are not active or because there could be some buy-back program in effect. When the borrow yields get displaced, the basis gets dislodged as well.

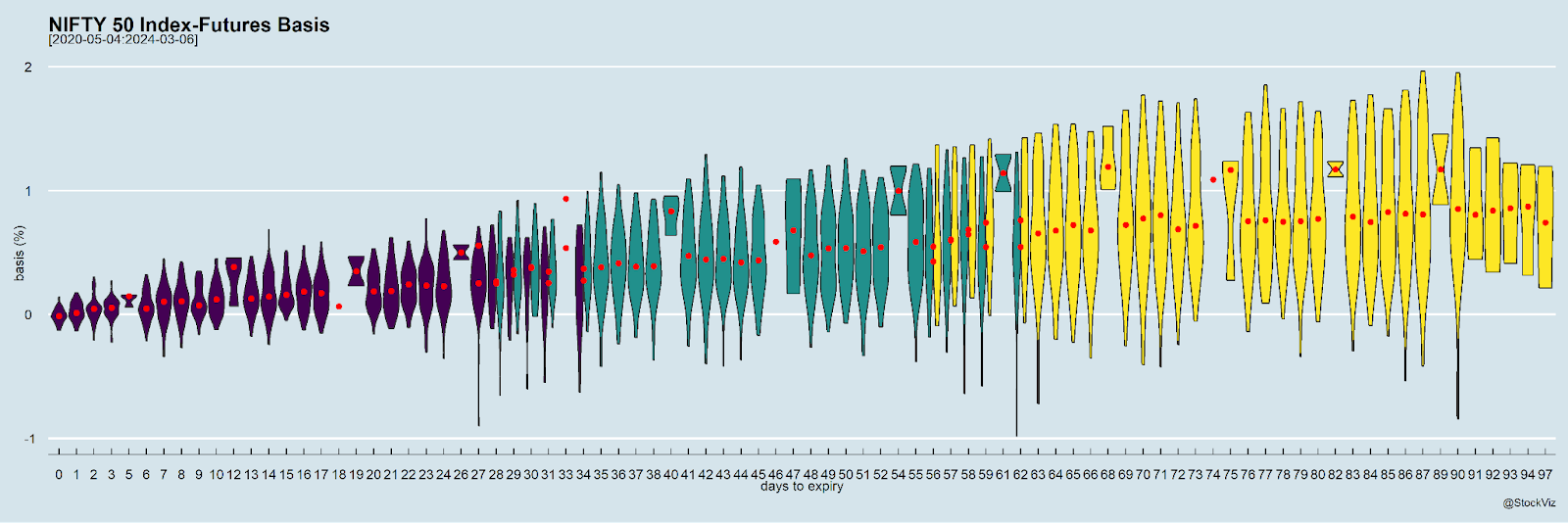

So, how the NIFTY cash-futures basis look like?

As you can see, the basis typically increases with days-to-expiry, but there are quite a number of days in which the basis goes negative. However, to quantify the arbitrage opportunity, you will have to adjust these for the underlying corporate actions.

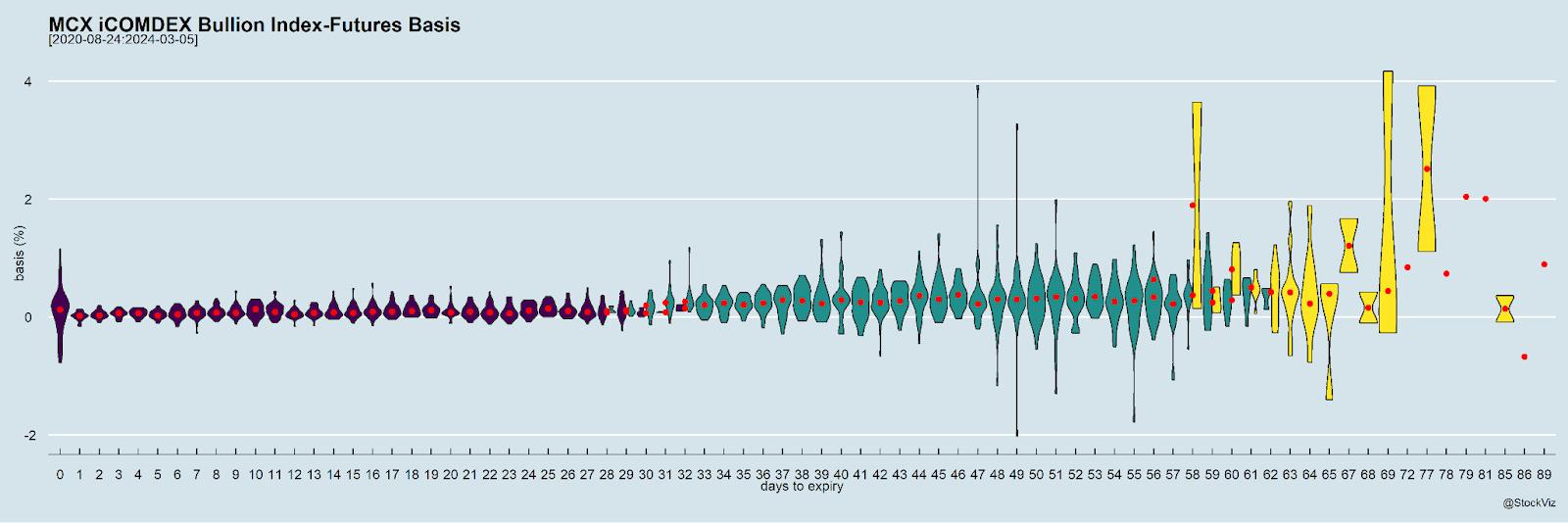

Commodity markets have the advantage of not having those pesky corporate actions to deal with. The MCX iCOMDEX Bullion Index, which is itself a combination of gold and silver indices, has futures listed on it.

Here, too, the basis occasionally goes negative. If you are interested in trying your hand at arbing the cash-futures basis, then this could be a potential hunting ground. It should be simpler than arbing the NIFTY 50, at least.

But how simple is it, really? For instance, on 2020-11-05, there was a basis of more than 2% on the December (24th) expiry futures. The Bullion index was comprised of 70.52% Gold and 29.48% Silver at that time. To arb this, you will have to buy the Bullion futures and short the underlyings (Gold & Silver). However, the underlying contracts have different December expiry days: GOLD 4th, GOLDPETAL: 31st. No matter which contract you choose, you will be taking on another type of basis risk. Besides, if you go with the GOLD and SILVER contracts, you’ll have to sell 21.35798346 and 41.38565905 contracts, respectively, for each Bullion index futures you buy. Getting rid of those decimals means trading massive exposures.

Does the cash-futures basis do weird things occasionally? Yes. However, arbing it requires deep pockets and risk management abilities that are beyond the reach of typical retail investors.