A product to get more Indians to save and invest

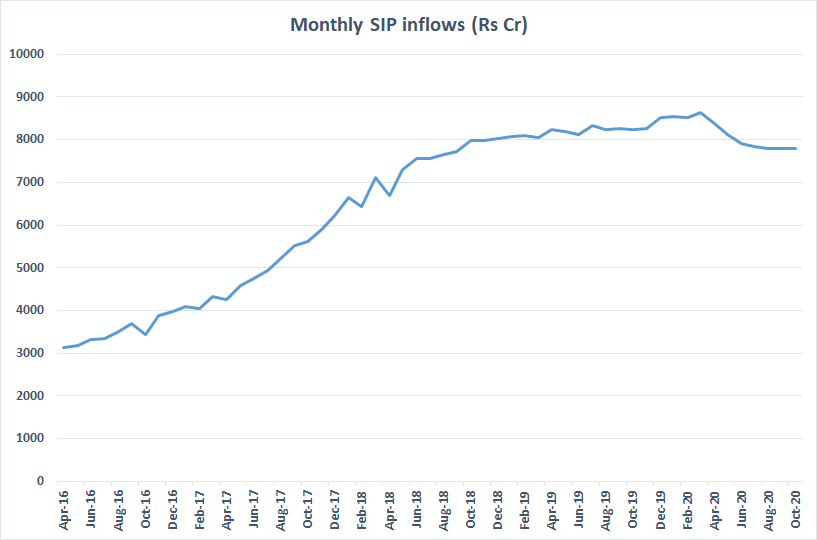

One of the biggest enablers for the growth of retail investments in India over the last 10 years has been Systematic Investment Plans or SIP in equity mutual funds. You select a mutual fund to invest in, decide how much you want to invest monthly, set up a bank ECS/NACH mandate form, and then money gets debited every month from your bank account and gets invested in a mutual fund. While there is some friction during onboarding and signing a mandate, once that is in place, it’s pretty much on auto-pilot. This automated investing has helped millions of investors build savings. The stock markets doing well in this period has also helped significantly. The industry-wide SIP book today is over Rs 7500 crores per month (the total amount that gets invested as SIPs).

Monthly SIP flows

Indian retail investors have benefited significantly by saving through SIPs. The key reason for this has been mutual fund distributors (IFAs/MFDs). They have ensured that people don’t drop off at the mandate creation step. Ensuring that SIPs are funded by automatically debiting money from the bank account is the key. If people had to manually transfer a lump sum amount every month, I’d bet that most of this SIP growth wouldn’t have happened, and more importantly, most investors wouldn’t have accumulated savings. While all of this seems great, where the industry hasn’t done well is that even today, there are maybe only around 1.5 crores to 2 crore Indians who actively invest through mutual funds or directly in stocks

And this is the question we constantly ask ourselves at Zerodha & Rainmatter—how do we grow this audience of people who are saving in India? Money lying idle in bank accounts has a high likelihood of getting spent in a world where marketers are constantly nudging us into buying things.

Stocks & MF for Indians who currently don’t invest

Saying this as a stockbroker might sound weird, but I don’t think the majority of the people who don’t currently invest are emotionally or financially ready to handle the volatility of the stock markets. While the top 5 crore Indians maybe have sufficient money or earn enough to take some amount of risk that is inevitable when investing in the stock markets, the rest of India can’t afford to take that risk. This means the potential opportunity to attract investors to capital markets is between 2 to 3 crore (20 to 30 million Indians).

The advent of direct mutual fund platforms where there is no commission paid to the distributor or IFA has now meant disintermediation and which potentially could mean lower growth of SIPs in the future. While there is the advisory (RIA) framework in place set by SEBI which is conflict-free (advisors earn only from customers and not from AMC/MF), it is extremely tough to build a sustainable business when collecting the advisory fees is difficult. Today an advisor needs to reach out to the customer at regular intervals and ask for the fees, instead of having some sort of a mandate which allows the advisor to collect the fees directly from a broker or the AMC which manages the assets (the reason why there is a vibrant advisory ecosystem in developed markets).

So, to grow participation in equity markets among the top 5% of India, I think the real problem that needs to be solved today is an easier collection of advisory fees. This needs some regulatory intervention, otherwise, the industry could potentially see de-growth in the future. Many MF distributors/IFAs are already making the shift to selling insurance policies (as there is nothing called direct Insurance plan today) as an investment product, which clearly they aren’t.

The remaining 95% of India looks mostly at real estate and gold (in the form of jewellery, the worst option) for savings. The illiquid nature of these assets makes them a poor choice, especially in times of emergency. Maybe the right product is to first help these people create some savings in fixed income products that have very little risk (like bank FDs & other debt instruments) and slowly introduce stocks/MF.

Why hasn’t any business built this?

When you talk about fixed income, the most popular product by far is the bank fixed deposit. Recurring deposits are the SIP version of fixed deposits. But recurring deposit is the least sold product by the bank. In terms of revenue, it just makes more sense to sell mutual funds or insurance policies. So, if anyone were to ever end up reaching out to a bank with an idea to save, you can be almost guaranteed that they will try to push you away from FD/RD and try and sell mutual funds or insurance policies (mostly insurance as they generate more revenue). Also, banks pay much lower interest on funds lying idle in your savings bank as compared to fixed deposits. So in a way, they have an incentive if nothing else to let the money be in the savings account itself and not even as FD.

For everyone who is not a bank, say a fintech startup, the way to build this type of product that gets people to first create savings by taking a minimum risk is by using either bank fixed deposits or debt mutual funds (liquid funds). We had attempted this as well by partnering with a startup called Balance. The idea didn’t fly for the following reasons, some of them are still valid today.

% return isn’t exciting enough

Greed or a much higher return is usually the enabler for most people to take that action of investing in equity-linked products. With fixed income, your product can’t really leverage greed. You have to create consciousness among the user on the importance of saving or having a rainy day fund. Extremely tough problem to solve.

Tough for a business to generate revenue

In equity-related products, fund houses and insurance companies charge higher fund management fees (150 basis points or 1.5%). They pass back upwards of 50% of this to the distributor. There are large businesses that have been built on top of the revenue generated by distributing equity-related products.

In the case of fixed income products, the margins drop significantly. The yields drop to less than 10 basis points, and hence, almost unviable for most businesses to sell fixed income to retail investors. 0.05% of Rs 1lk is Rs 50 or the potential revenue generated in a year by 1 client with Rs 1lk invested in debt mutual fund. Banks aren’t allowed to share a % of what they earn from the fixed deposits.

By the way, platforms that sell direct mutual funds (similar to what Coin by Zerodha offers) don’t earn anything as distributor commissions. Most of them offer the service for free and sustain themselves with backing from other revenue verticals or VC funding. For startups that don’t have any other revenue vertical, VC funding is also starting to dry up. Thus, building products selling almost zero yielding financial products is becoming increasingly difficult for startups.

Cost of fund transfers

Thanks to RBI, NPCI, UPI, the cost of fund transfers have dropped significantly. In addition, mandates can be registered online to debit funds automatically from the bank. However, the cost per transfer, albeit small, still makes this unviable for bank fixed deposits and debt funds as the revenue per transaction is close to 0. This impact is even more pronounced when the amount transferred per transaction is less and more frequent (a few thousand rupees or lesser).

Customer unwillingness to pay monthly fees

The only feasible revenue model is by charging some sort of a monthly fee for the platform. This has to be at least Rs 50 to Rs 100 per month given there isn’t a large enough customer base. But, it is extremely difficult to get fixed fees from customers. Of course, you can maybe find a few thousand paying users, but I don’t think as a country, we have 10lk Indians who will pay say Rs 100 per month for a platform like this. The only platforms that are successfully able to collect monthly fees today are around entertainment (Netflix, Hotstar, etc).

Who can build such a product?

This kind of instrument would probably need a fundamental rethink. I don’t think existing debt funds or FDs would fit the bill. Perhaps a new product that can promote the idea of savings for 95% of our population. Helping these people save in low risk fixed income products, and then when there is enough saving, enable exposure to equity. In the process help financialization of India and improve financial literacy.

In the US, platforms like Acorns and Digit are doing this quite well, but given the constraints mentioned above, the only businesses that can build such a product currently in India seem to be the banks. But given that this is probably a sub-optimal way for banks to generate revenue from customers, I doubt if this will ever happen.

For a startup looking to solve this problem, the challenge is to be able to find a revenue model. If using bank fixed deposits or liquid funds you have to charge a monthly fee from the user, which is extremely difficult considering the target audience. The only other way seems to be by creating your own fixed income products (instead of Bank FD/Liquid funds). Fixed income products with much lower risk than equity, but at the same time higher than bank fixed deposit returns, and that can generate revenue.

In the last couple of years, we have seen startups trying to build peer-to-peer lending platforms (P2P). The biggest issue though is that the risk of investing on a P2P platform is maybe as big as it is when investing directly in stocks, if not more. There are invoice discounting platforms, but a tough product for mass retail to understand.

The question we have been asking is, is there a better way to have a product that gives an upside of at least 2% more than bank fixed deposits or liquid funds, while keeping the risk significantly lower than equities? Can we then create a savings platform on top of this, which nudges people into saving as much as possible? And then, when there is enough saving, introduce stocks and mutual funds. We are exploring a couple of ideas along these lines. If you are trying to solve this problem please write to [email protected] and we would love to hear more from you.

Lovely post and comments from the commons!

For short term investment… I am waiting for Invoice discounting in ZERODHA

Sounds like a valuable problem.. Will come up with something!

”So, to grow participation in equity markets among the top 5% of India, I think the real problem that needs to be solved today is an easier collection of advisory fees”

– An alternative to solve for the ’advisory fee’ problem that you have quoted, can’t we start basic robo-advisory services for these top 5% of equity investors and then when they get used to it, start upselling advisory services by connecting them with personal advisors on a subscription basis for more nuanced investing.

This is something that the any trading app can help with. Thanks,Jatin

Why don’t more people look at Non Convertible Debentures as an option?

There is risk in every investment which should be demonstrated and understood clearly . Investors are afraid to invest beyond FD but they invest in Gold Bhisi schemes in Goldshops . Also there are people who give away hard earned money they lend to different borrowers who use these borrowed money as working capital in their respective businesses like real estate, sweet shops, hotels etc.

Lot of money is invested in such dealings. Which means investors are readily taking this unseen risk as they are investing in this unsecured , unorganised business which fetch them more than Bank FD nd they feel though there is risk element returns are sure by way of getting interest on a monthly or a quarterly basis & over maturity of term they continue to renew as this is rolling monies. Do we know size of this segment !!!! If these investors are investing in these options how can we pull them to straight to fundamental stocks, diversified mutual funds & show them the returns in form of dividend & growth vis-a-vis interest which they earn.

Rather than looking at FD investor the same investor is investing in such unorganised investment option !!!! How can we educate them & bring to organised canvas!!!

Everything have ”risk” the thing is our perception to it if you have FD or even SB in LVB or Yes Bank or with any other bank who

went to the process of moratoriumm.

Your perception of risk might go up due to withdrawal cap and so on.

HELLO!

I hope you would read this 🙂

There is numerous small business typically street-side vendors

they fulfil the finance requirement from private financiers at a rate of more than 40-50%. they aren’t financed by a bank or NBFC

what if we grab this market

To understand this, you should know about the Jagananna Thodu scheme by the chief minister of Andhra Pradesh scheme to provide an interest-free loan of Rs 10,000 to street vendors and other small traders.

My idea is all about the raise the capital through the SIPS and the raised capital will be distributed through the government to these vendors or self-help groups at a very low rate. repayment along with principal and interest on a monthly basis

advantages: compounding effect, monthly payments on time, easily disbursement and no competition

risk management: guaranteed by the state governments on the principal and interest up to a certain rate

investors got no worry because it is guaranteed by the state governments and high liquidity easy to redeem

sounds bit complicated, this all the basics of my idea

thank you

Pl explore Arbritrage products available due to Multiple Future contracts and Option hedging products. if branded an marketed properly, this would fetch rate of return above FD and below equity.

Can you offer a product wherein your principle is locked in a FD and monthly interest earned is invested in a MF or smallcase? If you can tie up with government banks offering SCSS to introduce SIP/smallcase to their senior citizen customers on a small portion of their monthly interest earned, I feel there is potential there. Banks can offer higher interest if the customer agrees to invest a portion of his monthly interest on SIPs.

Cheers,

Arun

Please see Kotak Equity Savings fund. A similar model can be adopted.

Gold , Silver & USD is the option which is secure and slightly higher than FD ,a guaranteed (in the form of pdc) income can be given and the profits & loss over and above can be proportionally distributed amongst investor and managers .

A product with barbell strategy will work ( e.g. 80% in Fixed instruments , 20% in Equity) will give 2% additional return if equity earns 15% per annum. But the challenge here would also be linked to the duration of the investment.

Think like a start-up. Allocate risk capital.

Insure the product – use an external insurance company.

how robust does your investment strategy look on back testing?

so the product offers an upside of market linked returns.

Indians love insurance– you like it or not.

and the product offers an ”assured” FD++ return. Keep a benchmark FD.

Announce a lockin period….3/5 yrs — earlier withdrawl => same return as bank FD.

The lure of insurance remains the topping.

You should check out growfix.in, it is something I have been looking at for quite a while but have not invested in because I am not sure if it would work. If someone like Rainmatter were to evaluate that and find it suitable (and hence offer it to customers or even recommend it otherwise), the fears of many would be allayed (including me).

Disc: Not associated with growfix or invested in it in any way.

As far as I could understand, Growfix doesn’t offer downside protection for the capital. While looking for the product for the next 2 crore people, returns coupled with capital protection will be imperative to bring people on board.

Another thing to consider is the prime lending rate vs savings account in countries like USA.

Debt and liquid funds could be a good idea to start a change with these another 2 crores. No risk in liquid and very less in debt if we pick up the right fund.

Looking at Franklin Templeton disaster in debt market, this one is also in a grey area

Hello sir

I think a product/scheme which invest in index,gold and secured bonds might be the right combination to beat FD rates and still have less risk than stocks or mf.

When more and more people get financial knowledge they will slowly invest in MF and stocks.

For that these ways might be useful.

Thanks with regards

Praveen

people go for FD not because it is ”Less risk” but because they think it has ”No Risk”. So the fund Nithin suggesting here wouldn’t have any direct relation to stocks.

Have you checked out the All Weather smallcase? smallcase.com/awi – top 100 equity index, gold & fixed income exposure with low-cost ETFs