Introducing PensionBox

Most Indians will live 10–15 years beyond the traditional retirement age. Yet a large share of the workforce has no structured pension or long-term retirement plan. Over the next 25 years, nearly 20 crore people will reach retirement without adequate savings.

The National Pension System (NPS) is one of the strongest retirement products available. It’s regulated, market-linked, and encourages disciplined, long-term investing. But adoption remains low. For individuals, the process feels complicated. For companies, the paperwork and compliance requirements make Corporate NPS difficult to roll out. This is what PensionBox is trying to fix.

We’ve been speaking with Kuldeep and Shivam for a while, and what stood out was how deeply they understand a problem that affects hundreds of millions of Indians but rarely gets the attention it deserves. At Rainmatter, we’re investing in PensionBox. At Zerodha, we’re partnering with them to power our Corporate NPS offering.

What they do

PensionBox offers two products, one for companies and one for individuals.

For companies (Corporate NPS)

PensionBox manages the entire Corporate NPS setup digitally. Employer registration, employee onboarding, monthly contributions, and compliance reporting are fully automated. Companies can integrate their HRMS or payroll system with PensionBox through APIs, and contributions flow directly from salaries into employees’ NPS accounts.

For individuals

PensionBox makes NPS simple to access and manage. Users can open Tier 1 and Tier 2 accounts, set up SIPs, track their PRAN, and manage withdrawals. They also support NPS Vatsalya accounts for children and offer EPF tracking.

For Zerodha users, onboarding is even smoother, log in with your Zerodha account with no additional KYC or account opening charges. You can track your NPS investments on both Coin and PensionBox.

Getting started with Corporate NPS

EPF is only one part of retirement planning. Corporate NPS lets employers offer a long-term retirement benefit that’s easy to implement and more tax-efficient for employees.

Tax benefits (invest, gains & withdraw)

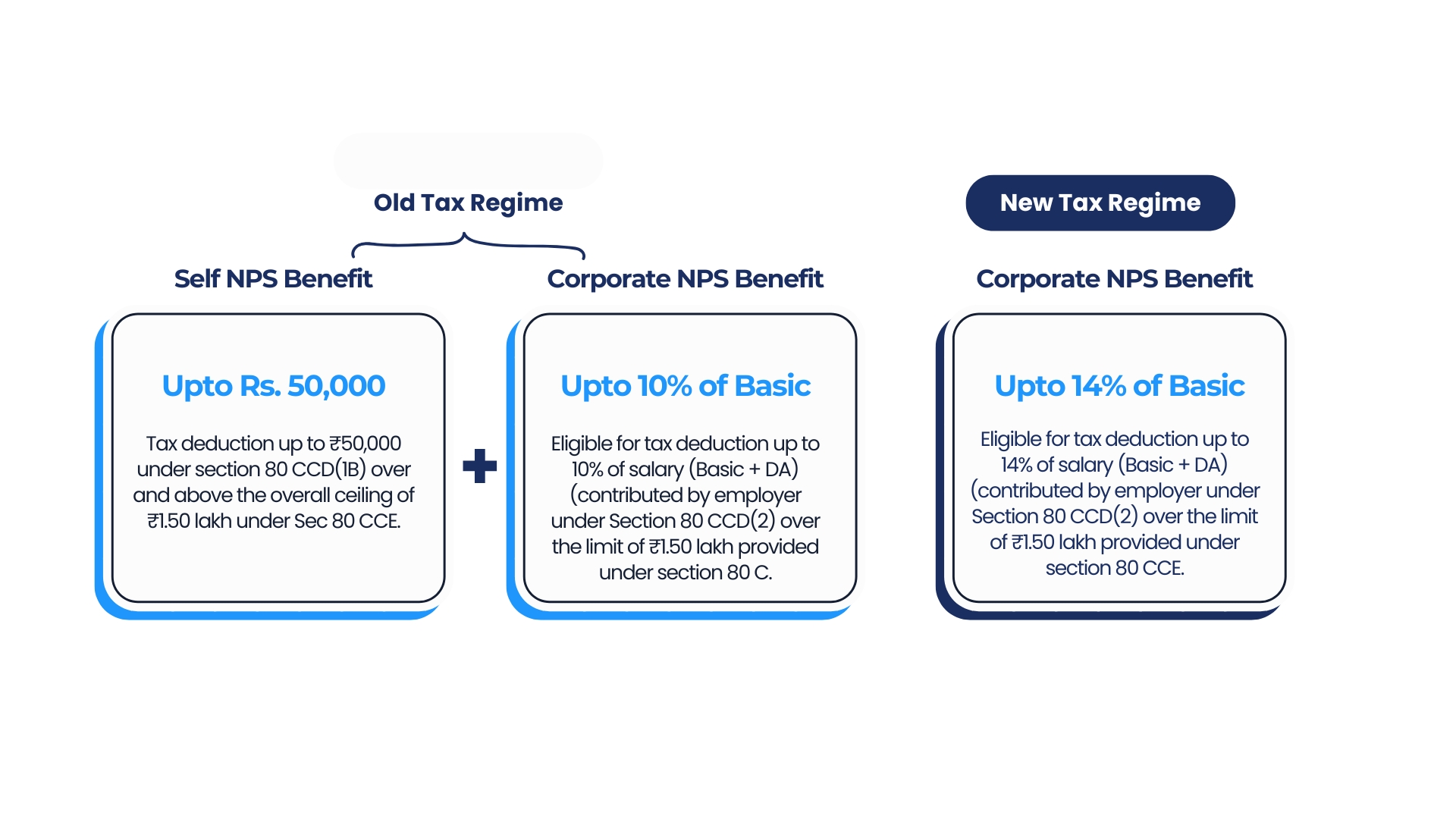

Corporate NPS remains one of the few remaining tax benefits under both the old and new tax regimes.

New regime

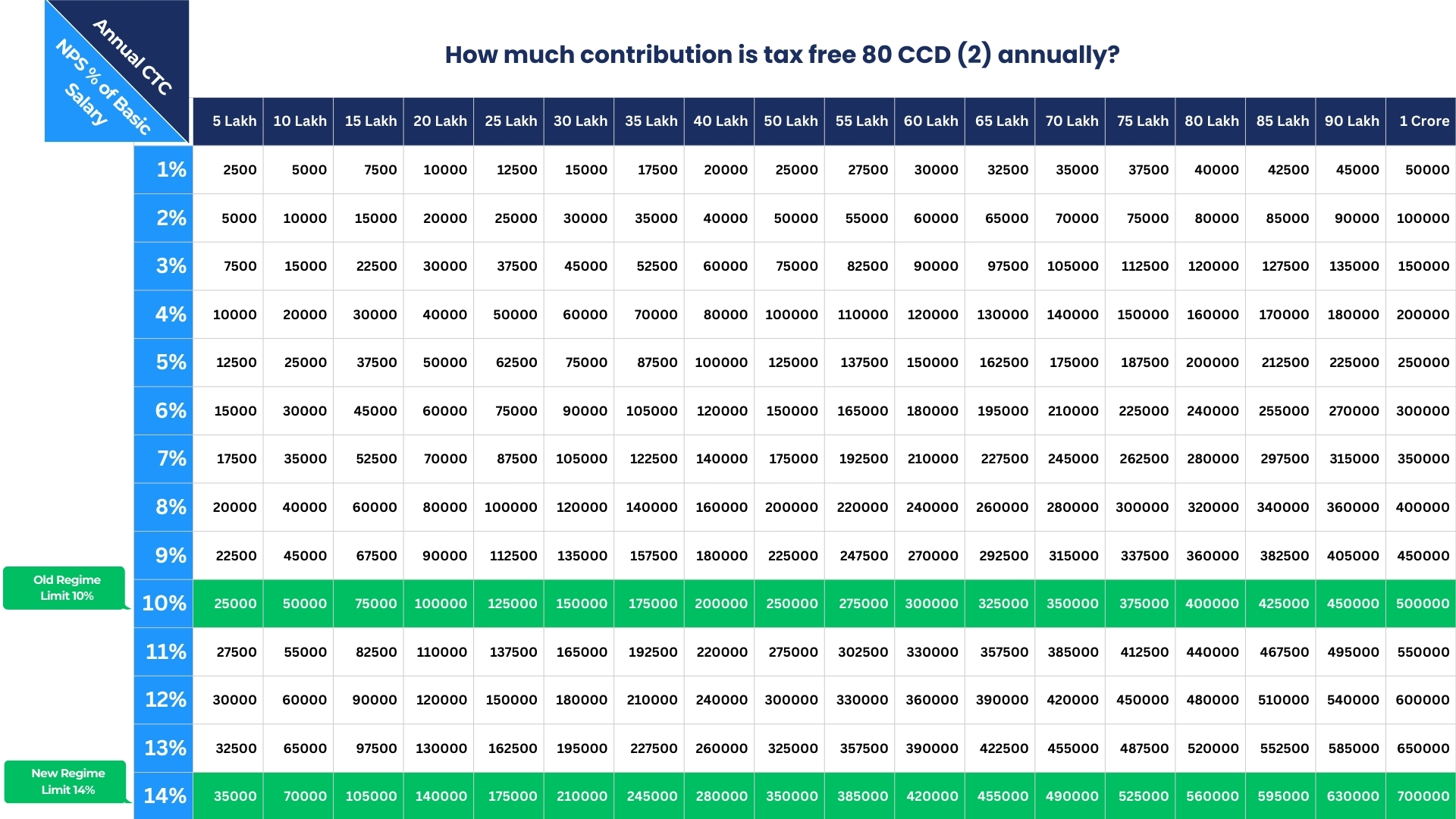

Employees can claim tax benefits on employer contributions of up to 10% of basic salary + DA under Section 80CCD(2).

(The 14% limit applies only to central government employees.)

Old regime

The same limits apply under Section 80CCD(2).

Employees can also make their own contributions and claim an additional deduction of ₹50,000 under Section 80CCD(1B), over and above the ₹1.5 lakh available under Section 80C.

(Note: NPS gains are tax-exempt. Withdrawals are partly taxed, 60% is tax-free, and the remaining 40% received as annuity is taxed as income.)

How does Corporate-NPS work with PensionBox?

PensionBox has made the entire Corporate NPS journey digital. From employer registration to integration with HRMS to monthly contribution processing, everything is paperless. Once set up, contributions move automatically from payroll into each employee’s NPS account. They also offer Corporate NPS services at zero cost to companies.

If your company doesn’t offer NPS yet, you can share this with your HR team or trigger an invite using https://pensionbox.in/workplace-pension.

If your employer already has NPS, PensionBox can help migrate the setup so that the entire process becomes digital and easier to manage.

Integrations with payroll and HRMS

PensionBox is building a broader retirement ecosystem by partnering with HRMS platforms, payroll providers, CA firms, and fintech companies. Their plug-and-play APIs allow Corporate NPS to be integrated into existing systems in a matter of weeks, helping more people start saving for retirement effortlessly.

If you’re an HRMS, payroll provider, or CA firm, you can explore partnerships and schedule a demo.

Why we are investing and partnering

Kuldeep and Shivam aren’t trying to reinvent pensions. They’re taking a well-designed, regulated product — NPS — and making it usable for both individuals and businesses. In 2025, they’re focused on scaling Corporate NPS. In 2026, they plan to expand into EPF and gratuity management, withdrawal planning tools, and solutions for gig workers.

Here’s a note from Kuldeep and Shivam

NPS is solid on paper, but the experience is broken. Companies get stuck in compliance. Individuals drown in paperwork. We realized this was an infrastructure problem, not a product problem. The validation came early. Our own families kept asking, ‘How do I actually do this?’ We built the answer.

Now we’re making it possible for any platform to offer pension services in weeks, not months.

We’re building for the security guard with no retirement plan. The gig worker without structured savings. The HR manager who wants to do right by their team but lacks the bandwidth to figure this out.

India’s retirement gap won’t close on its own. But if we can make the infrastructure simple enough that it becomes the default, we have a shot at changing the trajectory for millions.