Dark patterns in finance apps

There’s a paradox at the heart of financial services: What’s good for financial institutions is rarely good for you. All of the shady practices we see and the depressing stories we hear can be explained by this paradox. One of the more depressing manifestations of this paradox is dark patterns.

Dark patterns are design practices and techniques with the express purpose of tricking and manipulating you into doing something that’s bad for you. Most dark patterns are not outright fraudulent, but they dance around the lines that separate what’s ethical and unethical.

“Dark pattern” might sound like an abstract term, but we all deal with and also fall prey to them on a daily basis without realizing it. Perhaps the most common dark pattern that most Indians would’ve faced is getting scammed into buying useless insurance policies from relatives or neighbors. So dark patterns have been around for a long time, but the internet has truly democratized them. 🙁

As I started writing this post, I remembered a phenomenally stupid story involving a dark pattern. The story involves a senior executive at a mutual fund company whom I’ll call Kumar. One of the policies of the company was to invest a part of the salaries of senior executives in its own MF schemes.

One day, Kumar wanted some money and went to the company’s website to redeem the funds. To his surprise, he couldn’t find the “sell” button after wasting an hour. Frustrated, he went to the person responsible for the website and told him that there was something wrong with the site and he was unable to find the sell button. He asked him, if an employee was unable to sell, how the hell could regular investors sell their investments? The guy in charge tells Kumar this was intentional and he didn’t want customers to sell their investments easily.

As noble as the intent is to turn all investors into long-term investors, this is a classic example of a dark pattern. Kumar didn’t need the money urgently, but what if this happened during an emergency? Dark patterns can have serious real-life consequences. The story I told isn’t an isolated incident. The financial services industry is rife with such unethical practices, some due to incompetence, but most of them are due to banal malice.

A couple of years ago, I moderated this conversation about dark patterns, and when I was preparing for it, the question I kept having was, “How the hell can humans, supposedly the smartest creatures in the known universe, get scammed by a sneakily worded line of text?”

We fall for dark practices because they take advantage of our cognitive quirks and limitations. In 2011, Jeff Hammerbacher, an early employee at Facebook, said:

“The best minds of my generation are thinking about how to make people click ads. That sucks.”

He was spot-on.

In his best-selling book Thinking, Fast and Slow, the Nobel laureate Daniel Kahneman conceptualized two modes of thinking: System 1 and System 2 thinking.

System 1 thinking is fast, automatic, and intuitive. In this mode of thinking, our choices and decisions feel quick and effortless because we rely on mental shortcuts like pattern matching, emotional resonance, and past experiences. However, System 1 thinking is prone to the common behavioral biases like anchoring, confirmation bias, etc.

System 2 thinking is the opposite of System 1. It is slow, logical, and analytical. In this mode of thinking, you consciously make decisions only after thinking about all the choices and trade-offs.

Dark patterns work because they take advantage of our default behaviors and cognitive blind spots or biases. These “biases” aren’t defects; this is why I’ve always hated the term because of the negative connotation. What seems like a “bias” becomes an “evolutionary adaptation” when looked at from an evolutionary lens. They kept us alive for hundreds of thousands of years but are no longer helpful today. As the saying goes, we are using Stone Age brains to deal with 21st-century complexity.

Dark patterns bypass critical thinking parts of the brain and take advantage of emotions and tendencies like greed, fear, hope, inertia, impatience, scarcity, loss aversion, and choice overload. So when that bank relationship manager or platform is selling you an insurance policy with a 11% return, they are taking advantage of greed and our tendency to not make complicated calculations (system 2 thinking).

Here are the most harmful dark patterns to watch for in financial apps:

The “casinofication” of everything

The explicit focus of finance apps to get traders and investors to do more of everything is the most harmful dark pattern in investing. More activity = more revenue is the strategy of the entire industry. Broking apps across the world have also borrowed the most addictive features from gambling apps and video games. Investing has been turned into a “game.”

This dark pattern manifests in different ways:

- “Tips” and “content” are designed to appeal to the greed in you and get you to do more.

- Gamification of trading and investing apps with pointless things like challenges, badges, streaks, leaderboards, celebratory alerts, etc. The goal here is to generate more “engagement,” whatever that means. The irony is that in finance, activity and results are inversely proportional. If anything, “disengagement” is the best thing for investors.

- Subtle stock tips that masquerade as generic notifications. For example, an alert that says “RELIANCE up 5%” might seem pointless. In reality, this is a notification designed to trigger people to trade RELIANCE.

- Offering loans on the same platform or order path as trading and investing.

- Creating a fake sense of urgency.

Hiding things

Being opaque is the default instinct for most financial services companies, including many brokers. Financial services companies love hiding things—from charges, pricing, processes, disclosures, and returns to business models, you rarely find the details you are looking for.

Examples of this:

- Even today, many brokers don’t explicitly disclose their pricing and charges related to their products and services.

- Brokers make it easy to open an account but hard to close it. They reject closure requests based on flimsy and downright idiotic reasons.

- Some advertise their products and services to be free, but make money elsewhere with ridiculously high charges.

Mis-selling

Selling horrible financial products is the oldest dark pattern in finance. From opaque structured financial products, costly leverage, high-fee financial products, and garbage insurance products to shady wealth management services, brokers cross-sell the most useless financial products.

If you look closely into the fees and returns of these products, very few of them make logical sense. In fact, if I were the prime minister for a day, I would not only make 80% of these products illegal but also make selling them a human rights violation. This reminds me of Cliff Asness’s quote:

“There is no investment product so good that there’s not a fee that can make it bad.”

A few examples of this:

- Advertising loans with misleading statements like “0% interest,” etc.

- Misleading benchmarking of investment products. For example, an equity mutual fund being compared with a fixed deposit, or a mid- and small-cap MF/PMS being compared to a large-cap index, etc.

- Misleading returns, like traditional insurance policies claiming 10% returns when in reality they are closer to 5-6%.

- “Algo trading” strategies that promise double-digit monthly returns!

- Promising guaranteed returns.

Defaults

The other common dark pattern is defaults. These are instances where choices and consent mechanisms that you didn’t agree to are pre-selected so that you blindly proceed.

A few examples:

- Opting you into products, services, and features that you didn’t explicitly choose or ask for.

- Making logins contingent on sharing content for things like data, checking credit scores, etc. There’s a popular investment app that doesn’t allow login without you allowing the app to check your credit score.

- Consent to share your data with the group or third-party entities for cross-selling other financial products.

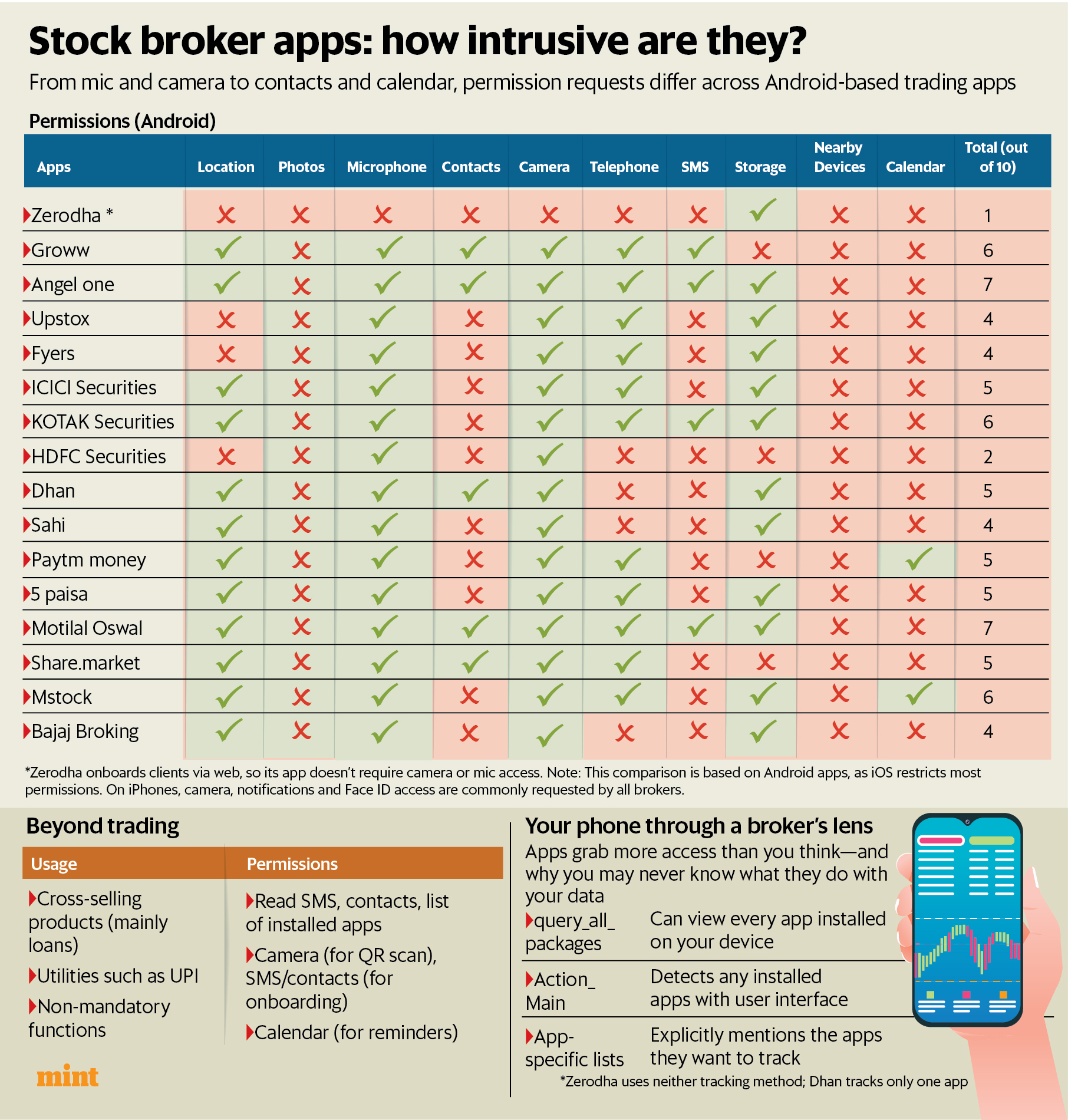

Tracking and selling data

Perhaps the most rampant dark pattern is the gross abuse of privacy. Today, most apps, including broking apps not only ask for unnecessary permissions to everything from the media in your phone, messages, calendar, and contacts, but also track your activity when you use other apps and websites. The term “tracking” doesn’t quite generate the same emotional response as “stalking.”

Source: Mint

Our philosophy

Much like other parts of financial services, the broking industry isn’t immune to dark patterns, but we at Zerodha have built the business from day 1 in such a way that we never have to do something shady to make a buck. At Zerodha, doing the right thing for the users is at the heart of all business and product decisions. To quote K:

“In hindsight, the business practices and end-user software that we have developed at Zerodha over the last decade, employ a philosophy that I would like to call user disengagement. At its core are two tenets:

Only do what is truly useful and meaningful to end users.

Don’t do unto others, what you don’t want done unto you.”

A few more things:

- We don’t have relationship managers or sales managers with sales targets.

- We don’t give stock tips. What most people don’t realize is that the reason brokerages give tips is to get you to generate brokerage for them.

- In fact, we actively try to discourage users from trading in many different ways, from nudges to Kill Switch.

- Absolute transparency in everything from our pricing to processes.

Here’s more about the philosophy at the heart of Zerodha.

AI-generated TL;DR

What are dark patterns?

Dark patterns are design practices and techniques with the express purpose of tricking and manipulating you into doing something that’s bad for you . The post explains that these aren’t outright fraudulent but operate in ethical gray areas. The author illustrates this with a story about “Kumar,” a mutual fund executive who couldn’t find the sell button on his own company’s website – this was intentionally hidden to prevent customers from easily redeeming their investments.

Why dark patterns work

The post draws on behavioral psychology, specifically Daniel Kahneman’s concept of System 1 and System 2 thinking . System 1 thinking is fast and intuitive but prone to biases, while System 2 is slow and analytical. Dark patterns bypass critical thinking parts of the brain and take advantage of emotions and tendencies like greed, fear, hope, inertia, impatience, scarcity, loss aversion, and choice overload.

Major dark patterns in finance apps

1. “Casinofication” of everything

The most harmful pattern is making investing feel like gambling through:

- Content designed to trigger greed and increase activity

- Gamification with badges, streaks, and leaderboards

- Fake urgent notifications about stock movements

- Offering loans alongside trading platforms

2. Hiding information

Financial companies systematically obscure important details:

- Hidden pricing and charges

- Making account closure difficult while opening is easy

- Advertising “free” services while charging elsewhere

3. Mis-selling

This involves pushing harmful financial products:

- Misleading loan advertisements claiming “0% interest”

- Deceptive benchmarking of investment products

- False return promises from traditional insurance

- “Algo trading” strategies promising unrealistic returns

4. Manipulative defaults

Pre-selecting options users didn’t choose:

- Auto-opting into unwanted services

- Requiring data sharing for basic login

- Default consent for cross-selling

5. Privacy violations

Excessive data collection and tracking across apps and websites, with the author noting that “tracking” doesn’t quite generate the same emotional response as “stalking” .

Zerodha’s alternative approach

The post concludes by outlining Zerodha’s “user disengagement” philosophy:

- No relationship managers with sales targets

- No stock tips (which are typically given to generate brokerage)

- Active discouragement of excessive trading through nudges and features like Kill Switch

- Complete transparency in pricing and processes

The fundamental insight is that what’s good for financial institutions is rarely good for you , and recognizing these patterns can help users make better financial decisions and choose more ethical platforms.

Really well written

Very informative 👌

Extremely good article and useful info. Worth sharing to most ”neighbors and relatives”.