Could Trend-Following Be A Successful Trading Strategy? (Part IV)

Our previous post on trend-following used cross-correlations to pick a diverse set of assets and then split the time series to arrive at asset-specific lookback periods to power a binary on/off signal. There are a few drawbacks to this approach:

- Indian rules and regulations allow a very narrow set of assets to be traded. Being selective about assets could actually be counterproductive by adversely shrinking the universe.

- Markets are dynamic. Lookback periods that work under one “regime” may not work in another. Trying to fine-tune static lookbacks could push us into a data-mining spiral.

- Binary signals introduce an element of timing luck in our back tests.

We can fix these problems by:

- Relaxing the correlation constraints by allowing most liquid assets into our universe.

- Using a uniform series of lookbacks on all assets.

- Use dynamic sizing based on trend-strength or volatility.

To be fair, these solutions drastically increase the bankroll required to run a diversified trend-following strategy. The discussion that follows assumes a maximum size of 10 contracts of the same notional exposure per asset.

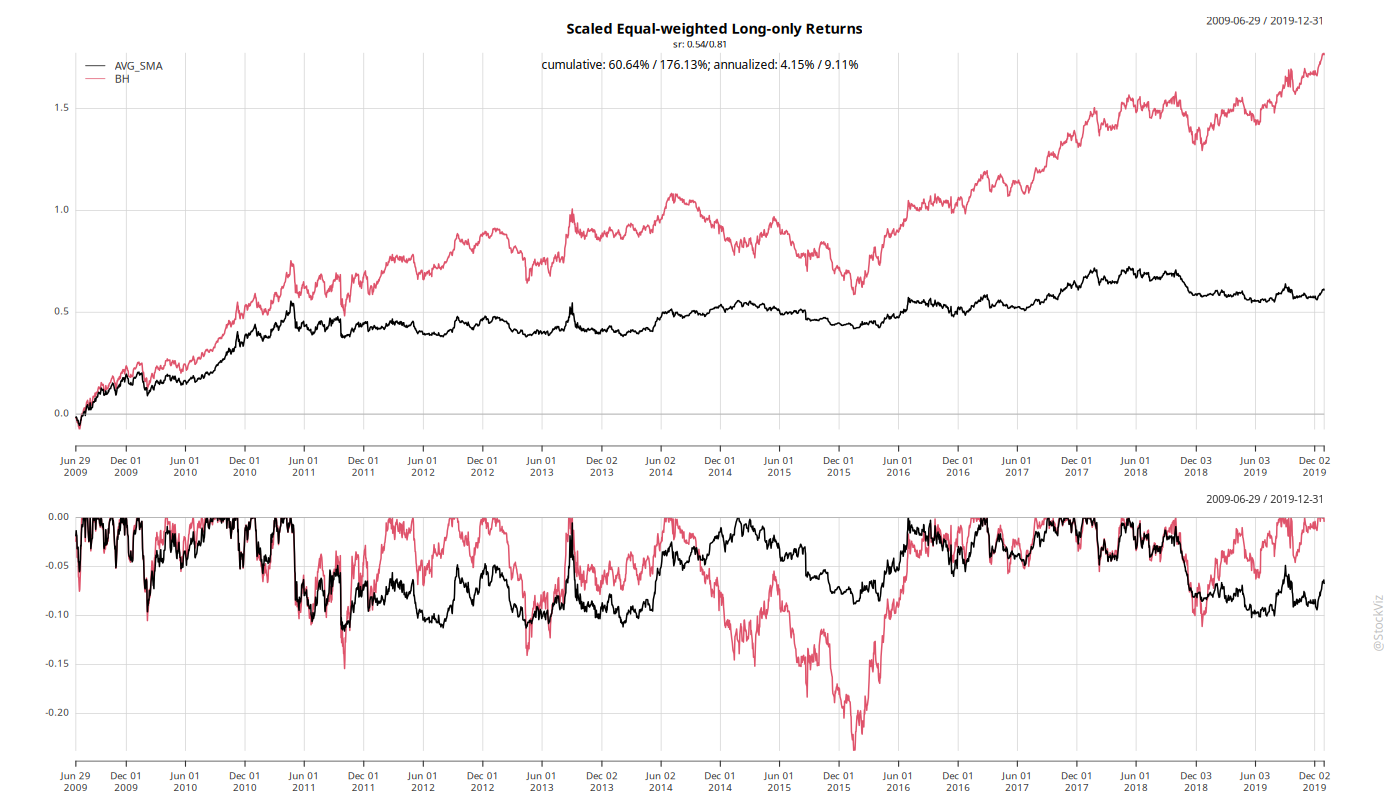

Cross-correlations on weekly time series do not tell the whole story. For example, we decided to pick one of NIFTY 50 or MIDCAP 150 based on their high weekly return correlations to each other. However, looking at annual returns paints a slightly different picture.

There have been years when NIFTY 50 and MIDCAP 50 were negatively correlated and there have been years when one massively outperformed the other. Why miss out on these years? The same goes for gold and silver as well.

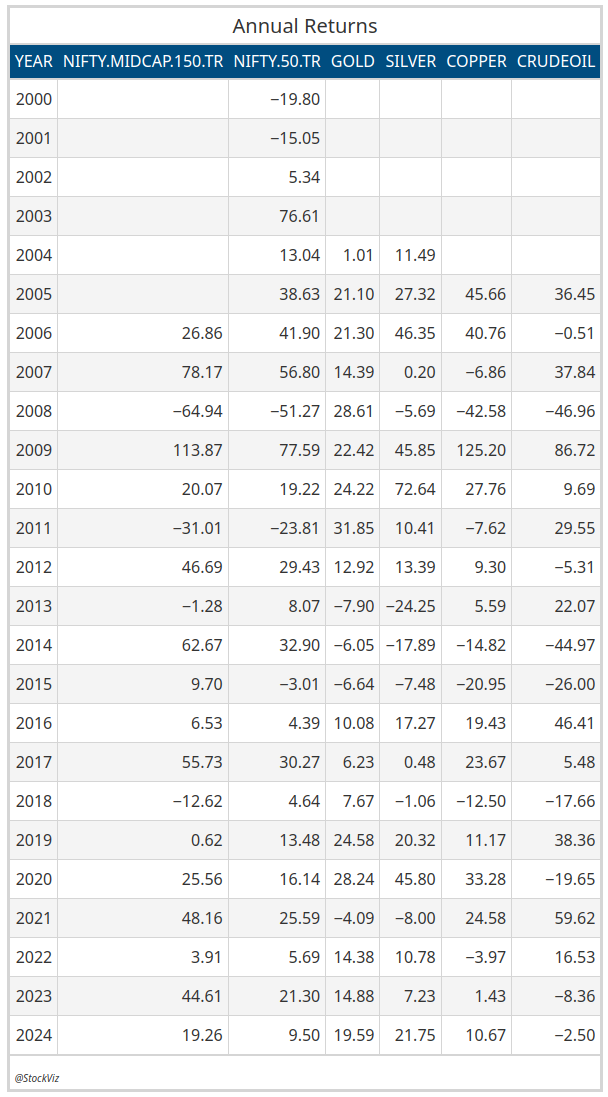

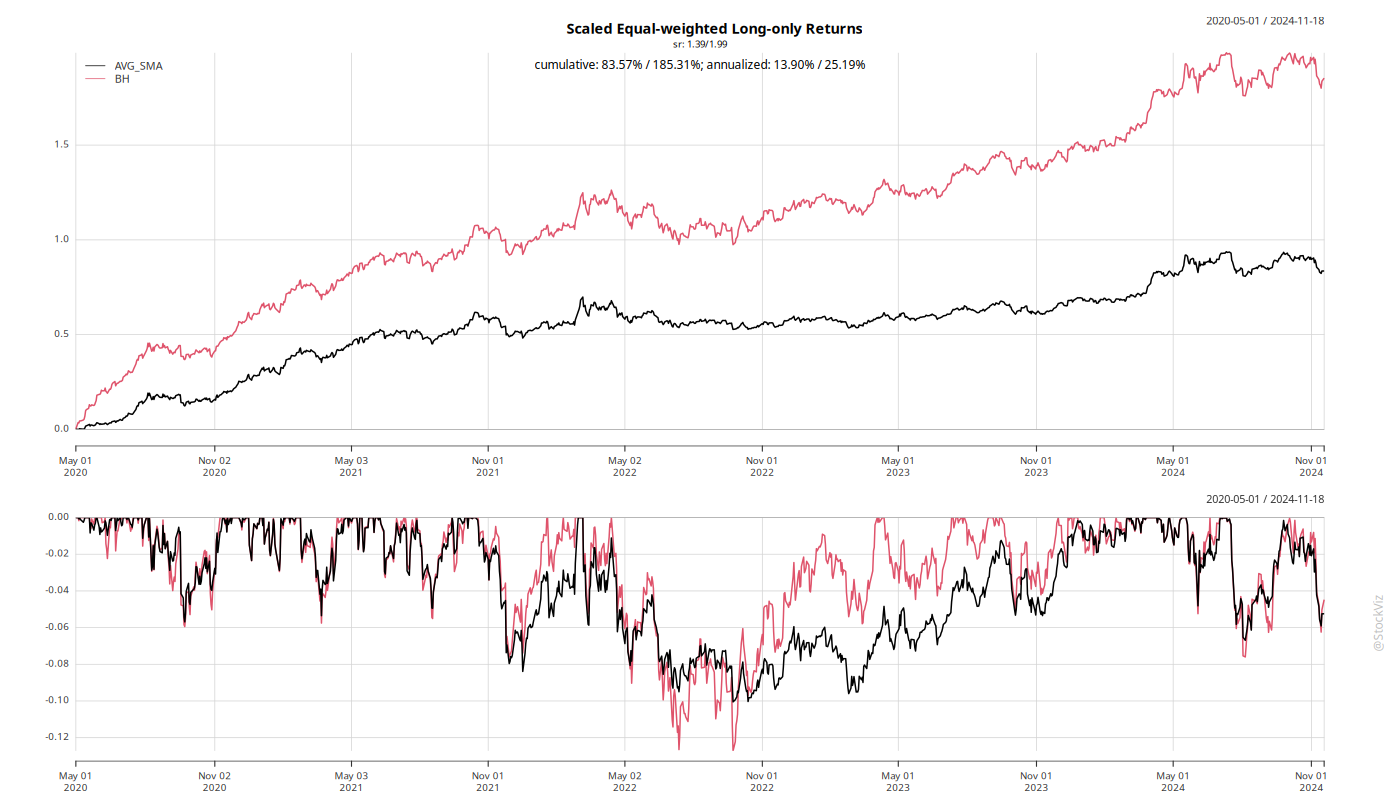

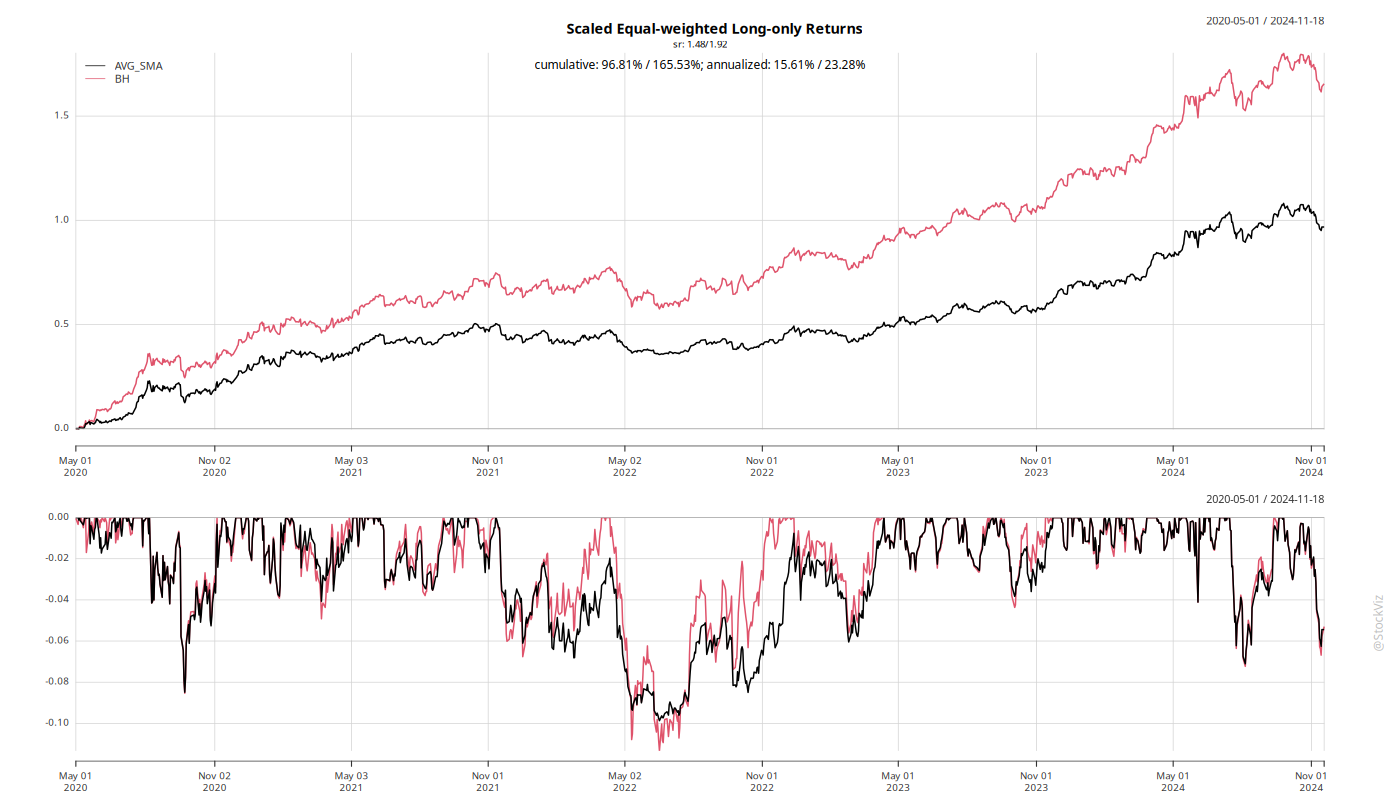

To avoid data mining, we run a 5xN SMA cross-over where N = [50, 100, 150, 200, 250, 300, 350, 400, 450, 500]. For every SMA(5) > SMA(N), you go long on one contract. Post-COVID returns, assuming transaction costs of 25bps, looks something like this:

A Sharpe Ratio of ~1.4 with a max drawdown less than 10% is pretty good for any strategy. Lever the 13.90% returns 2x and you get to a ~28% annualized return.

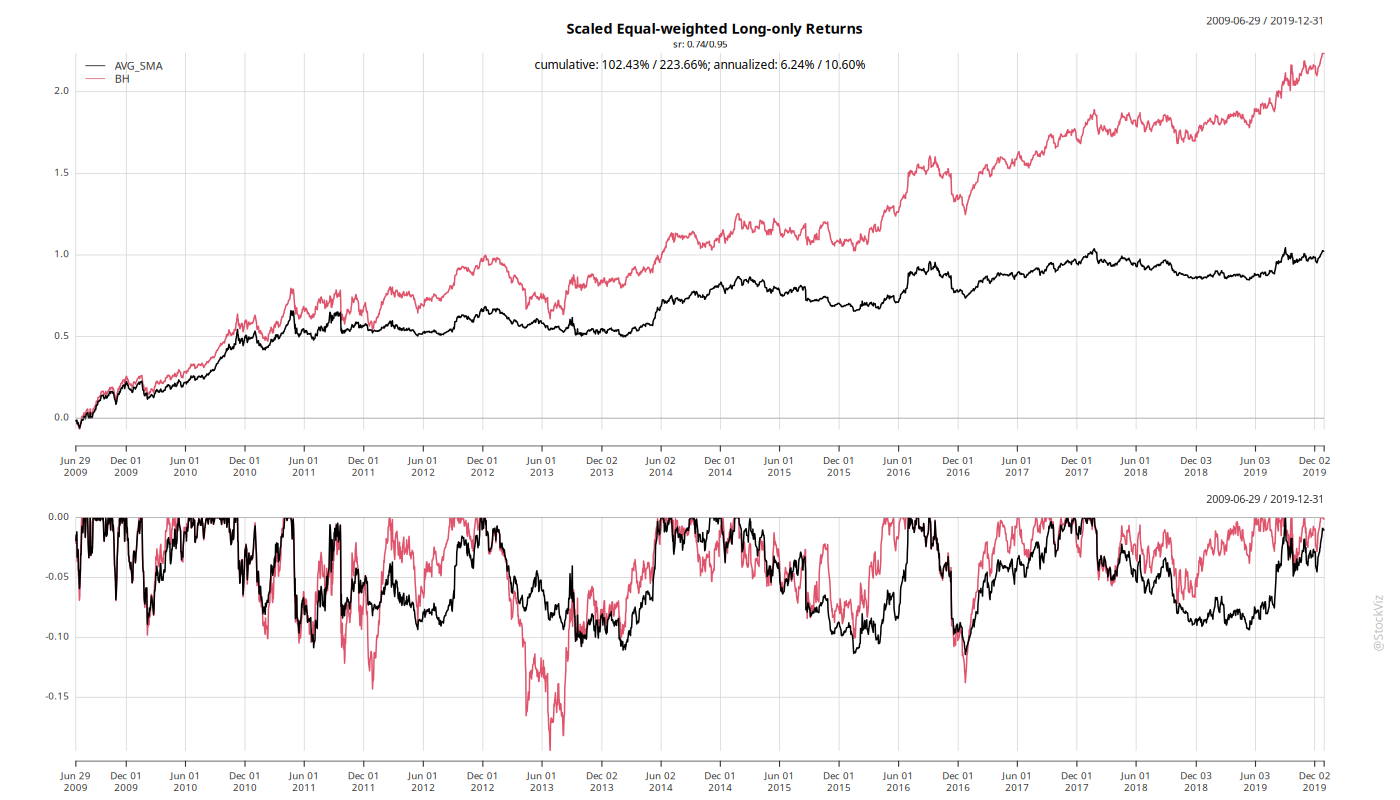

Pre-COVID returns are a bit of a let down with the strategy experiencing a lost decade.

The problem with a limited universe of assets to trend-follow is that individual assets going through a bad phase end up having an oversized impact on the strategy. Another way to frame this is that with a smaller universe, the assets you pick end up driving returns. For example, with perfect hindsight, you could drop copper and crude oil from your universe and boost performance by several points.

Post COVID:

Pre-COVID:

If you implement these strategies in the cash market using index funds or ETFs, then you will be disappointed with these return profiles. 20% drawdowns are par for the course. Why spend all this effort to reduce them and give up the upside? Diversify and chill!

Trend-following strategies make sense if you are a leveraged trader and there are assets that can be accessed only in the derivatives markets like crude oil, copper, etc. Or, if avoiding drawdowns deeper than 10% is very important to you and you don’t mind the trade-off.

Lesson: As long as you avoid data mining, there are no hard rules when it comes to trend-following. Your bankroll and asset basket dictate the strategy and outcome. Cash-and-carry investors looking for higher returns may be disappointed with trend-following strategies.