The evolution of mutual fund platforms in India

Starting around 2015–16, India saw a wave of fintech startups across payments, investing, insurance, lending, and various other corners of finance. What was interesting to me was the investing side of things and all the platforms that started by offering mutual funds.

This was also the period when India Stack started making financial onboarding easier. Aadhaar e-sign, DigiLocker, UPI, online KYC, and the broader digital public infrastructure made it possible for investing to be almost fully online. In the case of mutual funds, the experience became completely online.

This was also around the time we launched direct mutual funds on Coin in 2017. Initially, Coin had a ₹50 monthly fee. The logic was simple. When people invest in regular mutual funds, they pay commissions, and compared to that, ₹50 a month was nothing given the money people saved by not paying commissions. But India is a price-sensitive market. People didn’t want to pay even that nominal fee. So we made Coin free, apart from the fact that investing in stocks, ETFs, and bonds was already free.

When we started Zerodha with a discount broking or flat fee per trade model in 2010, the whole idea was to charge the same fee regardless of trade size. The question was simple: if the effort to execute a trade is the same, why should customers pay differently?

We used the same logic for mutual funds. We didn’t launch mutual funds until we could sell only direct, where we make no commissions from the AMC. Whatever we had to charge was to cover the operational expenses, etc., and if we did charge, which we did, it had to be transparent, and the customer had to knowingly pay it, unlike commissions in a regular mutual fund. This is why we initially charged ₹50/month and later made it free.

Around the same time, many other platforms also started offering direct mutual funds. A lot of VC money flowed into the space, and like mushrooms after a rainy day, mutual fund and investing platforms started popping up everywhere.

Most of them had roughly the same business model: offer mutual fund execution, maybe add some basic model portfolios, and then hope to eventually monetize the user base through higher-yielding products such as loans, insurance, advisory, or something else.

Even back then, this didn’t make a whole lot of sense.

The bet was that mutual funds would be the wedge. Acquire users through mutual funds and later sell them other financial products. But the problem was that the mutual fund investor base itself was not very large. Around 2017-18, there were just about 2 crore unique mutual fund investors in India—the market was tiny. Given that the product was free or nearly free, the path to meaningful revenue was fuzzy to say the least.

Soon, many of these platforms started pivoting into loans, insurance, and other things. But nothing really worked at scale.

The only business line that could generate revenue was stockbroking. A few platforms became brokers and have done quite well. But apart from broking, there weren’t many ways for these mutual fund platforms to make money.

The only other option was to switch to regular mutual funds and become a mutual fund distributor. You could make decent money. Not VC-style money, perhaps, but money.

And slowly, that is where the industry started heading.

By 2022–23, the signs were already visible. A lot of the investing platforms that had raised money were in trouble. Direct mutual fund execution by itself was not a business model. It was a subsidized acquisition strategy. And once the funding environment changed, that subsidy started looking expensive.

Today, there are only a few platforms offering only direct mutual funds. Even platforms that once championed direct mutual funds have started offering both direct and regular plans. The reason is obvious: a large user base that pays nothing is a nice metric, but if you have external investors, or if you are listed, you eventually have to show revenue. Slowly, direct mutual funds are becoming a hidden feature on platforms. Not only direct mutual funds, but several brokers that earlier used to offer free equity trades have also now started charging for them.

Quarter after quarter, you have to show growth. And it becomes hard to keep subsidizing a large base of mutual fund investors from some other business line forever. To be clear, I don’t mean this moralistically. Every business has to make money. To each business its own. This is the path some of them have taken, and that is fine.

But it’s obvious where this is headed.

Until recently, many of these platforms didn’t offer regular mutual funds. Now they do. That tells you something. They are looking for ways to monetize the investor base. Anyone with a reasonable understanding of the investing space could have seen this coming.

At Zerodha, we are in a privileged position. We don’t have the same pressures. Ever since we removed the ₹50 fee on Coin, we have had no plans to monetize mutual fund investing. We continue to believe that for self-guided investors, direct mutual funds are the best way to invest in mutual funds. It is just basic math.

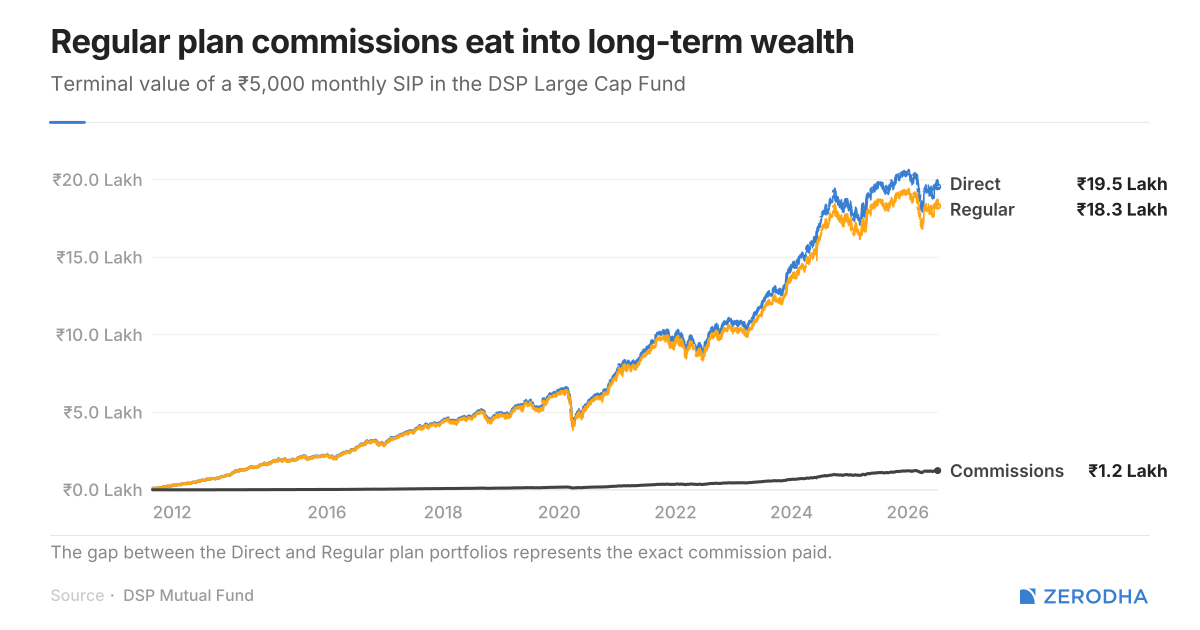

In regular mutual funds, you pay a commission. These commissions may look small in percentage terms, but they keep adding up over time. One of the most ignored ways to improve your odds as an investor is to keep your costs low.

The difference between the expense ratio of a regular mutual fund and a direct mutual fund is often around 0.5% to 1% depending on the category. That may not sound like much, but over long periods, and as your portfolio grows, it adds up. Mechanically, the larger your portfolio becomes, the more you pay in commissions.

If you know what you are doing, it makes no sense to invest in a regular mutual fund. You can invest directly and save that cost.

This is why Coin will continue to offer only direct mutual funds. We have no plans to offer regular mutual funds and no plans to charge investors for investing in mutual funds.

Coin is today the largest direct mutual fund platform in India and one of the few platforms that offers only direct mutual funds. We are also working on our financial advisory offering, and even here, we’ll only offer direct mutual funds.

The great fintech subsidy may be over elsewhere, at least for mutual funds, but you don’t have to worry about that at Zerodha.

A big thank you to the Zerodha Coin team for making investing so simple and user-friendly. The platform is intuitive, transparent, and makes mutual fund investing hassle-free. It’s great to see technology being used to empower investors and encourage long-term wealth creation. Keep up the excellent work!

how to convert regular to direct plan in m.f

Hi Vajay, you cannot directly switch from regular to direct, you will have to first redeem your investments in regular plan (this can trigger capital gains) and then start afresh on Coin.