Introducing the Zerodha Multi Asset Fund

If you ever feel like the stock market is an overwhelming place, you’re not alone. Every day, we’re bombarded with information: “buy this stock,” “sell that one,” “this expert predicts a crash”. It’s enough to make anyone feel like they’re overwhelmed and a step behind.

It’s easy to believe that successful investing means you have to be a genius stock picker or a market-timing wizard. The good news is that’s not the case. Asset allocation matters most for portfolio returns, not security selection or market timing. A famous study showed that asset allocation, that is, how you divide your investments across different asset classes, impacts your overall returns far more than picking individual securities or trying to time the market.

Their main finding of the study was that the asset allocation decision explained roughly 90% of the variation in portfolio returns over time and that security selection and market timing accounted for only a small portion of performance differences.

In short, according to the study, it’s asset allocation that is the primary driver of investment performance and not the picking of individual securities or market timing skills.

Let’s dive a bit deeper into this….

I know, “asset allocation” sounds like financial jargon. But it’s just a formal way of saying, “Don’t put all your eggs in one basket.” It’s about owning a thoughtful mix of different types of assets because they behave differently during the market’s inevitable ups and downs.

Why is this so important?

This is crucial because, as historical data shows, the top-performing assets change from year to year—a pattern clearly illustrated here.

Hence, to guess next year’s winner may require a crystal ball!

Therefore, a wiser & simpler approach is to own a piece of the key asset classes, i.e., have a well-diversified portfolio across various assets and segments. A well-diversified portfolio might not capture the dizzying highs of the single best asset in a great year, but it may provide better risk-adjusted returns over a longer term. In simpler words, it turns a rollercoaster into a much smoother, more manageable ride.

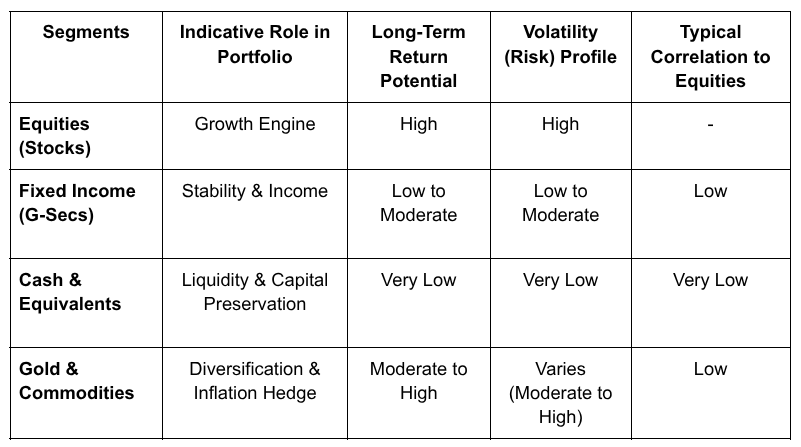

So, what are these different types of assets? Each asset class has a specific job to do within your portfolio. Think of it like building a team, where each player has a unique skill. It’s good to start with the simpler & the popular ones first, i.e., equity, debt, and gold, and at a later point, once your portfolio is stable and meeting your stated objectives, you may look at adding more exposures like international securities, etc.

Here’s a simple breakdown:

Looking at general market history, we’ve seen that stocks act as the engine for growth, though they are known for their bumpy ride. G-secs and cash have typically played the role of shock absorbers, and gold has frequently served as a cushion, holding its value when other parts of the market are uncertain.

Let’s be honest: The hard part

In theory, this all sounds pretty straightforward, right? But in practice, this is where most of us get stuck.

How do you choose the right mix? The sheer number of choices can lead to a situation where you get so stuck trying to find the perfect mix that you end up doing nothing.

Can you stick to the plan? Once you find the mix, you might face a situation where the asset allocation changes due to market corrections. The real challenge is rebalancing—selling some of what’s gone up and buying more of what’s gone down. It feels completely counterintuitive, but it’s crucial for managing risk. It takes a lot of discipline to do this consistently.

Do you have the time? Honestly, managing several different investments, tracking them, and dealing with the rebalancing and taxation is a chore most of us would rather not have.

Our approach is a simpler solution

If we know asset allocation is vital, but doing it yourself is a hassle, what’s the answer?

This is the exact problem we wanted to solve for you when we launched Zerodha Fund House. We believe that simple products can be powerful tools. That’s why we focused on creating a straightforward approach.

We designed the Zerodha Multi Asset Passive FoF, a 4-in-1 fund that invests across Equity Largecap, Equity Midcap, Gold, and G-sec ETFs in a predefined allocation that does the heavy lifting for you. It invests in a predefined mix of ETFs that aims to take an exposure of close to:

- 30% in Large Cap 100 ETF—following the top 100 index, which consists of companies that are generally considered the market leaders of their respective sectors

- 30% in Mid Cap 150 ETF—following the Mid Cap 150 index, which gives exposure to companies with relatively higher growth potential

- 25% in Gold ETF—tracking gold, which acts as a hedge against equity market uncertainty

- 15% in 8-13 Yr G-Sec ETF – investing in government securities with an aim to provide further stability to the portfolio

The fund aims to maintain this balance for you, offering a diversified and tax-efficient approach to long-term wealth creation in a single investment.

The most important takeaway

Here’s what I really want you to take away from this: The strategy is more important than any single product.

You can use the ideas and the allocation mix we talked about as a starting point or a mental model for building your own portfolio. The goal is to understand the why behind it. If you build it yourself with underlying assets of your choice, you’re still applying the same powerful principle.

Asset allocation is a big topic, and my goal was to start a conversation. We’ve only scratched the surface. There are nuances around how your allocation might change with age, your specific financial goals, or your personal comfort with risk.

– Vishal Jain, CEO Zerodha Fund House

To prevent unnecessary cost due to rebalancing, our investment strategy would be to maintain individual allocations within a 5% band of the proposed mix. Further, please note that the exposure mentioned above is only an intended illustration, and the actual exposure may vary depending on various factors.

Note: Please refer to the SID for the Asset allocation pattern of the Scheme which is 50% – 70% in Domestic Equity ETFs/Index Funds, 10% – 20% in Domestic Debt ETFs/Index Funds, 20% – 30% in Commodity ETFs & 0% – 5% in Debt Securities and Money Market Instruments.

Views are personal.

Please note that this article or document has been prepared on the basis of internal data/publicly available information, and other sources believed to be reliable. The information contained in this article or document is for general purposes only and not a complete disclosure of every material fact. It should not be construed as investment advice to any party in any manner. Please consult your financial advisor. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers shall be fully liable/responsible for any decision taken on the basis of this article or document.

I wonder if it makes sense to invest.

I am not able to invest in this fund. Getting a message “New investments have been stopped for this fund”. Could you pls help me with this?

Hi, the subscription period for this NFO has ended. The fund will reopen for investment on August 20th, and you will be able to invest after that date.

I have some money left in my pocket, should I invest?

can I still invest

Hi Raghu, the fund will reopen for investment on August 20th, and you will be able to invest after that date.

By investing in ETF’s, is the expense ratio been doubly charged?

Is the TER for the fund announced yet?

Hi Subhash, not yet. TER will be announced soon. You can keep track here: https://www.zerodhafundhouse.com/multi-asset-passive-fof/?source=home-announcement

Tax implications <=2 years:

In below case if someone is earning < 12 lakh is he exempted as per new tax regime?

Investment period <= 2 year

Gains/profits are treated as short-term capital gains & taxed as per your tax slab (plus 4% cess and surcharge, if any).

Wondering How frequently the rebalancing will take internally in the fund? is there fixed interval / Date?

Why are you investing in etfs and not direct equity? Will liquidity not be a problem since most etfs in India are too illiquid for a fund house to invest in?

Zerodha me Mera investment 10k kam dikh rha hai, ek din pehle ke compare me, bina buy or sale kiye….Do something

What will Zerodha do in this? If your portfolio stacks prices open low, automatically there will be a price difference.

stock*

Hi,

It would be good if there is some allocation to SILVER as well along with GOLD in this fund.

Why are you investing in etfs and not direct equity? Will liquidity not be a problem since most etfs in India are too illiquid for a fund house to invest in?

Why is it called FOF and not the mutual fund?

Is it investing in the existing funds and not directly in securities?

Whats the Historical ROI?

Hi Kaushal, the fund will invest in existing ETFs with exposure to Nifty 100, Nifty Midcap 150, Gold and Government Securities. Please check out the above post for more details.

Since this is a FoF, does it mean that the expense ratio will be the combination of the expense ratio of zerodha multi asset mutual fund as well as the expense ratio of the underlying funds?

Also, what do you mean by haircut of 9%?

Thanks

What would be the expected rtn over 3Y & 5Y period?

Is there any lockin period ??

Hi,

There is no lock-in period for this fund.

Thanks.

What is the expected expense ratio?

What will be tax?

Can we pledge for ’Zerodha Multi assset fund’ as collateral for our F&O positions?

Hi, you can once it is approved by the Clearing Corporation. You can keep track of all the approved securities here: https://zerodha.com/approved-securities#tab-noncash_equity

Is it possible to invest in NIFTY BEES as SIP in coin

can you share last 20 years stats of this?

You can check the data here – https://www.zerodhafundhouse.com/multi-asset-passive-fof/

What is the total expense ratio for this fund? Since it is a fof I expect it to be more.

The most important question.

What is the expected range of returns for this fund?. How is the taxation ?

Hey Geetha,

Considering the exposure the fund aims to take, it will be taxed as a hybrid fund. If the holding period of your units is more than 24 months then the capital gains will be treated as long-term and taxed at 12.5%. If the holding period is less than or equal to 24 months then the capital gains will be treated as short-term and taxed at slab rate.

Ling term capital gain is 15% not 12.5 %

Nice one . Can we do SIP in this

Hi Devi, you can invest in NFO now on Coin; this will be a lump sum investment. Once the fund opens for continuous purchase (within 5 business days from 8th August), you can start SIP.

If i want to invest through zerodha then would you be doing it and if yes what would be your commission

Hi Priyanka, you can invest in this fund on Coin: https://coin.zerodha.com/mf/invest?nfo=show There are no charges for investing in mutual funds.

How to invest. Please advice

Hi Sivaramakrishnan, you can invest in NFO on Coin: https://coin.zerodha.com/mf/invest?nfo=show

Sir,Am happy with our excellent Zerodha.com.

How much returns can I expect for one year.

What is the tax treatment of this fund? Also, I feel that allocation to gold is quite high, what data do you have to suggest that such a large allocation to gold is a good idea? What is time horizon for such an investment?

Hi Rakesh,

Considering the exposure the fund aims to take, it will be taxed as a hybrid fund. If the holding period of your units is more than 24 months then the capital gains will be treated as long-term and taxed at 12.5%. If the holding period is less than or equal to 24 months then the capital gains will be treated as short-term and taxed at slab rate.

Now indian government has recognized crypto asset and tey to regulate that so, why u are not interested to expouser in crypto upto 5 % to 10% to scheme….

If no then you are not different from others…

You are not brave to earn but you are eligible to interest for collect expense on overall volume..

Do new men,, we all investor want some innovation…

Otherwise you also explained us inflation effect on scheme to longterm return fir your scheme failure…..

Calm down buddy. India govt has recognised crypto, but has 100 ways to discourage you to put money in that. Trust me on this. You may see some good returns in short to medium term in some stable coin. But, a big financial reset is going to hit the world. Your son called block-chain backed crypto would turn zero over night. Bitcoin will be called as the biggest ponzi scheme of the last several decades.

What about taxation? How it is categorized for LTCG & STCG?

Hi Yashodhara,

Considering the exposure the fund aims to take, it will be taxed as a hybrid fund. If the holding period of your units is more than 24 months then the capital gains will be treated as long-term and taxed at 12.5%. If the holding period is less than or equal to 24 months then the capital gains will be treated as short-term and taxed at slab rate.

Do we have 1.25 lak rebate yearly in this fund?

For collateral Margin, It’d be considered Cash Equivalent or Non-Cash

Gold STANDARDS WERE WWI ERA THOUGH GOLD HAS GIVEN GREAT returns last few yrs but shall never replace paper money and its utility in jewellery is lmited, an asset other than gold may be a better mix

This is an excellent FOF. I agree with the overall premise. But could you guys share some quantitative metrics such as Sharpe ratio, max drawdown, historical returns etc?

Hi Sumanth,

You can view the metrics here – https://www.zerodhafundhouse.com/multi-asset-passive-fof/

TER – are we not paying double TER with FoF?

How can i invest

Hi, you can invest in NFO on Coin: https://coin.zerodha.com/mf/invest?nfo=show

What about the taxation whether it will be treated as dent or equity fund

Hey Chinthan,

Considering the exposure the fund aims to take, it will be taxed as a hybrid fund. If the holding period of your units is more than 24 months then the capital gains will be treated as long-term and taxed at 12.5%. If the holding period is less than or equal to 24 months then the capital gains will be treated as short-term and taxed at slab rate.

1. Mean ever invested in equity in bad geo political or during other periods ?

2. Many scheme like quant multi asset fund many time take cash on hand and down the equity expouser… Will u like this or not…

3. If yes then its interesting and if not then your scheme is not better than other….

What is the Total Expense Ratio of this fund?

Why Mutual fund purchased via Coin platform does not reflect in CAMS or KFIN portal?

I got a few suggestions that should be mentioned in every fund description summary

1)Mention dividends reinvested in funds(if they are)

2) Mention the expense ratio of every scheme you put out

This Fund of Fund is going to be available as ETF or Mutual Fund? Also, what is the hair cut that is determined for this fund if it is pledged for trading?

And what about the Taxation (income tax) in such Multi Asset Allocation Fund ?

Hi Ketan,

Considering the exposure the fund aims to take, it will be taxed as a hybrid fund. If the holding period of your units is more than 24 months then the capital gains will be treated as long-term and taxed at 12.5%. If the holding period is less than or equal to 24 months then the capital gains will be treated as short-term and taxed at slab rate.

Why discussion did not cover tax implications?

What will be the tax rates since equity is less than 65%?

Have a option daily call / put buy ?

Need a video on this

Ok

Thanks Vishal,

Please share your insights on how has this mix performed. How does the 1y, 3y, 5y, 10y backtest look with regard to Nifty 500 in terms of Rolling Returns and during market Drawdown.

Hi Pinkal,

You can view everything about the fund here – https://www.zerodhafundhouse.com/multi-asset-passive-fof/

Zerodha

Thanks Vishal, how has this mix performed. How does the 1y, 3y, 5y, 10y backtest look with regard to Nifty 500 in terms of Rolling Returns and Drawdown?

25 % only in Gold seems a bit high

What is the max historical drawdown?

What’s the frequency of stocks shuffling?

Backtest result is good with compared to other index in both bull n bear markets

Can you share the exact max historical drawdown % you saw in your backtest? And for how many years did you backtest?

Hi Akhilesh,

You can check everything about the fund here – https://www.zerodhafundhouse.com/multi-asset-passive-fof/

Can we do Sip or need to invest upfront

Hi Archit, you can invest in NFO now on Coin; this will be a lump sum investment. Once the fund opens for continuous purchase (within 5 business days from 8th August), you can start SIP.

What will be the haircut for pledging?

Hi Akhilesh, the haircut for Multi Asset mutual funds is around 9%.