November 24, 2023

What is Hard and Soft Underwriting?

Guest Author | Equity Investing

In May 2023, SEBI amended regulations [notification] to allow hard underwriting for IPOs in India. Before we lay out the difference between hard and soft underwriting, let us first understand what underwriting means.

The company launching an IPO can pay the underwriters a fee to ensure the IPO does not fail. In case of inadequate subscription, the underwriter buys the shares.

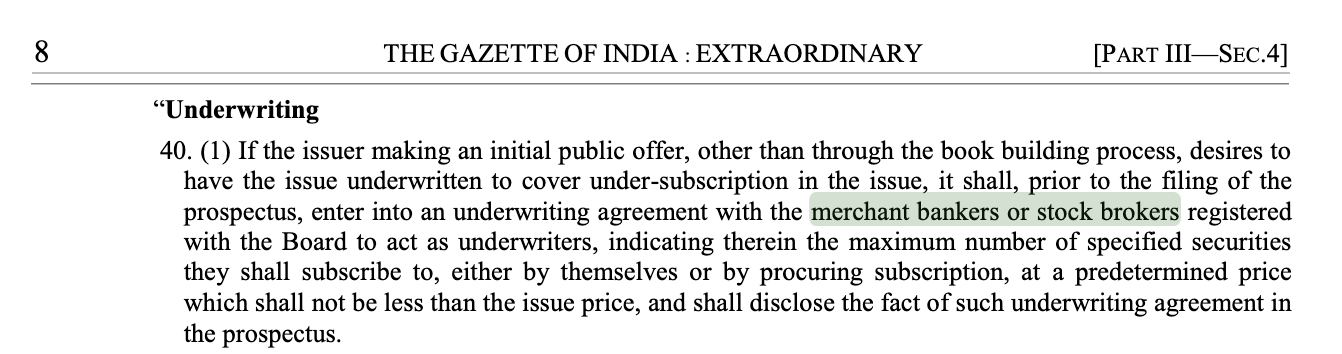

Who is an underwriter?

SEBI defines merchant banks and stockbrokers as entities that can underwrite an IPO. Here is an extract from the SEBI notification:

What does underwriting mean in an IPO?

The IPO issuer enters into an agreement with its merchant banks to guarantee that the IPO will not fail. There are two forms of underwriting – soft & hard.

In the case of soft underwriting, the risks guaranteed are lower. The SEBI consultation paper mentions this form of underwriting is presently used in India for covering payment risk in an IPO. Here, the underwriting agreement ensures the IPO does not fail if the minimum subscription is received, but payment could not be collected.

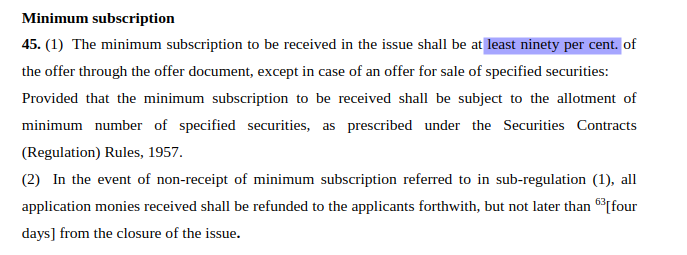

What is the minimum subscription?

In case a company is raising ₹100 in an IPO, it should at least get subscriptions of ₹90. If it fails to get a 90% subscription, the IPO will have to be forfeited. Here is an extract of SEBI’s ICDR Regulations:

However, if the company is raising ₹100 where ₹80 is in the form of new shares, and the balance is in the form of shares sold by existing investors/promoters, the offer size to be considered is ₹80. Therefore, the minimum subscription becomes ₹72 [i.e., 90% of ₹80].

The balance, i.e., ₹20, is called the offer for sale portion of the IPO.

Example of a soft underwriting arrangement

Suppose a company is raising ₹100, which is completely in the form of new shares. Now, the subscription needs to be at least ₹90 for the IPO to sail through. The company collects bids of ₹92.

In the above scenario, the IPO will be deemed successful. However, during allotment, the registrar of the company finds that 5% of the applications cannot be processed due to technical failures. Check out this post for the list of entities involved in the IPO process.

The net payment the company is able to collect after the failed applications is ₹87. The underwriter will buy shares worth ₹3, to ensure the minimum subscription requirement is fulfilled.

What is hard underwriting?

In the above example, the IPO would have failed if the subscription collected initially was for ₹80 instead of ₹92. The merchant banker’s obligation to underwrite would not be triggered. This is where hard underwriting can help the issuing company.

If an IPO is hard underwritten and is able to collect only ₹80 worth of subscriptions, the IPO will still sail through. The merchant banker will have to buy ₹10 worth of shares to bring the IPO collections up to the minimum subscription mark. The underwriting agreement could also be structured such that the underwriter has to buy shares worth ₹20, i.e., to ensure the entire ₹100 IPO collections are done by the company.

What are the benefits?

The company launching the IPO will benefit from the increased assurance of their IPO sailing through. The uncertainty from the viewpoint of an IPO investor also reduces since the merchant bank guarantees the success of the IPO. Both of these benefits come at a cost, i.e., a higher fee for the merchant bank.

Important – Just because the IPO process becomes guaranteed, it may not translate into better stock performance. The factors at play, once the stock lists, are the same.

This guest post is by Mohit Mehra. Mohit splits his time between Zerodha & Rainmatter, sharing his experiences on this blog.

Two reasons, predominantly:

1. Technical errors – Either the confirmation of the block was a false positive, or the debit attempt is failing. This does not usually happen.

2. Funds blocked in a 3rd Party Account – Let\’s say I apply for an IPO but use your bank details. Funds will be blocked and my application will seem to be successfully placed. However, when the RTA validates the bank details with the demat details i.e. when they check if the PAN is the same in both the bank & the demat, this application will be rejected because of 3rd party funding. This leads to a bigger number of rejections than technical errors.

With the availability of ASBA, why would the applications not be processed? What am I missing?

Thanks for the kind words, Gaurav.

Feeling Motivated after continuous all superb blogs