This week in fintech and health | Edition #2

One good chart

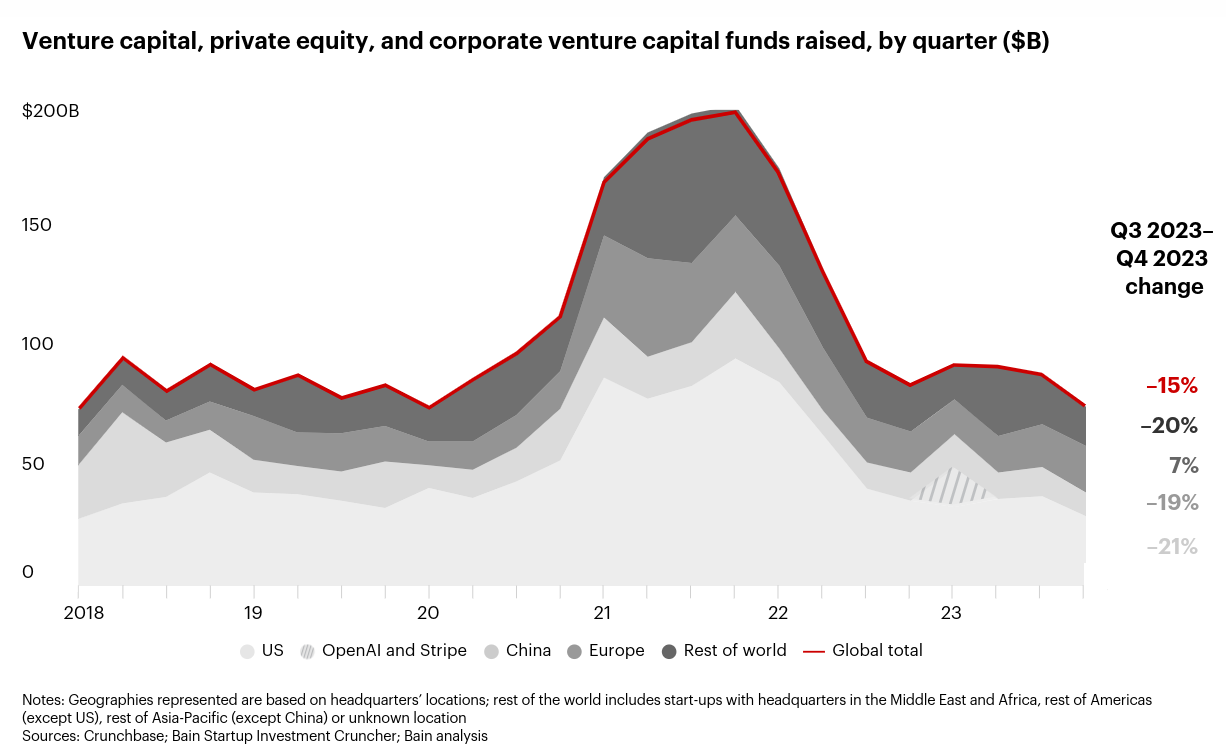

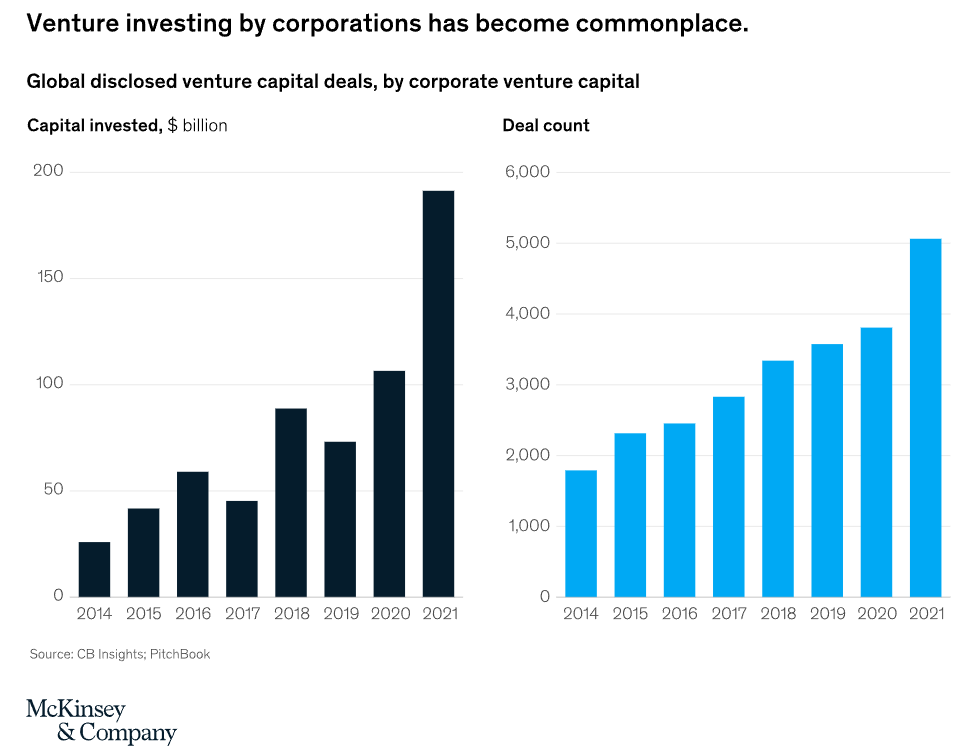

The rise of corporate venture capital

By Dinesh.

One of the biggest trends in venture investing in the last decade has been the rise of non-traditional investors like crossover hedge funds, corporate investors (CVC), private equity, and mutual funds. These plates became especially big during the post-pandemic madness bidding up deals to astronomical levels.

India has also seen a mushrooming of corporate venture investors (CVCs) and they are now sizable players in the venture capital. Anecdotally, I’d say that at least 20% of all venture deals now involve CVC investors like corporates and family offices. I’ve been speaking to these CVCs and many of them seem to have slowed down their investments. The 2020-2022 craziness is now firmly in the rearview. Terms like “due diligence” and “profitability” are sexy once again.

A few thoughts and observations about corporate venture capital. I will try to do a detailed blog on why CVCs are critical to the Indian start-up ecosystem. But here are a few pointers to remember:

- On average CVC backed startups have higher odds of survival. I’m guessing the longer term capital, strategic vision and distribution advantages that companies bring to the table is a factor.

- The incentives are a little different with CVCs. Since many investments tend to be strategic and not financial, the behavior is different.

- CVCs bring advantages like access to seasoned founders, hands-on operators, and insider industry expertise that traditional venture investors can’t bring to the table.

No banks?

By Bhuvan.

I read in a recent FT piece that Monzo, one of the darlings of the neobanking wave, is looking to raise £350 million at a valuation of £4 billion. It got me thinking about the state of neobanking. From about 2019 to 2021, neobanking was one of the hottest fintech trends. I’m more of a capital markets and wealthtech fintech guy and not a banking fintech guy. But as an amateur neobanking enthusiast, here’s what I think about the space.

The first neobanks, or digital banks, started in the aftermath of the 2008 global financial crisis as trust in traditional banks cratered. However, the adoption of smartphones was the key enabler for the rise of neobanks. By 2015, almost everyone in developed countries had a smartphone, and some of the more popular neobanks like Monzo, Chime, Revolut, and N26 had arrived on the scene.

The neobanking wave really took off in 2019, and soon VCs ploughed billions into neobanks around the world. Between 2017 and 2019, $32 billion flowed into neobanking startups. In 2023, there were over 400 neobanks globally, according to one count.

Ok, what the hell are neobanks?

A neobank, according to the accepted definition, is a digital-first bank without a bank license that partners with existing banks to provide a better banking experience. But this isn’t accurate. Many of these neobanks now have bank licenses or are applying for them.

Why do we need neobanks?

Here’s the broad sales pitch:

- Traditional banks are horrible. They have high fees, hidden charges, and horrible user experiences. You deserve a better and more modern banking experience.

- Millions of people are unbanked or underbanked.

- Traditional banks try to serve everyone and are meant for no one. We will focus on specific niches and offer tailored solutions.

Does a neobank work?

Not all neobanks are built the same. There are mass-market consumer neobanks, niche consumer neobanks, and B2B neobanks.

Consumer neobanks make sense in theory. Traditional banks have high costs because of their physical presence and compliance burden. Since neobanks partner with existing banks and don’t have physical branches, their customer acquisition costs (CAC) are lower. If neobanks do have a banking license, their costs are higher but still lower than those of traditional banks. This should enable them to scale easily and be profitable.

But reality is different. If a neobank doesn’t have a banking license, then it’s just a good-looking skin (app) on top of an existing bank. That means it can’t accept deposits or lend. The only revenue it can generate is a cut of the fees charged by the underlying banks and commissions from distributing financial products. The biggest revenue source is the interchange fee on debit card transactions, which is split between the underlying bank and the neobank.

In the US, this can be a decent chunk of revenue, due to a regulatory quirk that allows banks with less than $10 billion in assets to charge a higher interchange fee. There’s a cap on what bigger banks can charge. So, neobanks partner with smaller banks to get a bigger cut of interchange. As the financial plumbing expert Patrick McKenzie put it, “interchange is the revenue model which got a thousand pitch decks funded.”

In India and Europe, this is a smaller revenue opportunity because of lower interchange. Other revenue opportunities include commissions from selling other financial products such as loans, stocks, mutual funds, insurance, crypto, P2P investing, and so on. Revenue opportunities for neobanks are limited unless they achieve massive scale with hundreds of millions of users with decent account sizes. However, if a neobank were to obtain a banking license and then lend from its own balance sheet, the story could change. Neobanks like Monzo, N26, and Starling have all got their licenses. Revolut applied in the UK but withdrew in the US.

Logically, this is the path for the Indian neobanks, but the RBI is stingy with giving out bank licenses. Things are even more complicated for VC-funded startups because the RBI dislikes complex shareholding structures, as can be seen from how PayU has had a hard time getting a payments aggregator license.

B2B neobanks, on the other hand, work with businesses to provide them payment solutions, accounting tools, payroll software, and lending products. They earn a percentage of the transaction value for processing payments, as well as subscription fees for other tools. This is probably a higher revenue opportunity, though the competition here is just as intense as for B2C.

A BCG report hit the nail with respect to the challenges:

- Without access to deposit funding, neobanks in developed markets are under threat because the technological gap between traditional banks and them is narrowing. For example, J.P. Morgan allocated $12 billion for technology in 2022.

- Neobanks in emerging markets may fare better because of the large unbanked and underbanked populace, and banks that haven’t faced serious competition.

Here’s are a few questions I have:

- Neobanks provide amazing user experiences, but is that a good enough value proposition?

- Neobanks are still new. Will people trust them enough to be their primary bank accounts and maintain large cash balances? You could argue that people rely on mental accounting and the notion of a “primary account” doesn’t exist, but the question of trust still remains even with deposit insurance with the underlying bank.

- There are many narrow neobanks that cater to specific user groups and identities. For example, there are neobanks for freelancers, immigrants, kids, parents, people of color, the LGBTQ+ community, climate-conscious people, etc. Are these niches big enough?

- Perhaps the most important question is: can neobanks generate the kind of super-hit returns that VCs are looking for without a banking license?

- Are their models defensible if they rely on other banks? Because partner banks can pull the partnerships anytime.

- Finally, can they survive the looming threat of regulatory crackdowns? We saw this with Chime in the US, who was asked to stop using the term “bank.” N26, Monzo, Chime, and Revolut have all either been fined or are under investigation for money laundering lapses. Then there’s the PayTM saga.

Neobanks in India, US and Europe have raised huge amounts of money at astronomical valuations. Now comes the hard part. After 2022, their valuations seemed to have cooled off and fresh funding to neobanks has dried up. Chime was valued at $25 billion in its last round but shares were sold at an implied valuation of $5.9 billion in the secondary markets. Revolut was valued at $33 billion in its last round but investors have slashed its valuation by 40-46%. It will probably be the same for Indian neobanks as well. The title of a 2022 Ken article summarized it best: “For Indian neobanks, raising $900M in funding was the easy part”

We’ll look at neobanks closely in future issues. My colleague Mohit who’s a self confessed “payments guru” had some unhelpful comments which I’ve duly ignored.

Health

Is it just me, or has the number of people talking about health suddenly gone up? Mind you, I’m not talking about the number of healthy people, only people talking about health.

I feel this is a direct result of the growth of health and wellness influencers, podcasts and videos, and coincides with the whole culture of self-improvement. The fact that a term like “biohacking” has become part of mainstream culture is telling. “Live longer” is a good hook to get anyone interested in anything. People will gladly throw a lot of money to consume all sorts of sludge, as long as it doesn’t involve getting healthy the boring old way.

Short form video platforms like Tok-Tok and Instagram have accelerated this trend, spreading short snippets of information at a rapid clip. Health trends and fads alike seem to spread like viruses, with all of humanity glued to their screens. In a world without social media, short form video and YouTube, drugs like Ozempic would never be this popular.

The last biohacking trend is ‘nicotinamide adenine dinucleotide’ (NAD+) therapy. NAD occurs naturally in living cells. It’s involved in crucial functions like energy production, DNA repair and regulating circadian rhythms. NAD+ fans believe it’s a miracle drug that can do anything: slow aging, improve energy levels, perk up one’s mood, build muscle and burn fat. But, like with many “miracle” cures, the evidence is thin. — Elle Magazine

Speaking of untested stuff that can damage your liver, poison your blood and kill you like a character in a mediaeval movie, the benefits of supplements may be oversold.

“Even the best-case scenario is comparable to a marathoner shaving her head: the aerodynamic advantage is real, but it’s also meaningless.” — Outside

In the same vein, nutraceuticals have become a nuisance given their dubious miracle claims. It looks like the Indian government has grown tired of their nonsense, and is trying to regulate them. — Finshots

Silicon valley bros are manifesting psychedelics. Once part of the counterculture, psychedelic substances are now more mainstream than ever, despite questions about their legality. This hasn’t deterred VCs, who are ploughing hundreds of millions into startups experimenting with psychedelic substances like ayahuasca, MDMA, and psilocybin. — Financial Times

Here’s a good summary of a recent mega-study involving 61,000 people with gym memberships. The things that work the best to motivate people to go to a gym are financial incentives and changing the nature of the gain and loss frame. — Clearer Thinking

One of the side effects of modernity is that we get regular doses of nutritious microplastics even if we don’t want them. 🙁 Harmful microplastics have been found everywhere from the oceans, to blood, to faeces, to even breast milk. New research shows that they have invaded placenta as well. Plastics will stay by you, it seems, from the earliest moments of birth to long after death.

Investments at Rainmatter

Did you know the wheat flour we typically consume, be it wheat we mill ourselves or buy from supermarkets, is not as nutritious as we assume? Pranjal and Arjun, the founders of TWF Flours explained that most of the nutrients in the wheat grains are lost during the grinding process. Many of us on the team didn’t know this. It was surprising considering wheat is the second most consumed grain after rice. Considering that this is a large problem, it was a nobrainer for us to join the TWF team on their journey to solve this problem. Here’s a short investment note.

The line about “due diligence” becoming sexy again made me laugh; the two of us plan trips just as differently—I make a spreadsheet, while my friend books at midnight—and KnowUsWell gave us a reason to compare notes. Do you think Indian CVCs are slowing mainly because profitability matters again, or because the post-2022 funding mood changed?

I found myself taking notes while reading because there were so many points that I didn’t want to forget. Thank you for sharing such insights.