Introducing Fixed Deposits on Coin

Even today, a large part of household savings in India sits in fixed deposits.

The appeal is simple, predictable returns, no market volatility, and very little to manage once you’ve invested.

But that simplicity doesn’t scale well. Once you have FDs across multiple banks, rates are scattered, processes differ, and tracking maturity dates and interest becomes harder than it should be.

We’re simplifying this by bringing fixed deposits to Coin.

You can now invest in FDs across multiple banks, compare rates side by side, and track everything, such as invested amount, accrued interest, and upcoming maturities, in one place.

We’re starting with four small finance banks:

- Suryoday Small Finance Bank: up to 8.0% p.a.

- Utkarsh Small Finance Bank: up to 8.0% p.a.

- Unity Small Finance Bank: up to 8.0% p.a.

-

Shivalik Small Finance Bank: up to 8.30% p.a.

The RBI regulates all four, and deposits up to ₹5 lakh are insured under DICGC (Deposit Insurance and Credit Guarantee Corporation).

Tenures range from 7 days to 60 months. Premature withdrawal is allowed after 7 days, with applicable penalties shown upfront.

How to invest

On the Coin app, tap on Fixed Deposits and then Invest.

On the web, log in via Kite and go to Fixed Deposits, or visit fd.zerodha.com.

From there:

- Pick a bank and compare interest rates across tenures

- Use the calculator to estimate returns

- Enter your investment amount (minimum ₹1,000)

- Choose payout mode (at maturity, monthly, or quarterly)

- Select maturity preference (refund or reinvest)

For your first investment with a bank, you’ll need to complete a one-time KYC. This includes PAN, Aadhaar verification, basic details, and nominee information.

You’ll also need to verify your mobile number via OTP and add your bank account (via UPI or account details).

After payment, a short video KYC needs to be completed within three days. Once verified, your FD is booked, and confirmation is shared.

For future investments with the same bank, this process is skipped, making it much faster.

You can also watch this video for a walkthrough.

A few things to know

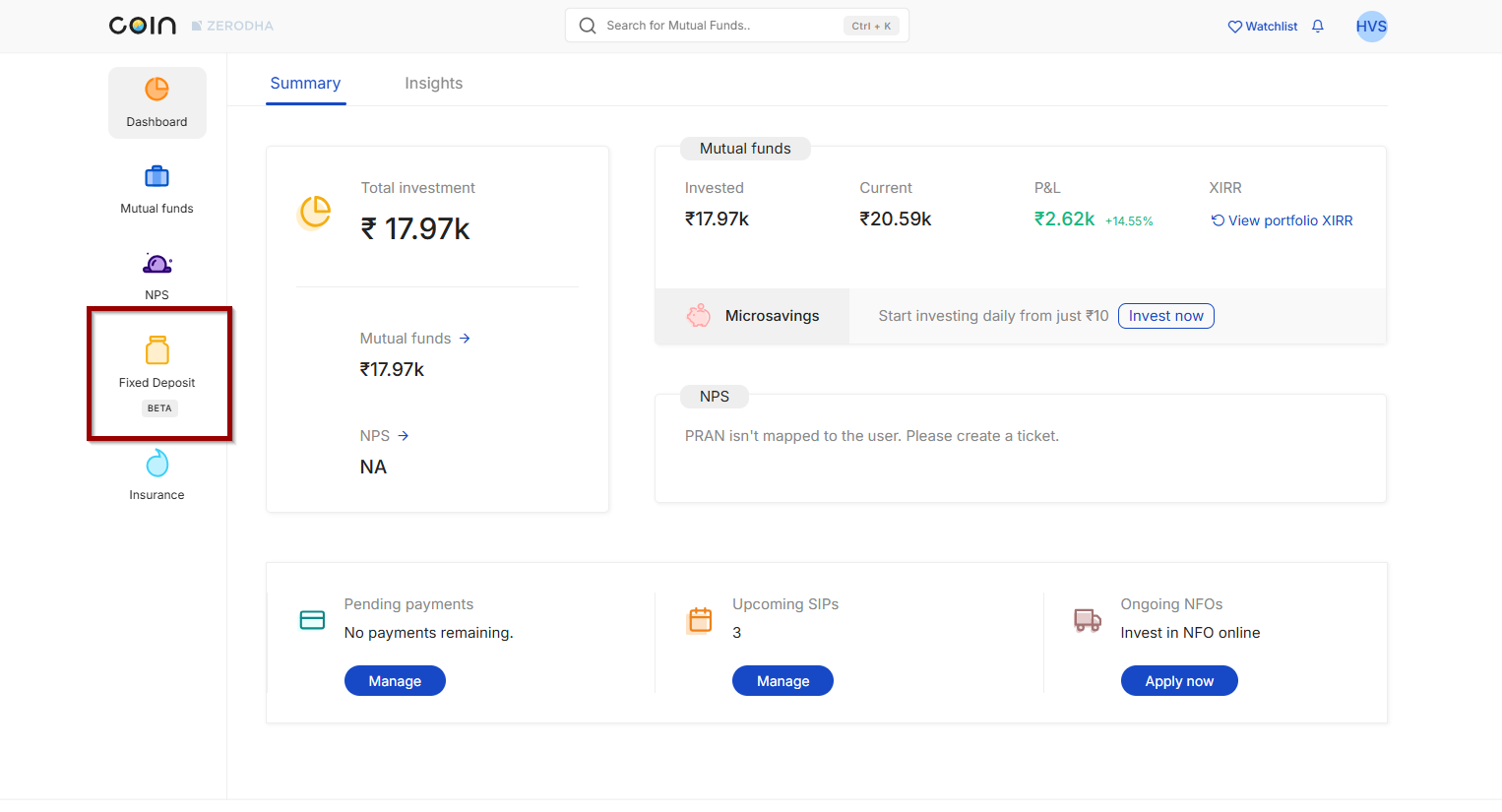

Tracking: All your fixed deposits are visible in one place on Coin. You can see the total amount invested, accrued interest, and upcoming maturities without tracking each FD separately across banks.

Auto-renewal: You can choose to renew your FD automatically at maturity. We’ll notify you in advance so you can review or change this preference before it’s executed.

Premature withdrawal: You can withdraw your FD before maturity if needed. The applicable penalty, based on the bank’s terms, is shown upfront so there are no surprises.

Senior citizen rates: If you’re eligible, higher interest rates are automatically shown and applied based on your PAN details.

Taxes (TDS): Interest earned on FDs is taxable as per your income tax slab. TDS is deducted by banks if interest exceeds ₹40,000 (₹50,000 for senior citizens) in a year. Since TDS is calculated per bank, you’ll need to report total interest across all FDs while filing returns. Tax details and certificates will be available for reporting.

You can learn more about FDs on Coin by visiting FAQs for Fixed Deposits (FDs).

Note: Fixed Deposits cannot be pledged as collateral. Learn more.

Disclaimer: Fixed Deposits (FDs) are not exchange traded products. Zerodha Broking Ltd. acts solely as a distributor for FDs and such products. Any disputes with respect to such services will not have access to SEBI SCORES/ODR, Exchange Investor Grievance Redressal Forum, or Arbitration mechanism.

May i know from when Zerodha would be introducing US Stock investing through Gift city?

Hi, our team is currently working on this. We will keep you posted regarding any updates here: https://tradingqna.com/t/gift-city-based-us-investing/190085

I have a suggestion for you, I request you to improve it in ur next update.

please add folder system for portfolio. I am facing trouble to find out the stock in my portfolio. If you maek such system than I can pur my scripts into various folders like small, mid, large, mf, sectors, etc.

Hi Kavita, we’ve noted your feedback. For now, you can categorize your trades and investments using the Tags feature available on Console to tag and sort holdings according to your preference. https://support.zerodha.com/category/trading-and-markets/kite-features/tags/articles/add-tags-on-console

Hi,

This service is highly unreliable. Just tried to open a new fd of INR 1000 with Suryoday Bank as a trial and upi payment failed with the message saying ”Receiver account can’t accept the payment…” or something like that. Couldn’t even read the error message because the control was redirected back to Coin app. The amount was deducted from my account but was deposited back in a minute. All in all this service is so unreliable that I won’t bother to use it again. I accepted better work from Zerodha given their main competitor StableMoney is doing better in this space. I don’t want to use StableCoin because their service is bad but Zerodha has done even worse job..

I just tried to open a new fd of 1000 INR and now stuck on Payment screen. Besides adding my bank account using my account number and ifsc code it does not allow me to pay via netbanking. It asks me to pay via upi but I don’t want to pay via upi so why are you not providing an option to pay through netbanking?

Hi Amit, Netbanking option is available for payments over Rs. 1 lakhs.

Wow.. Why is it not mentioned anywhere? I tried so many things, tried again and again to get it working to no avail and then finally quit.. not expected from Zerodha. I have already moved to a different platform for booking my FDs. These days you can lose customers easily if you are not good enough…

Can we in list top bank like HDFC, BOB, Axis ?

Hi Rahulkumar, we’re working on adding more banks.

Can we pledge these FD for Margin on the zerodha kite ?

Hi Akhilesh, no, currently FDs cannot be pledged for margin. We’ve taken this as feedback.

Can these fd used as a cash component for margins in fno

Hi Shashikanth, no, currently FDs cannot be pledged for margin. We’ve taken this as feedback.

Can we also add the some info around CRISIL rating guidelines? Like which is better rating A or A1 or A+ or A1+. It will be really helpful if we have it on the https://fd.zerodha.com/ page

Hi Nishit, we’ve explained how to interpret credit ratings here: https://zerodha.com/z-connect/rainmatter/a-quick-guide-to-cash-management-for-startups#:~:text=mutual%20debt%20fund.-,Corporate%20fixed%20deposits,-Corporate%20FDs%20are

Can NRI’s book FD and later repratriate the amount once completed the FD term. Please let me know.

Hi Subash, currently, FDs on Coin are available only for Indian residents. NRIs cannot invest at the moment. This is because the digital KYC process (including Aadhaar-based authentication and video KYC) is designed for resident Indians with Aadhaar-linked mobile numbers.

Can we pledge the FD and get margin?

Hi Vinod, no, currently FDs cannot be pledged for margin. We’ve taken this as feedback.

Can you share a notification when pledge option is made available. Looking forward to invest once pledge option is available, hopefully that will be considered as cash component.

What are the charges I’d be paying to Zerodha for this feature?

Hi Rahul, we don’t charge anything for investing in FDs from Coin.

Who would invest with these cooperative banks but good to know that you have taken the first step.

I would expect the below in future.

– FD from major banks

– FD through zerodha can be pledged

– Instant loan on FD through zerodha

– Option for monthly FD interest credit and then debit towards SIP

Points above will give you edge over other players and also benefit customers.

These are not Co-operative Banks. They are ”Small Finance Banks”

Great initiative.

Can NRIs use these feature if they not in the country? I mean usually the video KYC require you to be in India and close to the location on the aadhaar card.

Hi Belal, currently, FDs on Coin are available only for Indian residents. NRIs cannot invest at the moment. This is because the digital KYC process (including Aadhaar-based authentication and video KYC) is designed for resident Indians with Aadhaar-linked mobile numbers.

First of all, Small Finance Banks are not cooperative banks. SFBs like larger commerical banks are insured for 5 Lacs by DICGC in addition to being regulated by RBI. So there’s is practically no difference on that level. I have been invested with SFBs for over half a decade now. Their interest rates are always higher than scheduled commercial banks. Have make really good interest earnings upto 9% p.a in the past years. Only recently has RBI dropped interest rates considerably so SFBs hage come down to about 7.5% p.a for FD otherwise it was really good.

SFBs like larger commerical banks are insured for 5 Lacs by DICGC in addition to being regulated by RBI –This insured is per customer or per account

Hi, Small Finance Banks are different from Co-Operative banks. As they are regulated by RBI, deposits up to ₹5 lakh are insured under DICGC (Deposit Insurance and Credit Guarantee Corporation).

There is a significant flaw in how bank portals process addresses in the Hyderabad region. Many deposits are being rejected post-KYC because systems do not recognize ’KV Ranga Reddy’ as a serviceable district, despite it being a core part of the city.

Banks should implement a serviceability check prior to the KYC process. Improving this address validation logic would prevent the loss of potential clients and streamline the onboarding experience.

can we pledge this FD to get margin for trading?

Video KYC is done after the payment, and FD is booked if the KYC is verified. This is only convenient to the bank. Why not complete all the KYC related process before payment is made?

Asking the real questions +1

Hi Anil, we’ve noted your feedback and will look into improving this experience.

Are your fds ensured upto 5 lacs

Hi Vishal, yes. All three banks are regulated by RBI and deposits up to ₹5 lakh are insured under DICGC (Deposit Insurance and Credit Guarantee Corporation).

It is a good start, but this facility will become truly beneficial for everyone only once fund pledging and margin facilities become available.

Is this facility available at zerodha app ?

Hi Rama, you can invest in FDs from Coin app.

Is there a provision for submitting form 121 to avoid TDS? If not then this facility is pretty useless. Also just 3 banks? You should have started with a bang with at least 10 banks..

Hi Amit, you can currently file TDS exemption for Suryoday Small Finance Bank FDs online through the platform. For other banks, you can directly submit Form 15G/15H to the bank. We’re working on adding support for more banks.

Please inform once pledging is possible , this would be useful for many F&O traders.

Can NRI invest under NRI fixed deposit which is tax free.

Hi Hitesh, currently, FDs on Coin are available only for Indian residents. NRIs cannot invest at the moment. This is because the digital KYC process (including Aadhaar-based authentication and video KYC) is designed for resident Indians with Aadhaar-linked mobile numbers.

Hello sir g g g g

Can we pledge these FDs to get margin for F&O?

Can we pledge it for margin? Collateral?

NO

READ THE

Note: Fixed Deposits cannot be pledged as collateral

What is the point in launching FD in coin , if it does not allow us to pledge ?There are many platforms which provide this facility 🙁

Which platform??

Can you include shriram finance and bajaj finance too?

Hi Sakthivel, we’re working on adding more banks. Thanks for the feedback.

HOw to close FD before maturity period pls tell

Hi Manish, once you invest in FDs, these will show in the Holdings section on fd.zerodha.com; you can redeem FDs from there.

Normally with Mobile banking if i close the FD the amount will be credited to my account immediately although its on saturday and sunday. how it will work in this case? will the amount gets credited to my bank account or to me zerodha fund?

Can we Pledge these bank FD with Zerodha ?

can we pledge it ? if yes- is it comes under cash equivalent collateral or not

NO

READ THE

Note: Fixed Deposits cannot be pledged as collateral

Can we pledge these FDs to get margin for F&O?

The interest rates should be visible before opening the account. Two, where to submit form 15g/15h. For retired bank employees it would not be beneficial for others it may be.

Hi, you can check interest rates upfront across all available banks before you invest in FD. From 15G/15H can be submitted directly to the respective banks.

NOW IT IS FORM 121

NO MORE 15s

Can NRO or NRE account holders can do?

Hi Paresh, currently, FDs on Coin are available only for Indian residents. NRIs cannot invest at the moment. This is because the digital KYC process (including Aadhaar-based authentication and video KYC) is designed for resident Indians with Aadhaar-linked mobile numbers.

Can we pledge it as a cash equivalent collateral for the Option Selling Margin requirement?

same question

Can we pledge these FDs to get margin for F&O? is yeas what is it will be cash or non cash? what is HC?

Can we pledge these FDs to get margin for F&O ?

Can we pledge these FD for Margin on the zerodha kite ?

Can I get colletral on my FD amount?

Can we pledge the FDs? like we do Liquidbees

Can we pledge these FDs to get margin for F&O?

Hi Sagar, currently it is not possible to pledge FDs for margin. We’ve noted your feedback.

I think no is the answer as of now