What did we learn?

2023 was an interesting year, to say the least. Given the new year, it’s a good time to reflect on the year that has passed. When I wrote a post last year looking back on 2022, the mood was gloomy due to all the markets undergoing a detox. Investors were bracing for a bear market because interest rates were rising globally. The consensus was that the US would enter a recession, and as the saying goes, “if the US sneezes, the world catches a cold.” However, what transpired in 2023 was the opposite of what most investors expected.

There’s always craziness in some corners of the markets. It’s a good idea to look back on some of the crazy things and learn a little. We learn so that we can ignore the lessons and make the same old mistakes in unique ways. In this post, I look back on a few interesting developments in 2023 including why losing money was hard in 2023, bull market mistakes, the importance of good behaviour, why boring things work, etc.

What’s gonna happen, who knows?

2023 was a good year for the markets on the back of a depressing, 2022. Before we look at 2023, I want to step back a little and reflect on the last four years because it’s a unique period. We’ve probably lived through 10 years worth of events in this short span. There are valuable lessons that we can take away from this weird and crazy market phase. It has been four years since the worst of COVID. For many, the 2020 crash has faded into a hazy memory, but I still often think about it because it was my first serious financial crisis — I’m a post-2008-baby.

COVID wasn’t just a financial crisis but an existential crisis that affected everything and everyone. Think about the fact that we shut down the entire global economy and restarted it. At the risk of stating the obvious, shutting down and restarting an economy is not like restarting a car. The fallout from COVID was devastating. On the one hand, you had a massive loss of life and the destruction of livelihoods. On the other hand, you had a spectacular episode of financial instability.

First, global equities fell by 20–40% in a month. For comparison, it took 8–9 months for the markets to fall by ~35% during the 2008 global financial crisis. In 2020, by the eighth month, markets had recovered all their losses (black line). Such was the ferocity of the crash and recovery.

Then, the panic spread to the bond markets as spreads widened, pushing up borrowing costs. This caused credit rating agencies to downgrade a record number of companies. Predictions of corporate defaults also rose dramatically. At the same time, there was a dash for cash. Everybody, from individual investors to corporations to large institutional investors, wanted cash, which led to a wholesale dumping of bonds. This selling pressure led to the evaporation of liquidity in the government bond markets and money markets—it was like a run on the bond markets. This pressure was perhaps the most acute in the all-important US Treasury market, which seemed like it would snap. Currencies, except the dollar and key commodities, all crashed alongside.

Then, there was a dramatic policy response from governments and global central banks. Governments took various measures to reduce the loss of livelihoods through loan moratoriums, cash benefits, and other stimulus programs. Central banks deployed all the monetary policy tools in their arsenal on a scale never seen before, not even during the 2008 crisis.

To give you a sense, the G10 central banks increased their balance sheet size by $6 trillion in just three months. This is over and above the billions and trillions funnelled into the hands of consumers. This stunning liquidity injection put a floor under global financial markets, and the panic subsided. All these events transpired in 7-8 months. In many ways, reality was unfolding at 3X speed.

Source: BIS.

Source: BIS.

Now, think about the market performance in the last four years. In 2020, we had the worst market crash since 2008. Large, mid, and small-cap indices were down between 38% and 45% in a month at the depths of the COVID crisis panic. But we then saw one of the fastest recoveries ever, and all the indices closed in the green. In 2021, we had a rip-roaring rally, especially in mid- and small caps.

In 2022, the sentiment soured as inflation spiked worldwide due to pandemic-induced supply and demand idiosyncrasies. As central banks started hiking rates, equity and bond markets fell around the world. The worst of the fall was in the growthiest segments of the markets, like tech and speculative asset classes and sub-asset classes like crypto, NFTs, SPACs, and investment themes like “disruptive innovation” and unprofitable companies, especially in the US. This was the theme of last year’s review. The Indian markets were insulated from the crash as India came to be seen as an oasis in a dreary world.

2023 was a repeat of 2021, as the global markets all but erased the losses in 2022. Though not as crazy as 2020 and 2021, there was euphoria in the markets again. Small caps, IPOs, penny stocks, and crypto all had a good year.

The last four years are the perfect example of how unpredictable markets can be. Duh!

Everybody was a genius

Everything went up in 2023. In fact, you couldn’t have lost money even if you tried.

Here’s a simple experiment: we created three equal-weight portfolios of 30 stocks randomly chosen from the Nifty Small-Cap 250 index. Of the three, one portfolio underperformed the index and yet was up 33%. The other two were up ~43%, in line with the index.

Another way of looking at this is the performance of the Nifty Microcap 250 index. This index consists of 250 stocks beyond the Nifty 500 and is up 60%+, while the Nifty Smallcap 250 index was up 45%. So, no matter how scientifically stupid your stock picking was, odds are you would’ve done better than Nifty 50 at the very least.

Like 2021, it’s a good time to remember one of my favourite quotes:

“Don’t confuse a bull market with brains!”

The real superpower

When the entire world is going mad, the ability to remain sane is a superpower. This is true in both bull markets and bear markets. In a bull market, you need to have the equanimity to say that the good times won’t last forever, and in bear markets, you need to have the courage to say that the bad times don’t last forever either.

This chart shows the annual Sensex returns in green and the fall from the peaks (drawdown) within that year in red. 2023 was the 8th consecutive year Indian markets delivered a positive return.

Will the good times last? I wouldn’t bet on it, but then again, nobody knows what’s going to happen.

Things change. That’s about as sure a prediction as I can make. Your investment strategy should be designed to survive different market conditions. You can leave the predictions to the astrologers and parrots.

There’s always a party somewhere

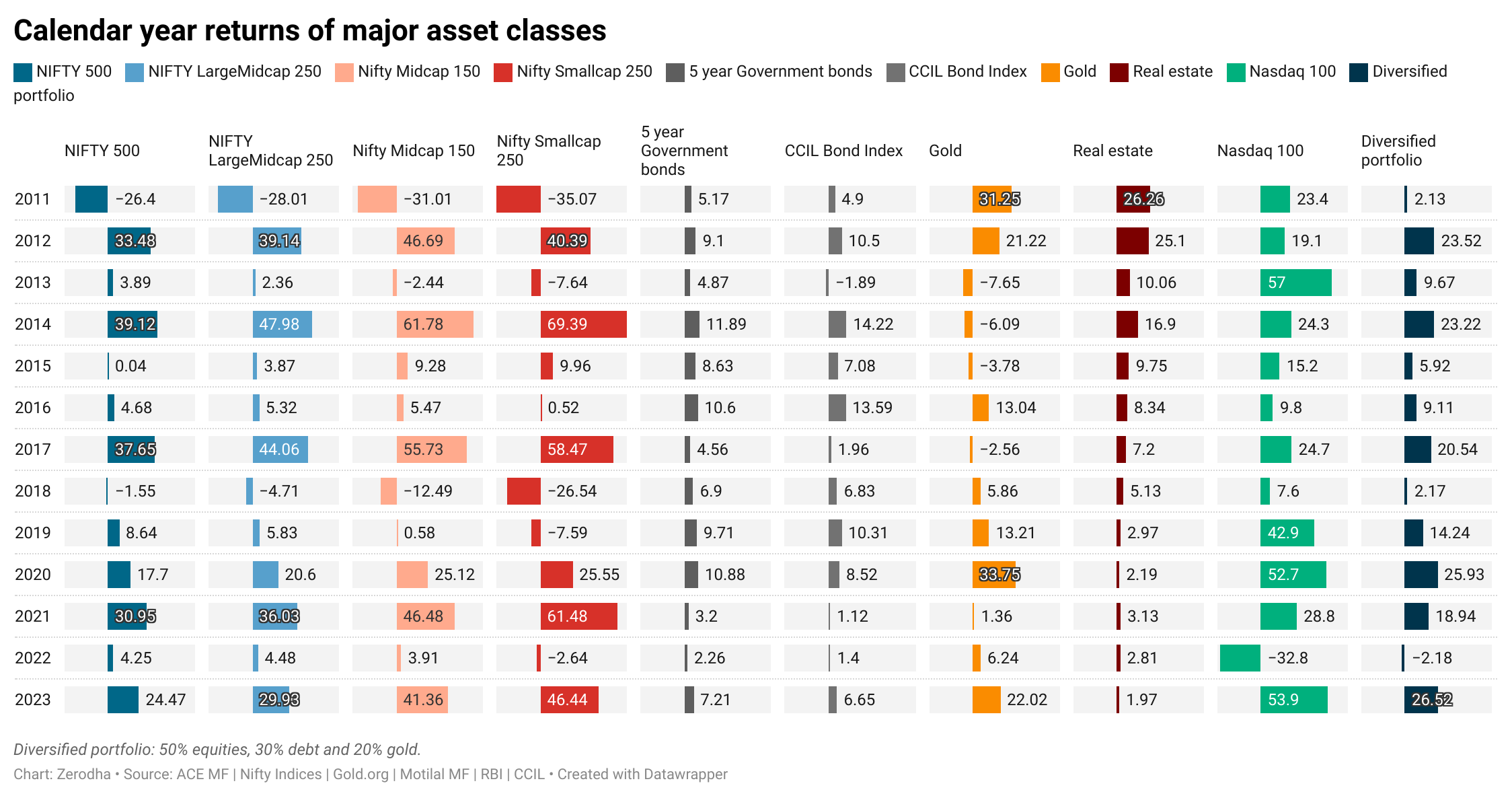

Everything is cyclical in the markets. Something will do well some of the time, and nothing will all the time. Take a look at the annual performance of the major asset classes.

Here’s the annual performance of various sectors.

The best-performing asset classes and sectors keep changing. If you can pick the best asset classes, sectors, and stocks, you’re a genius; enjoy being rich. But most of us aren’t. If you keep jumping between what’s doing well, you will surely underperform a fixed deposit.

It’s never easy to watch something you don’t own go up. You will have raging FOMO, and you will feel miserable that something that you don’t own is doing better than what you do own. If you talk to other people about your investments, things get worse. You may look like an idiot because they might be making a ton of money by doing something stupid. In any given year, anything from small caps to shitcoins will be doing well. But the only way to create wealth over the long term is to resist the urge to do something stupid. You have to be comfortable looking like an idiot in the short term. That’s where returns come from.

Everything changes, except human behaviour

Now, just because people like me write gyan blog posts on what not to do doesn’t mean people will listen. The world changes, markets evolve, and the planet itself changes, but the one thing that doesn’t change is human behaviour. Over the 400-year history of modern financial markets, people have made the same old mistakes in different ways. We humans are terribly unoriginal.

A classic bull market mistake is chasing whatever is doing well. In 2023, this was the mad rush by investors into small and mid-caps. From 2018 to 2021, when the mid-cap and small-cap indexes were sideways, there were net outflows from mid-cap and small-cap funds. But as soon as the mid and small-cap funds started doing well in 2021, there were continuous inflows. What’s weird is that flows into large-cap funds have fallen, and there were even outflows in some months in 2023. It seems like people are investing in mid-cap and small-cap funds by redeeming or changing allocations away from large caps.

This isn’t new, and there are countless examples. We’ve seen this with PSU banking funds in 2023, IT funds in 2021, US funds in 2019–2022, crypto from 2020–2022, mid and small-caps until 2018, and so on. Whenever something does well, investors inevitably deviate from their plan and pile into the shiny object of the moment. I’m repeating what I mentioned above, but it’s never easy watching what you don’t own do well. We all know that a sensible and diversified portfolio has a high probability of doing well over the long run. But to reap the benefit, you must stick with it like grim death, as Cliff Asness says.

“A huge part of our job is building a great investment process that will make money over the long term, but a fair amount of our job is sticking to it like grim death during the tougher times.” — Cliff Asness

Boring worked, again.

I want to share something Morgan Housel said on a recent podcast:

What matters is not necessarily what are the best returns that you can earn this year – that’s what everyone chases – but that’s not what matters. What matters is what are the best returns that you can sustain for the longest period of time.

So, this is why, on an annual basis, I strive for average returns in my index funds by design. Why do I do it? Because that’s going to give me the endurance to hold them for 50 years. And if you can earn average returns for 50 years, you’re going to end up in the top 1% of all investors, and you can do it with zero effort. What’s average in the US Stock Market? 6% real (six and a half percent real after inflation) is what’s been. If you can earn six and a half percent returns after inflation for 50 years, it’s going to achieve dynastic wealth, making your great-grandchildren wealthy, and you can do that with zero effort.

Now, look, past performance is not indicative, there’s a nuclear war, etc. You can come up with all these scenarios in which it’s not going to work out, you can come up with scenarios in which the economic conditions of the last 100 years are not going to replicate for the next hundred years. Okay, all those aside, earning average returns for an above-average period of time is way more lucrative than trying to earn superior returns for a shorter period of time.

In other words, stick to the boring stuff. Look at the last column in this chart. Those are the returns of a hypothetical portfolio of 50% in Nifty 500, Nifty Midcap 150, and Nasdaq 100, 30% in government bonds, and 20% in gold. The returns are pretty good. They aren’t as high as 100% equities and as low as 100% debt, but they are somewhere in the middle.

A 100% equity portfolio is like eating something new from a fancy hotel every day. A diversified portfolio, on the other hand, is like dal chawal. Now, you might enjoy eating something new every day for a while, but in the long run, you’ll ruin your health. Dal chawal, on the other hand, is boring but healthy. It’s not easy to stick to dal chawal in the long run, but you’ll live longer.

It doesn’t just end with investing in a diversified portfolio. Here’s a counterintuitive fact: most of your returns won’t come from high returns but from increasing your savings rate. Let me illustrate this with an example. This chart shows two scenarios:

- A monthly SIP of Rs 5,000 in the DSP equity and bond fund.

- A monthly SIP of Rs 5,000 in the same DSP Equity and Bond Fund, but with an annual increase of 5%. This means each year, you add 5% to the monthly investment amount, starting from Rs 5,000. So, it’s Rs 5,000 plus 5% in the first year, and this increment continues each year.”

In the scenario where you invest a fixed amount of Rs 5000 a month, you would’ve invested Rs 14 lakhs, which would’ve grown to Rs 1.19 crore over 23 years. If you had increased your SIP amount by 5% every year, you would’ve invested Rs 27 lakhs, which would’ve grown to Rs 1.59 crores. In both scenarios, the return on the fund is the same, but the final investment is different because you invested more.

Now, this is a hypothetical example. If you do well in your career, you will not only be able to invest more than Rs 5,000, but you will also be able to increase your SIP amount by more than 5% every year. You also might have bonuses and other large one-time cash flows that you can invest over and above this. So, you can very well build a large corpus. If you invest regularly, increase the investment amount every year, behave well, and if the markets do well, your final investment amount might give you a heart attack.

So, what is the best approach to investment success? In my opinion, less choice. Low cost. Don’t look at your portfolio values very frequently. Don’t peek! It’s a bit hyperbolic, but I tell people that every time they get a statement, throw it in the waste basket. Do not look at it. And only when you retire, open the statement. But before you open it, have a cardiologist in the room, because you’re probably going to have a heart attack. You simply won’t believe how much money you’ve accumulated over all those years. It’s the compounding. The phrase I use is this: “Enjoy the magic of compounding long-term investment returns without the tyranny of compounding long-term costs.” – Jack Bogle

Predicting is a fool’s errand but a solid business opportunity 😬

At the end of every year, you see “experts” and “specialists” try to predict how the markets will perform the next year. They use everything from artificial intelligence, blockchain, kundli, and technical analysis, but they are worse than a drunk guy making predictions. Most analysts are like Royal Challengers Bangalore (RCB), almost close to winning the trophy for 16 years.

This is just one example of how hard it is to make predictions. As much as we would like to think experts can predict the future, there’s no evidence of that, and you don’t have to take my word for it.

- In December 2022, the Financial Times surveyed 45 economists about their predictions for 2023. 85% of them predicted a recession in 2023. They were wrong.

- The CXO Advisory Group analysed 6584 forecasts from 68 finance gurus. Only 48% of the forecasts were accurate, and 66% of the gurus were accurate by less than 50%.

- Vanguard looked at the predictions of top analysts from 2011, and the actual returns of the S&P 500 index were wrong in 9 out of 12 years.

- Researchers looked at median analyst estimates for earnings growth from 1997 to 2021. Much to the surprise of the analysts themselves, the analysts were so wrong that they made my neighbour’s dog look like Warren Wooffett.

- If financial analysts are bad, economists are worse. Economist Zsolt Darvas analysed the inflation forecasts of the European Central Bank (ECB). From 2013 to 2020, the ECB consistently predicted a rise in inflation, but the actual inflation remained well below the target.

- Bloomberg analysed over 3,200 GDP forecasts from the International Monetary Fund (IMF) since 1999. In 6.1% of the cases, the IMF was within a 0.1% margin of error. But in 56% of the cases, it underestimated the GDP growth and overestimated it in 44% of the cases. The average forecast gap was 2%.

I can keep going, but you get the point.

One of my favourite examples of the futility of predictions is of the legendary Jeremy Grantham. He is best known for his prescient predictions of the Japanese crash, the dot-com bubble, and the 2008 crash. Since the 2008 crash, he’s been bearish to various degrees, but the US market has had one of the best decades ever.

I’m sharing this chart with the utmost humility. My point is not to illustrate that Mr. Grantham is a terrible forecaster; we’re all wrong most of the time. Who the hell am I to judge someone so accomplished? But the point is, your investment decisions shouldn’t be based on what some famous investor said.

You should listen to the best, including Jeremy Grantham, and learn from them. He has written some remarkably insightful letters over the years, like this one, for example. But the ultimate decision to invest or not invest in something should be based on your research and understanding. You can’t invest based on borrowed conviction. Jeremy Grantham or Warren Buffett won’t send you stock tips with entry and stop-loss targets on WhatsApp.

Look, there will always be a gifted few who’ll have clairvoyant abilities and make a ton of money. But most experts are as good as my neighbour’s chihuahua trying to pick stocks. If your investment decisions rely on predicting the future or the expertise of experts and gurus, you are better off putting all your money in a fixed deposit and moving on with your life or please contact me. I’m a god when it comes to picking stocks, and I run a paid seminar on how to pick stocks. Limited seats available.

“When one is investing, one is dealing with the future. None of us – regardless of intellect have actually been to the future, so we don’t know what we are talking about” – Hugh Hendry

Having said that, people crave certainty, and they want to be told what to do. Why do you think all these gurus and experts have such huge followings and lucrative businesses? Giving people what they crave and catering to people’s greed and anxiety will always be a good business model. So the moral of the story is that being a charlatan and scammer is lucrative 😛

Never bet against India?

In his 2021 letter, Warren Buffett famously wrote, “Never bet against America.” If you look at the 37-year history of the Indian markets from when the BSE Sensex index was created in 1987, the Indian markets have done remarkably well. Just like betting on America has been rewarding, so has betting on India.

So far, despite all the end-of-the-world events, our markets have always climbed the wall of worries and rewarded patient investors. The last 5 odd years are a case in point: we had a pandemic, two wars, the threat of nuclear armageddon, historic financial volatility, a mini-banking crisis, locusts, floods, wildfires, and god knows what else. Despite that, the Indian markets are at lifetime highs.

I know, I know. Past returns blah blah. What if India becomes Japan, blah blah?

These are valid concerns. But only God and the all-knowing YouTube gurus can predict the future. I’ve no clue if the Indian markets will do well. If Vladimir Putin or Kim Jong Un decides to press that big red button, long-term investing will be the least of our worries. If you listen to the news at any point, you can find 10 reasons why the world will end soon. But despite all the monumentally dumb things humans do, we’re still here. Will we be here tomorrow? Only that YouTube guru guy knows.

The reason why I like sharing this chart is to underscore the fact that there’s always a reason to sell. Investing requires a certain amount of irrational optimism. Long-term investing is a fundamental bet that the companies and by extension, the markets will do well.

But, Irrational optimism doesn’t mean irrational delusions. It goes without saying that you need to invest the right way. By that I mean, having a good entry, exit, and risk management plan. Investing in the right asset classes, having a sensitive asset allocation, and behaving well.

As for the What if India becomes Japan crowd, there’s a non-trivial chance that we might get hit by a bus, so why even step outside the house?

Here’s a brilliant quote about pessimism and catastrophizing that I heard on a podcast recently:

“I’ve suffered a great many catastrophes in my life. Most of them never happened.” — Mark Twain

So, what did you learn?

somebody once said, u don’t have to believe in truth, u jus need to hear it once .. then it will start forcefully operate in you .. that was the change this article brought to me …

this post has changed my entire perspective on investment …

I took some screenshots of this and referred again and again when in doubt ..

a true guidance, 24 carat gold, thanks .. @bhuvan

Hi,

Nicely written article with a lot of context!!

Also learned a lot about your neighbour’s pets 😀 😀

A well written article. Thanks 🙏

I completely agree with Never Bet Against India minimum for next 25 Years

Good read

Nice article. Thanks 🙏

Very well written!!

Its during the bad times when every analyst and find house is bearish on good stock, you should believe in the business and business’s profit making ability. This is where alpha is created by investing in good companies at cheap valuations..

Invest and wait for 1-2yrs to see the same fund houses turning bullish on these stocks..

Nothing is technical.. everything is based on macro and micros. Once there is money printing, excess liquidity market will rise… in bad times n high inflation period. Stocks will be hammered and kept in consolidation zone for longer time where retailers lose patience. Look at hdfc kotak bajaj finance asian paints.. invest and foget for 4-5yrs.. volatiliy is your friend in stock market!!

If you want sound sleep. Diversit your investments in direct stocks, small cap mid cap flexi cap direct active mutual fund, bond fund, SGBs, Nifty ETFs and some cash and sit tight. Enjoy the life!!! Because time is limited. Money printing is unlimited!!!

Fantabulous article with well informed facts, data and figures.

Highly appreciable brother.

Nice article. Patience is the name of the game!!

Very well described. Great analysis overall from different years . Humble yet very prescise.

Awesome article…It clears all my doubts and silenced all my anxieties..

Thanks not enough…Love you Guys..🇮🇳❤️❤️❤️

This was a great post!! Looking forward to reading more such articles from you.

The writer deserves a raise!

Awesome 👍. it was like reading a Wait but Why blog.

what an amazing amazing article, in the muddy sea of finfluencers, you, Bhuvan n Zerodha, are a lighthouse of right things …

Very good article Bhuvan

Really enjoyed reading it . Learner a lot of stuffs in my 20’s , I wish not to make the mistakes what others have done and to keep a long term investing perspective.

The best part of the article was roasting of RCB. 😂

Thankyou so much.

Ultimate stats. Liked that one – stats can give some sense although can’t predict anything as repeatedly told here. Kudos for summing this up. But aftercall, the question remains the same. What to go buy now? haha

Good article covers the investing predicament and opportunities in the simplest possible manner. I have been following this strategy for a while now and can’t say I’m disappointed in any manner whatsoever.

Excellent article!!

Thank you Bhuvan and Team Zerodha for this profound article. I have always liked the way you guys write the articles, they are factual, well researched, well presented and simple.

I’m sure that thiss article is going to be an eye opener for many Investors, specially the ones who get caught with predictions and YouTube Gurus instead of learning, researching and become a well informed investor.

Awesome! 👍!

Highly inspiring. Thank you.

Very Well Researched 👌🏻 and Top Quality 🔥 Article written by Bhuvan & Zerodha Team. Thank you for Awesome and Enlightening Article. Really Appreciate 👏🏻 your Efforts, Team Zerodha.

Good read.

Thank you for a well-researched and well thought through article.

Nice article, well done!