Avoid surprises: why disclosures are important in a health insurance policy

When it comes to health insurance plans, every policyholder has one essential requirement—transparency from the insurer.

Everyone seeks a health insurance provider who will be upfront about a policy’s drawbacks, exclusions, and probable suitability. Let’s be honest about it, health insurance policy documents are a maze—a deadly combination of legalities, medical terminologies, and financial jargon.

Unfortunately, most providers are not straightforward about the cons of their policies. This pushes potential health insurance buyers to seek expert guidance from neutral platforms that would help them choose the best possible policy.

On the other hand, health insurance providers have a similar ask – transparency from their potential policyholders, or in other words, disclosures. So, what are these disclosures in health insurance plans? What can happen if you fail to disclose details to your health insurance providers?

Here’s what we have gathered from the industry experts at Ditto Insurance –

What are Disclosures in Health Insurance Policies?

| In a Nut Shell: Medical history details of the policyholder |

There are certain details that you are expected to be transparent about when applying for a health insurance plan. This involves details regarding –

- Your pre-existing medical conditions (anything that you have been diagnosed with and have taken medications for over the last 3 years. On the other hand, it’s best to declare any and all prior ailments that you have been diagnosed with across your life.)

- Any family medical issues (in case you have been diagnosed with the same medical condition as any of your other family members)

- Your prior history of hospitalisation/treatments or surgery (along with the reasons, frequency, and the tenure of your stay – submitting reports would be helpful)

- Any diagnosed chronic ailment (any ongoing medication or any medications taken in the past with prescriptions, if possible)

These are called disclosures in health insurance.

Here is an example of two real cases where there has been a risk of claim rejection and, in the worst case, policy termination.

Case 1: A case where mild non-disclosure could be requested to be reconsidered

In November 2022, a policyholder bought a health insurance plan for his parents through an expert platform. However, he didn’t disclose that his father had been taking hypertension medication for 12 years.

In April 2024, his father was hospitalised in Chennai for a kidney infection (Pyelonephritis). The family filed a cashless claim for ₹1,00,000, but it was rejected when the insurer discovered the undisclosed hypertension.

This highlights the risk of non-disclosure—claims can be rejected. The intermediary suggested filing a reimbursement claim (where you pay upfront and claim the expenses later). The waiting period for hypertension under the policy was two years. Since that period had passed and there were no further non-disclosures, the insurer approved the reimbursement. However, you must understand that all insurers may respond in the same way.

While the claim has been approved, the family has had to endure the stress of rejection and the anxiety of waiting to see if it will be accepted.

Case 2: A case of non-disclosure that led to policy termination

Let’s look at another case –

In February 2024, an individual bought health insurance through a platform but failed to disclose her history of strokes since 2021.

In August 2024, she filed a claim for a heart attack requiring hospitalisation. The insurer reviewed her records, found the undisclosed strokes, and rejected the claim.

The policyholder argued she had mentioned a past hospitalisation (for diabetes, not strokes) to the advisor, but it wasn’t noted. Despite her efforts, the insurer rejected the claim and terminated the policy.

In this case, the claim wasn’t just rejected—the policy was terminated, which would make it harder for the policyholder to get another policy.

These examples highlight the importance of disclosing medical conditions when applying for health insurance. Now, let’s focus on what disclosures are and the possible consequences of non-disclosures.

Why are Disclosures Important for Insurers in Health Insurance Plans?

| In a Nut Shell: It determines the premiums, choice of health insurance plans, and underwriting directions. |

- The Calculation of Premiums

Many platforms offer free health insurance premium calculators where you enter details like age, coverage, and gender to estimate premiums. However, these numbers are only approximations. Actual premium calculations use “actuarial science,” factoring in many elements like:

- Age

- Gender

- Medical history

- Medical issues across the family (in case you have been diagnosed with the same)

- History of hospitalisation

- BMI (Body Mass Index)

- Location (Tier 1/Tier 2/Tier 3 cities)

- Number of family members covered

- Claim history (in case you are porting from one health insurance plan to another) and more

(Additionally, these premiums vary based on your choice of health insurance plan and provider. This will be discussed in the next point.)

- The Choice of Health Insurance Plans

While comprehensive health insurance plans are suitable for everyone, some policies are crafted as niche products—the target is to offer niche plans to policyholders with specific medical conditions. By disclosing your medical conditions, the insurer or the advisor will be able to help you with more suitable policy.

For example, heart-specific health insurance plans bridge gaps in standard coverage for cardiac patients. They offer:

- Short waiting periods for cardiac treatments

- Extensive pre- and post-hospitalisation coverage

- Add-ons tailored for cardiac issues

- No room rent restrictions

- No sub-limits on cardiac procedures

(that is, considering you have chosen an ideal health insurance policy for heart patients)

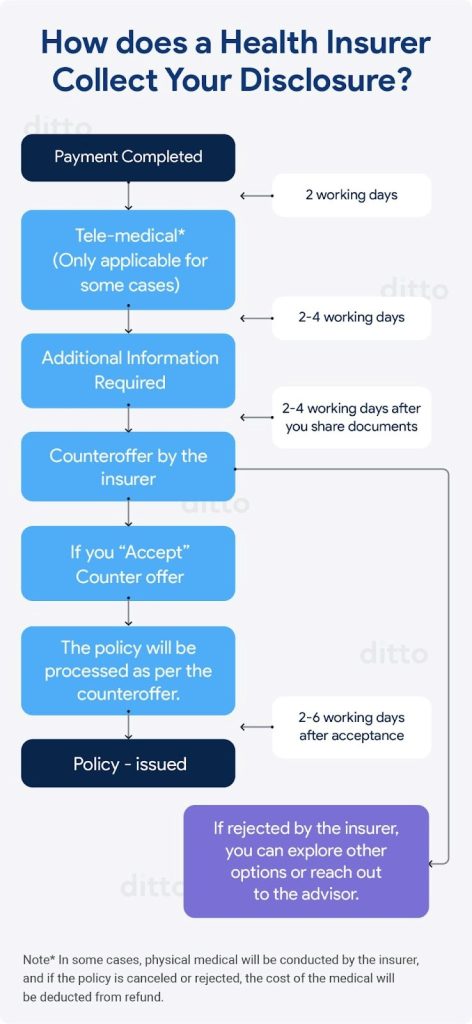

- The Health Insurance Application Process

Here is the process by which the disclosures are collected from a policyholder.

(Underwriting is the insurer’s method of evaluating the risk of providing coverage. While it may not seem like a direct benefit to the policyholder, it plays an important role in ensuring the right premium amount is set, thereby lowering the chances of claim rejection.)

So, the moment you provide the details as disclosures in your health insurance policy, the insurer’s underwriting team will evaluate those details and start working towards your policy. The team builds an accurate premium (including loading charges if required) and finds the best possible policy based on your disclosures.

What should a policyholder expect in cases of non-disclosures in their health insurance plans?

| In a Nut Shell: You might be looking at rejected claims, discontinued coverage, or blacklisting – depending on the severity of the case and the health insurance provider in question. |

The demand for health insurance has risen due to rising healthcare costs, medical inflation, and COVID-19 awareness. However, insurers are more cautious about fraud, leading to stricter actions for non-disclosure of medical details:

- Claim rejection: If key health details are not disclosed, claims are likely to be rejected, leaving policyholders to pay out-of-pocket despite having insurance.

- Plan termination: For non-disclosure of serious conditions, insurers may cancel the policy, leaving the policyholder financially vulnerable. This termination also appears when applying for future coverage.

- Blacklisting: In extreme cases, non-disclosure may be seen as fraud, resulting in blacklisting. This makes it hard to find new coverage, often leading to policies with high premiums and many restrictions.

Conclusion

A health insurance policy can be your financial ally during medical crises. To get the best plan, ensure transparency by fully disclosing your medical history. As it is, after you provide them with all the details, the underwriting team will examine the details and health insurance plans come with a moratorium period (a period during which the provider keeps taking a closer look at your medical history to explore the disclosure details that you have provided) of 5 years. And you know, what exactly should you expect and not expect? So it’s wiser to come clean and secure a reliable policy early!

This article is authored by Shrehith Karkera from Ditto .

The views and opinions expressed in this blog are those of the author. All content provided is for informational purposes only and should not be taken as professional advice.

thank you for sharing valuable knowledge

This article provides valuable insights into the importance of transparency when purchasing health insurance. Disclosing pre-existing conditions, family medical history, and past treatments can significantly impact claim approvals and policy terms. For those seeking comprehensive health coverage, I recommend Care Supreme Health Insurance, which offers robust protection and peace of mind.

This was truly a well written coverage on Insurance and its disclosures appropriately blending its importance from both the insurer and policyholder’s aspect.