Everything you need to know about Closing Auction Session (CAS)

Every day, stock exchanges have to determine the “closing price” of a stock. This closing price is used for a bunch of important things:

- Computing the value of the Index (Sensex and Nifty). Nifty and Sensex are calculated as (Closing Stock Price x Number of Shares = Market Cap / Base Value).

- NAV of a Mutual Fund scheme is determined by AMCs based on the closing price of the stocks.

- For F&O contracts, the closing price of the underlying stock is used for final settlement on expiry day.

It’s needed for other things too:

- For brokers to show you P&L reports, they need a closing price. For something as simple as calculating your portfolio value.

- When you pledge stocks as collateral, they’re also valued at the closing price.

Now that we know we need the closing price of a stock, let’s understand how it’s calculated. Today, the closing price is not equal to the Last Traded Price (LTP) of the last trade at the stock exchange.

You can’t just take the LTP of a stock as the closing price. Imagine a stock that’s traded actively between Rs. 1,000 and Rs. 1,010 throughout the day. But at 3:29 pm, someone sells 10 shares at Rs. 980 in a thin moment. That Rs. 980 becomes the LTP, but it doesn’t truly reflect where the market values the stock. To counter this, exchanges currently use the VWAP method to calculate the closing price.

VWAP = Sum of (Price x Volume of each trade) / Total Volume

Starting August 3, 2026, SEBI wants to redefine the manner in which the closing price of a stock is calculated by introducing a Closing Auction Session.

Why the need to change the methodology?

In the current system, the VWAP price is discovered for all trades happening via the Continuous Trading Session (CTS). SEBI believes that if CAS were to replace this, it leads to better price discovery because all buyers and sellers submit their orders into one common pool during the auction window. So instead of scattered trades happening at different times as they would during a CTS, you have one big pool where everyone’s interest is visible at the same time. Because everyone’s orders are in one pool, the closing price that emerges reflects the collective view of all market participants.

This also helps in improving efficiency for the execution of large orders. Today, if a mutual fund wants to buy or sell large quantities of shares, they have to break the order into much smaller orders to avoid moving the price against themselves. In CAS, since all orders are pooled together, a large buyer is more likely to find a large seller at the same price point, making it easier and cheaper to execute big orders.

Also, it’s a global norm. Most large markets, such as the NYSE, LSE, etc., use CAS, and these are amongst the most trusted markets in the world. It also helps index fund managers and ETFs significantly reduce their tracking errors.

What changes for traders and investors?

As a retail trader trading in equity and derivative markets, here’s what you need to know. In Phase I, the equity segment is divided into two categories:

- Category I: Stocks on which F&O trading is allowed

- Category II: All other stocks

In Phase I, CAS will be applicable only for Category I stocks; these are stocks on which F&O contracts are tarded on both NSE and BSE. This means:

- Stocks that don’t form part of CAS: regular trading will continue till 3:30 pm.

- Stocks that form part of CAS: trading stops at 3:15 pm.

- Derivatives market stays open till 3:40 pm.

For CAS stocks, here’s how things will work when trading stops at 3:15 pm:

| Session | What happens | Time |

|---|---|---|

| 1 | Reference price calculation, transition from CTS to CAS | 3:15 pm (5 mins) |

| 2 | Order entry: both limit and market orders | 3:20 pm (5 mins) |

| 3 | Order entry for limit orders only, market orders locked, random close | 3:25 pm (5 mins) |

| 4 | Order matching | 3:30 pm (5 mins) |

If you are trading intraday using the MIS product type, note the auto square-off timings effective August 3, 2026:

- Equity (stocks not under CAS): 3:25 pm

- Equity (stocks under CAS): 3:10 pm

- Equity and index derivatives: 3:25 pm

You can check the latest intraday auto square-off timings here.

Here’s a breakdown of the entire process:

3:00 pm to 3:15 pm

Between 3:00 pm and 3:15 pm, regular markets (continuous trading session) are functioning as usual. Alongside, the exchanges are also calculating the VWAP of these 15 minutes. This VWAP price becomes the “Reference” price, think of it as an indicative price that is carried forward into the closing auction session.

3:15 pm to 3:20 pm

At 3:15, the market for all Category I stocks stops. The market is transitioning from CTS to CAS. The exchange calculates the reference price during this time. The price band in the CAS session will be +/- 3% of the reference price calculated. No orders are allowed from 3:15 to 3:20 pm. If there are any open orders from CTS, they are carried forward into CAS except SL orders, Iceberg orders, and orders placed outside the price band, which will be cancelled.

3:20 pm to 3:25 pm

Order Entry Session I is opened. One can place both market and limit orders during this time. The exchange starts sharing the following information on a continuous basis: (a) indicative equilibrium price (b) total buy/sell quantities (c) imbalance quantities (d) indicative index value

3:25 pm to 3:30 pm

Order Entry Session II is opened. Here, only limit orders can be placed. Market orders cannot be modified or cancelled. This session closes randomly between 3:28 pm and 3:30 pm, this is to avoid last-minute flooding of orders.

3:30 pm to 3:35 pm

The exchange stops accepting all orders and runs the equilibrium price algorithm, in which all orders match at the equilibrium price. This price now becomes the official closing price of the stock.

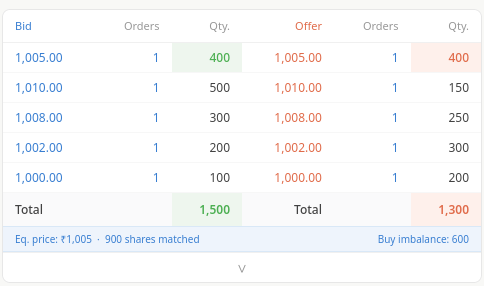

How is the equilibrium price determined?

This is the bit where it gets slightly confusing. Let us give it a shot. Let’s say the market depth for a stock during CAS looks like this:

From this market depth, one can ascertain the following:

A buyer willing to pay Rs. 1,010 will also buy at Rs. 1,005 — they’ll take any price equal to or below their limit.

A seller willing to accept Rs. 1,000 will also sell at Rs. 1,005 — they’ll take any price equal to or above their limit.

So we build a cumulative picture:

| Price | Cumulative Buy Qty | Cumulative Sell Qty | Executable Volume |

|---|---|---|---|

| Rs. 1,000 | 1,500 | 200 | 200 |

| Rs. 1,002 | 1,400 | 500 | 500 |

| Rs. 1,005 | 1,200 | 900 | 900 |

| Rs. 1,008 | 800 | 1,150 | 800 |

| Rs. 1,010 | 500 | 1,300 | 500 |

Rs. 1,005 has the highest executable volume of 900 shares, so Rs. 1,005 becomes the equilibrium price/closing price. If two prices tie on executable volume, the exchange picks the one with the smaller imbalance between buy and sell quantities. If that’s still tied, it goes with the price closest to the reference price.

If you have any questions, let us know in the comments.