Introducing Blostem

Booking an FD with a bank where you don’t already have a savings account is still much harder than it needs to be. Every bank has its own onboarding and KYC flow, most of which are not designed for someone who only wants to open an FD. This friction keeps most people tied to their primary bank, even when other banks may be offering better rates.

We have been speaking with the Blostem team for a while now, and what they are building is something the wealthtech ecosystem has quietly needed for years. They have taken on the unglamorous challenge of building plug-and-play banking infrastructure, starting with fixed deposits (FDs) and recurring deposits (RDs), so platforms like ours don’t have to stitch together one bank integration at a time.

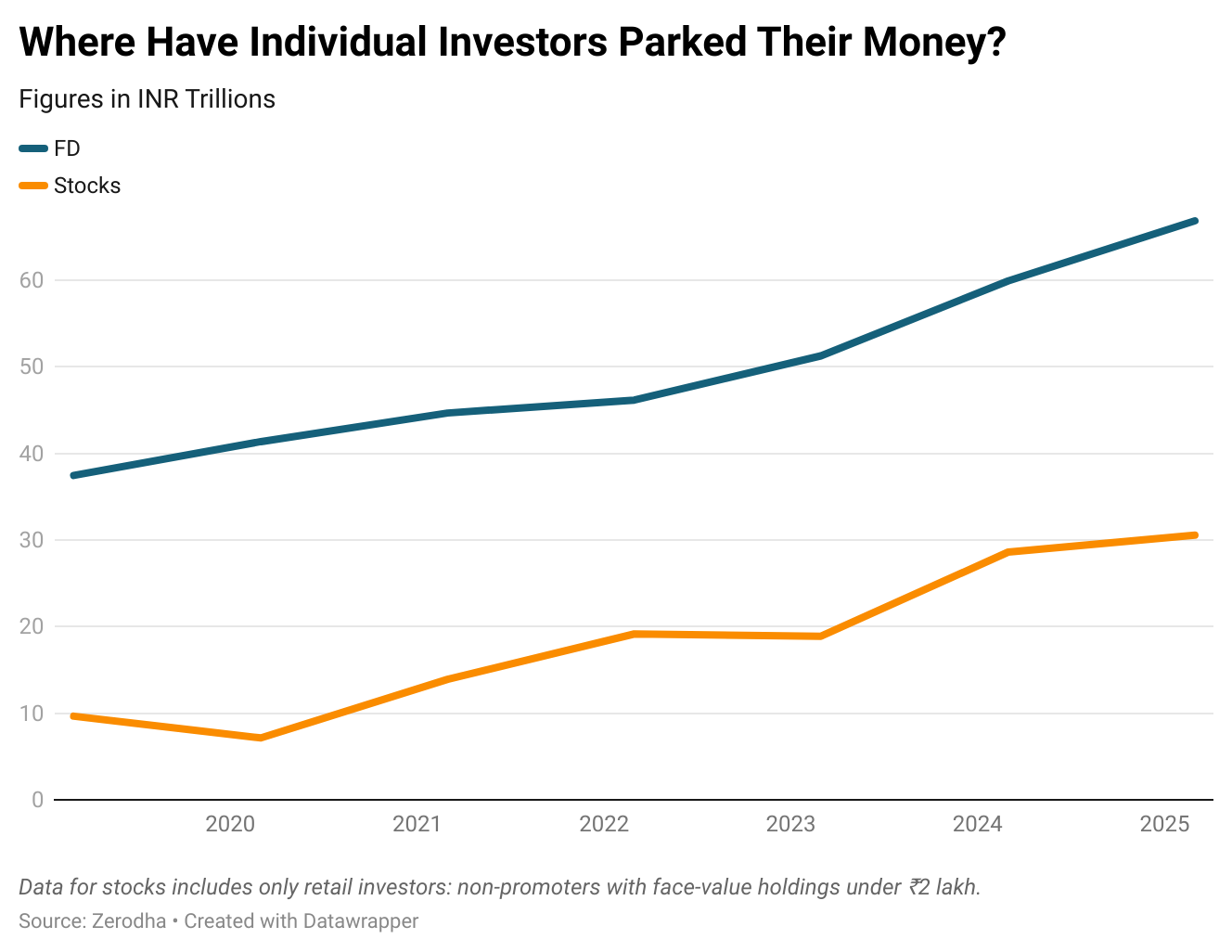

Across the fintech industry, we have all spent the last decade expanding the range of investment products available to users. Most platforms, including us, have added fixed-income mutual funds, ETFs, government securities, and more. But despite all this innovation, FDs continue to be the simplest and most familiar starting point for most savers. This story reflects in the numbers, too. As of 31 March 2025, about ₹131 lakh crores was parked in FDs with banks in India, and roughly ₹66 lakh crores of that belonged to individuals. Even after the massive bull run in stocks since 2020, individual investments still sit largely in FDs, with retail equity holdings at only about half this amount.

Over the last six years, individual FD balances have grown by almost 80 percent across very different rate cycles, while retail equity ownership has tripled from a much smaller base.

India loves FDs, but the experience hasn’t caught up

We first spoke with Blostem because we wanted to use their rails to offer FDs on Coin. As we understood their work better, we felt it made sense to back them as investors as well. As part of our effort to help people save and invest more thoughtfully across their entire balance sheet, we are investing in Blostem through Rainmatter, and Zerodha will integrate with them to offer FDs on Coin. Here are some observations we had about the FD savings landscape:

- FDs are still the default savings product in most households.

- Deposit insurance covers up to ₹5 lakh per depositor per bank. India has not seen depositors lose money in a universal bank or even a small finance bank. The same cannot be said for some co-operative banks. In practice, we see some people prefer to keep their FDs within the insured limit, which feels like a safe boundary. Unlike banks, fixed deposits with NBFCs don’t have any insurance.

- Most people simply create an FD in the bank where they hold their savings account. The best FD rates are not always in your primary bank, since each bank adjusts rates based on its deposit needs. Some people split FDs across banks, tenures, and family members to stay within insurance limits, but the process is still manual and fragmented.

On the platform side, anyone who wants to offer FDs ends up rebuilding the same painful stack. Multiple bank integrations. Different APIs and compliance processes. Reconciliation and operational overhead as a banking correspondent. For a brokerage like us to offer multi-bank FDs directly, we would need to build and maintain several point-to-point integrations, each with its own quirks. This is slow, brittle, and pulls focus away from what we do well: building investor-facing products.

This feels similar to the early days of payments. Before payment aggregators and UPI, every merchant had to deal with multiple banks and gateways one by one. Deposit infrastructure is at a similar point today.

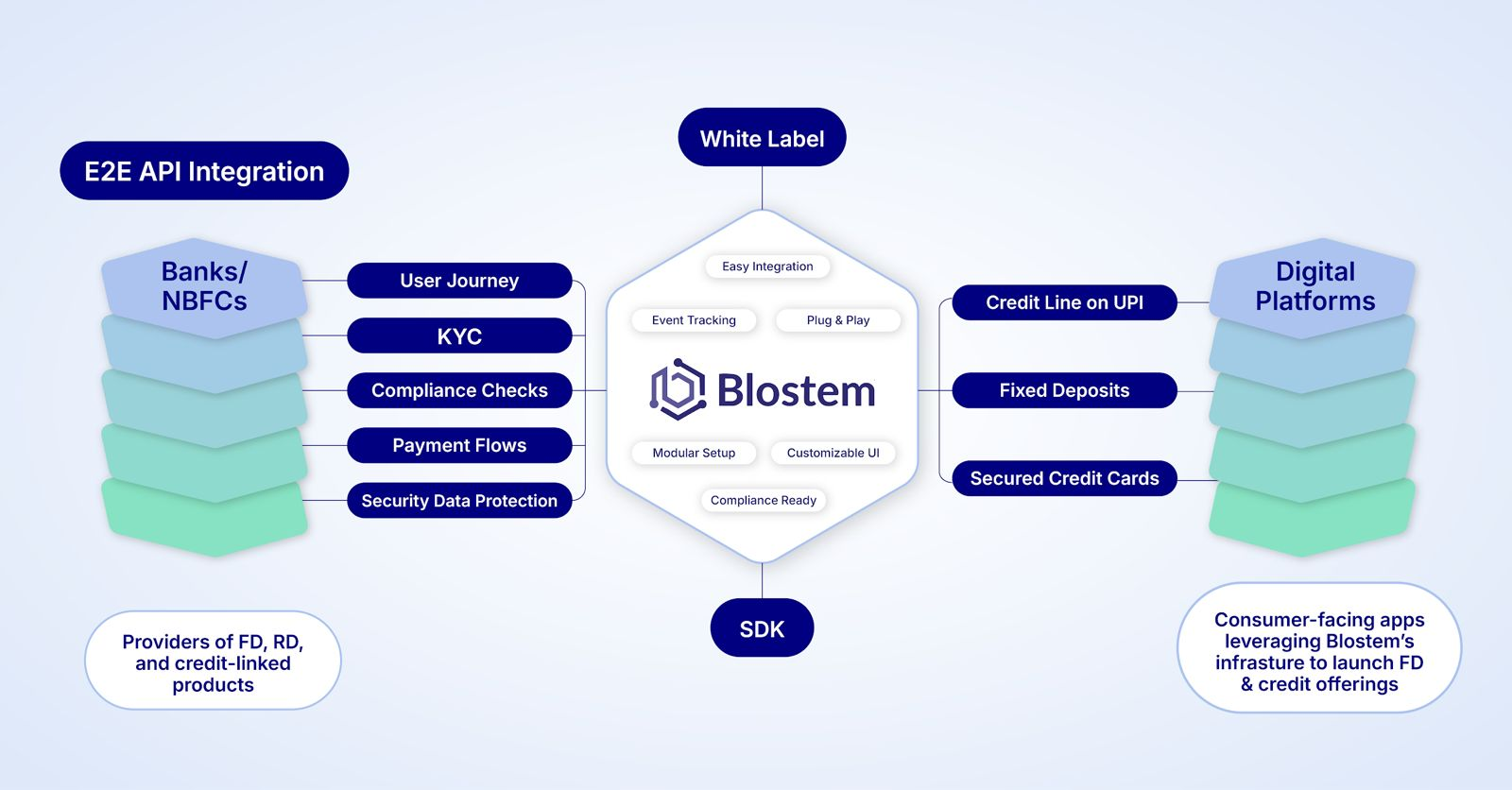

What Blostem does

Blostem is essentially a payment aggregator equivalent for banking products. They offer a single platform that lets apps offer FDs from multiple banks and NBFCs through a standardised onboarding, booking, and servicing flow.

Wealth apps, brokerages, NBFCs, and other fintechs can embed FDs without building custom integrations with each institution. Blostem is also developing other products in collaboration with its partner banks, including credit on UPI and FD-backed credit cards. Currently, Blostem collaborates with several banks and NBFCs, facilitating FD bookings through its user-facing partners. The founding team (left to right in the photo below: Sandeep, Ravi, Uday, and Pankaj) has been quietly building this for years.

Here’s how Ravi described why they started Blostem:

“We started Blostem with a simple but ambitious goal: to make regulated banking products easily accessible to every Indian through the apps they already trust and use. Today, offering something as fundamental as a fixed deposit requires every bank and fintech to rebuild the same stack— integrations, servicing, reconciliation—over and over again. It’s inefficient, time taking and prevents innovation from scaling. We knew there had to be a better way.

If payments could get UPI and equities & mutual funds could operate through exchange rails, we believed banking products—starting with FDs and adding on other products such as secured credit cards—deserved the same unified, reliable infrastructure layer. Blostem exists to bridge that gap. For us, this isn’t just infrastructure—it’s a step toward helping India save better, with choice, trust, and scale built in.”

What stood out to us is their willingness to take on the infra-heavy work required to make FDs usable at scale.

Why we are investing and partnering

FDs are still a core part of a balanced portfolio. While we keep emphasising long-term equity investing, there is always a place for predictable, low-risk instruments. FDs, especially within the DICGC limit, continue to be one of the simplest ways to do this even with smaller banks that are growing their balance sheets today.

Building this infrastructure alone is slow and painful. Every bank has its own systems, rules, and timelines. Maintenance gets harder as products grow. It takes away focus from building good user experiences and risk guardrails. Blostem already focuses on this, and partnering with them lets fintech apps piggyback on their banking relationships and co-create new fixed-income features.

Ending note

At Rainmatter, we like supporting teams building the boring but critical infrastructure for Indian savers. These are the things that make the system safer, more transparent, and less friction filled. If you are building something similar, infrastructure that helps people save, insure, or invest better in a responsible way, we would love to hear from you.

And if you would like to know more about Blostem or connect with their team, visit: blostem.com

Really interesting infrastructure play. Standardizing bank integrations could save fintech teams a lot of engineering effort.

can i go to coin and make a deposit from my HUF coin id

It’s been almost 2 months since the partnership with Blostem has been announced but we still lack the option to invest in Fixed deposit from Coin App. Also the Coin Web for investing in fixed deposits does not works. Could you please let us know some timelines by when Zerodha is planning to launch these feature’s as I am looking forward to have all my savings at the same place(Coin app).

Dear sir We are BDFI INFOTECH PRIVATE LIMITED . Sir we are service provide company like – AEPS , BBPS, DMT & CMS etc services .Sir We need Account opening api & OTHER SERVICES SO sir please provide us full Details as soon as possible contact – 8630078684