NRE or NRO? PIS or non-PIS? – Understanding NRI accounts

If you’re an NRI, managing finances in India can be tricky, especially with the various account types and investment options to consider.

In this post, we’ll break down everything you need to know about NRE, NRO, PIS, and Non-PIS accounts and also discuss why NRIs from the U.S. and Canada face restrictions on investing in Indian mutual funds.

Who is an NRI?

An NRI, or Non-Resident Indian, is an Indian citizen or a person of Indian origin who resides outside India for employment, business, or any other purpose that indicates an intention to stay abroad for an indefinite period. The Indian Income Tax Act defines NRIs based on their physical presence in India during the financial year, with specific conditions that must be met to qualify. Broadly speaking if you live outside India for 182 days or above, you are an NRI.

What Are NRE and NRO Accounts?

Non-Resident External Account (NRE) and Non-Resident Ordinary Account (NRO) accounts are bank accounts designed specifically for NRIs, to help them manage their income earned abroad and in India. The differences between the two are:

| Feature | NRE | NRO |

| Purpose | For NRIs to park foreign earnings in India | For NRIs to manage income earned in India |

| Repatriation | Funds are fully repatriable. No additional formalities. | Limited to $1 million per financial year. Must submit Form 15CA and Form 15CB, which can be obtained from their bank every time to repatriate. |

| Taxation | Interest earned is tax-free in India | Interest earned is taxable in India |

| Currency | Maintained in ₹ | Maintained in ₹ |

| Deposit | Deposits in foreign currency | Deposits in both foreign currency and ₹ |

| Withdrawal | Withdrawals in ₹ | Withdrawals in ₹ |

What are PIS and Non-PIS?

While NRE and NRO accounts are bank accounts, PIS (Portfolio Investment Scheme) and Non-PIS refer to specific types of investment routes for NRIs in India. The differences between the two are:

| Feature | PIS | Non-PIS |

| Purpose | For direct equity investments in Indian stock markets | For other investments, including mutual funds, bonds, and non-equity securities, some of which may be traded on stock exchanges |

| Shareholding restrictions | RBI has an upper cap on NRI shareholding in a company | No restrictions |

| Regulation | Governed by RBI. A PIS letter from RBI is required to make investments | Not governed by RBI |

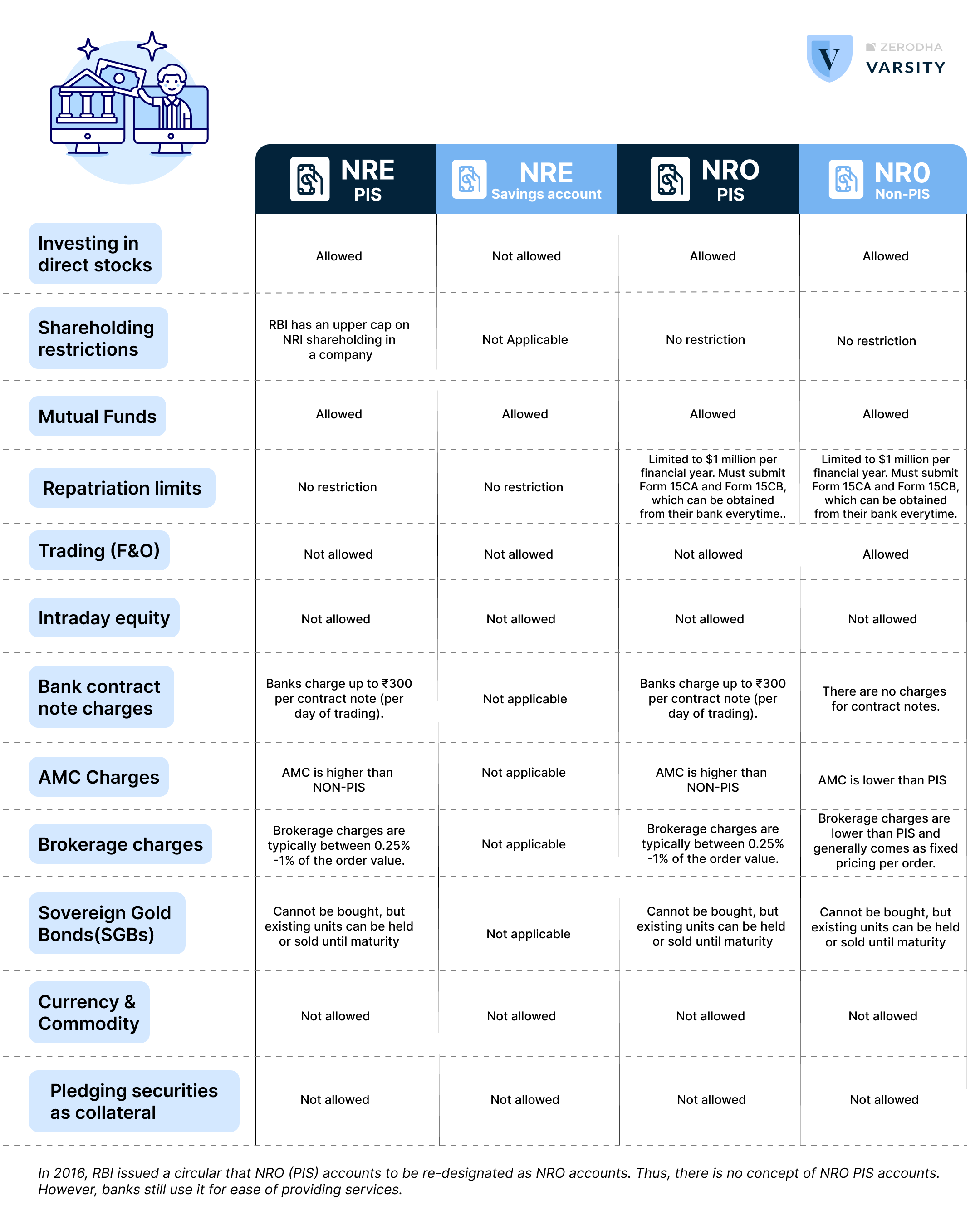

Below is a table outlining what is allowed and what isn’t for each of these accounts:

Please note that, as per the rules, the only available route to investing in equity markets directly is the NRE PIS account.

Why do NRIs from the U.S. and Canada face restrictions in mutual fund investments?

NRIs from the U.S. and Canada often face difficulties when trying to invest in Indian mutual funds due to several regulatory hurdles, primarily revolving around FATCA. The Foreign Account Tax Compliance Act (FATCA) mandates that financial institutions report details about taxpayers to the Internal Revenue Service (IRS) on a daily basis. This increases compliance burdens for the Asset Management Companies (AMCs). Failure to comply with the regulations can lead to hefty penalties.

AMCs that allow NRIs from the USA and Canada to invest in mutual funds do so with many terms and conditions. The following AMCs are some that allow NRIs from the USA and Canada to invest as on the date of publishing this article:

- Aditya Birla Sun Life Mutual Fund

- Nippon India Mutual Fund

- Quant Mutual Fund

- Sundaram Mutual Fund

- UTI Mutual Fund

- Parag Parikh Financial Advisory Services AMC

Check with the respective AMC for more details.

I work in Qatar and I do not have any income in India, I want to invest in Mutual funds only. What is the correct account type NRE or NRO account that should be opened.

I work in Qatar and I do not have any income in India, I want to invest in Mutual funds only. Please advise the correct account type I need to open with Zerodha, and taxes applicable, charges applicable.

What is costs for NRI in Stock trading ,is mutual fund also has Trading Costs ?

What happened ,if i continue using Resident account ,without taking any NRI Account in India . even I residingin abroad

Hello

Can I convert my zerodha NRO -non-pis account to to NRE -PIS account

Thanks

Prashant

I am an NRI working in dubai and I want to invest only in mutual funds through Zerodha. According to the comparison image published on your Varsity website, it is mentioned that:

Mutual funds are allowed through an NRE Savings Account

NRE accounts offer tax-free returns and no repatriation limits

AMC and other charges are not applicable for NRE Savings Accounts (as per the chart)

However, when I contacted your customer support, I was told that NRE Savings Accounts are not supported, and that I would need to open either an NRE PIS or NRO non-PIS account.

I would appreciate your clarification on the following points:

Can I invest in mutual funds using an NRE Savings Account (non-PIS), as mentioned in your published material?

If not, and mutual fund investments are only possible through an NRO non-PIS account, why is this discrepancy not updated or clearly mentioned on your website?

How can I enjoy the benefits of lower/no AMC or transaction charges, as stated for NRE Savings Accounts in your chart?

Is there any way to invest in mutual funds via NRE and still retain tax-free and fully repatriable status?

I am only looking to invest in mutual funds—not in stocks or derivatives. Please advise the correct account type I need to open with Zerodha, and how to ensure I minimize charges while retaining NRE account benefits if possible.

”Please note that, as per the rules, the only available route to investing in equity markets directly is the NRE PIS account. ”

What does this mean? Can’t I directly invest in stocks with an NRO Non-PIS account?

What happen once I come back permanently in India with my stocks in Pins Demat account? Can I open new residential demat account and transfer existing shares?

Hi Yogesh, you can convert your NRI account to a resident account. We’ve explained the process here.

Hi,

My name is Jegan and residing in Singapore.I would like open the trade account for investment. Need further assistance. Thanks!

For the NRI USA and Canada the ones that I checked in late 2023 and allow to invest in Mutual Funds are

SBI

UTI Mutual Fund

Parag Parikh Financial Advisory Services AMC

Rest in the above list were not responsive.

Being an NRI from canada it is okay for me to invest in mutual funds from regular NRO account by transferring money from NRE account ?

I am using NJ Wealth services to do so?

Please also explain on the taxation when I redeem and also if possible elaborate on TDS, LTCG or STCG RULES.

Hi paras,

Answering on behalf of our NRI team – No limit of transferring from NRE to NRO account. Regarding the tax rules, you can refer to this article

https://zerodha.com/z-connect/varsity/new-tax-rules-for-nris-starting-fy24#:~:text=NRIs%2C%20however%2C%20must%20compulsorily%20follow,formula%20of%2012.5%25%20without%20indexation.&text=TDS%20is%20a%20mechanism%20used,live%20and%20work%20outside%20India.

Can i convert my current resident account to NRO PIS without diluting my current stock and MF holdings?

Hi Ashish,

Replying on behalf of my NRI team – RBI issued a circular stating existing NRO (PIS) accounts may be re-designated as NRO accounts. As a result, there is no concept of NRO PIS accounts. At Zerodha, a resident account can be converted into an NRO account. For more details, you can email [email protected]. For accounts with other brokers we recommend checking with them.