How is India placed among the emerging market economies?

- How has India performed compared to other emerging markets, both in the short and the long run?

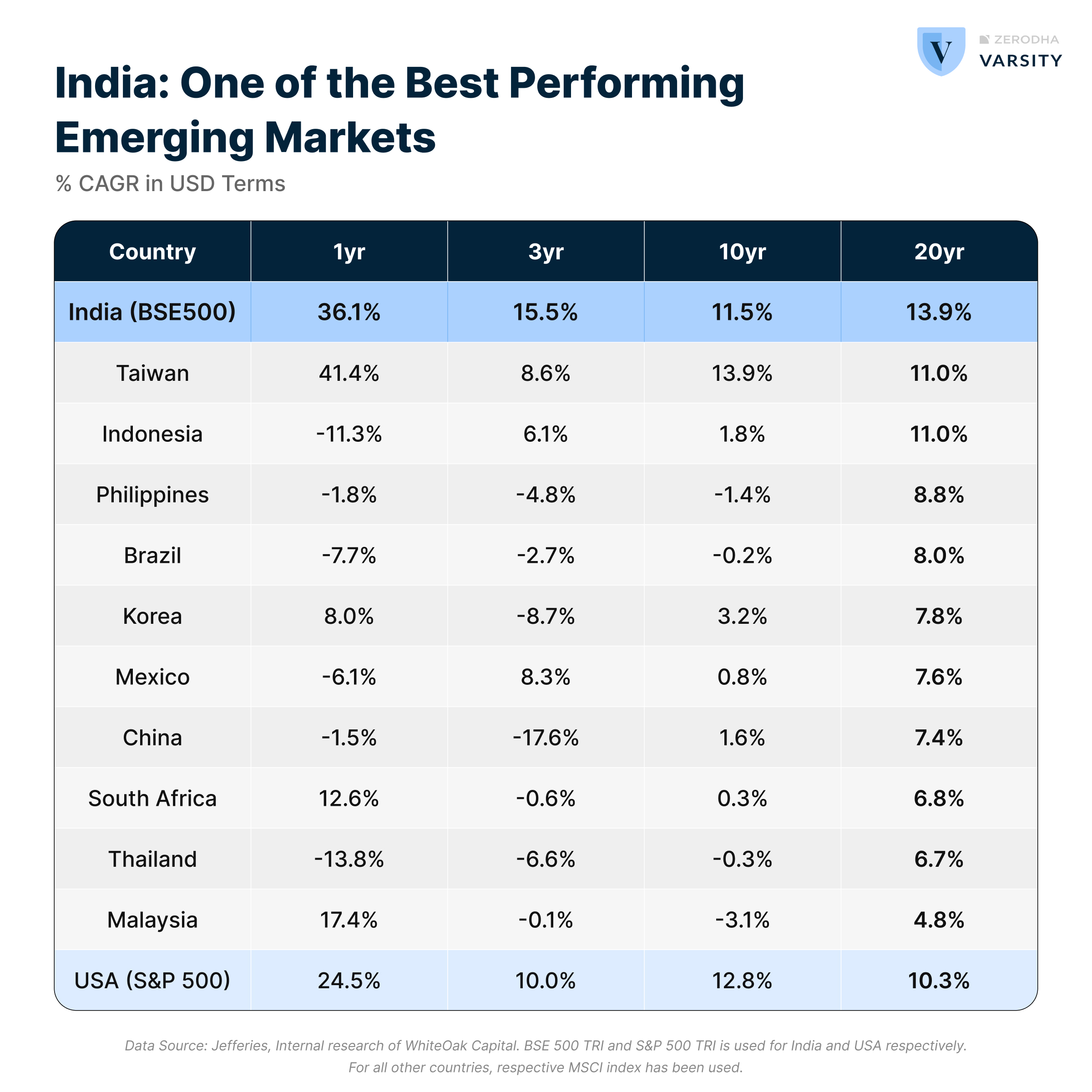

With a 13.9% compound annual growth rate (CAGR) over the last 20 years in USD terms, India is one of the best-performing emerging markets (EMs) over the long term. In the short term (last 3 to 5 years) as well, while most of the major EMs delivered negative to low single-digit returns, India has delivered double-digit returns.

2. The MSCI Emerging Markets (EM) Index is a benchmark index that tracks the performance of equity markets in emerging economies. What is India’s significance in this index? How is it compared to our neighboring nation, China?

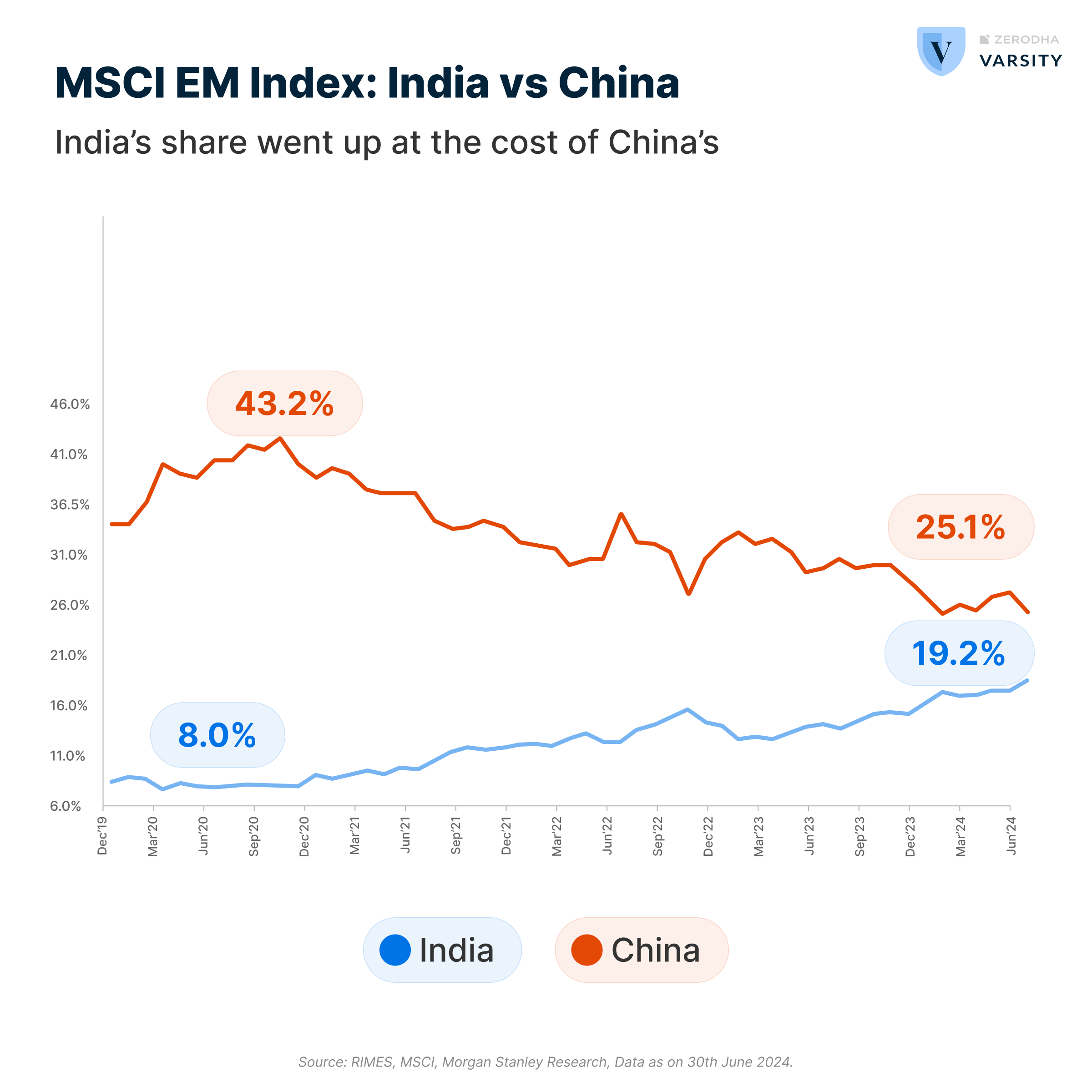

India’s weight in the MSCI EM Index has risen significantly over the last few years. It now commands a 19.2% weight, up from 8.0% in 2020.

Most of this gain has come at the expense of China—its share of EM has slipped from a peak of 43% to 25% at present. This development augurs well, as India stands to benefit from any upturn in FII sentiments on emerging markets.

3. Let’s talk about valuations. Does India trade at a premium or discount to emerging market valuations generally?

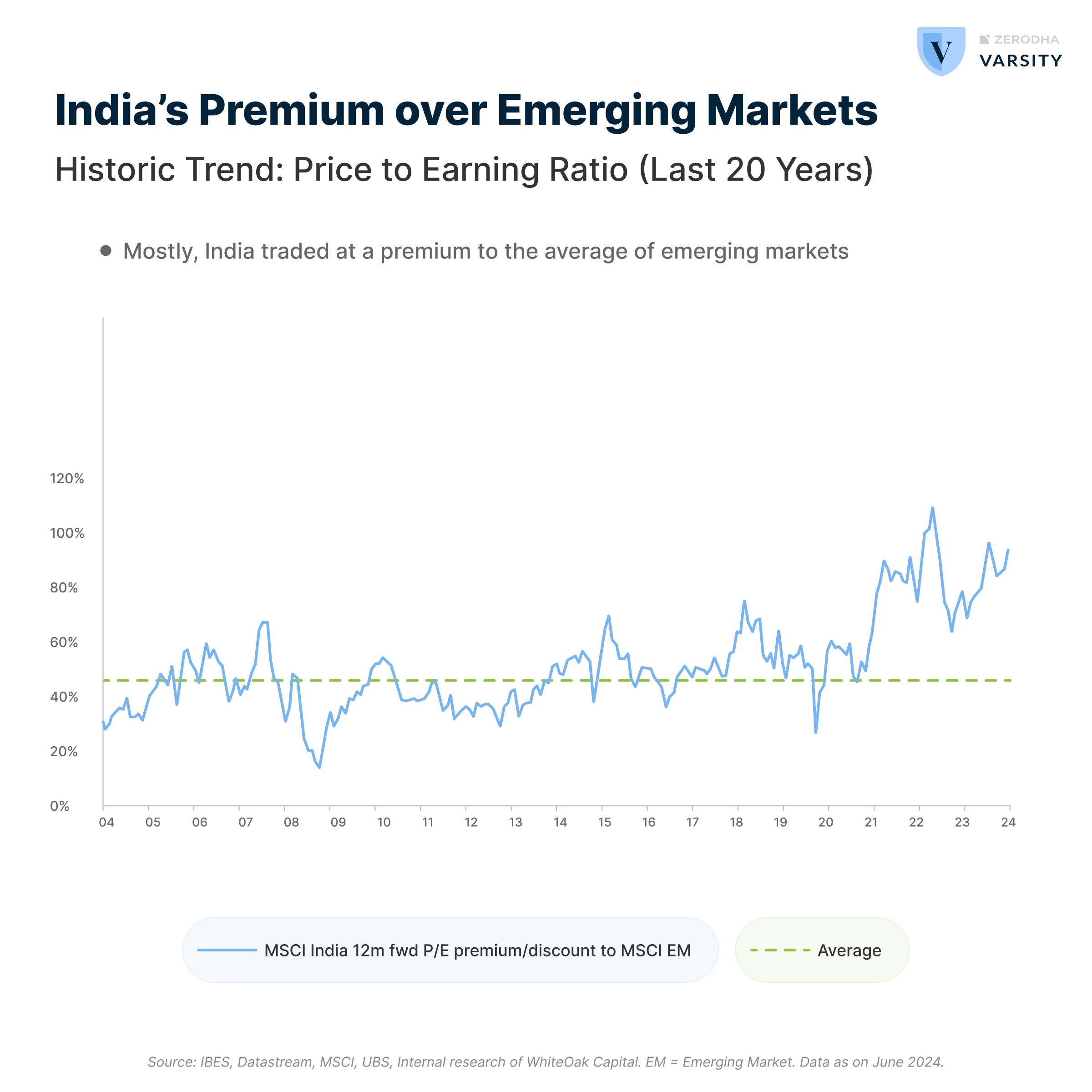

Over the last ten years, on average, India has traded at around a 60% and 97% premium to the emerging markets on a 12-month forward price-to-earnings (P/E) and price-to-book (P/Bv) basis, respectively (according to consensus estimates compiled by Bloomberg and Factset).

4. What do you think is the reason for premium valuations historically?

India has historically traded at premium multiples compared to other emerging markets.

The reason is not different from what is observed for relative multiples of individual company valuations. As we all know, in any sector or country, the company with the fastest-growing sales or profits does not necessarily merit the highest multiple. In fact, other factors, such as corporate governance and the quality of underlying assets, are usually the dominating factors that affect multiples. It should not be surprising then if the same is true for the overall market multiple across countries.

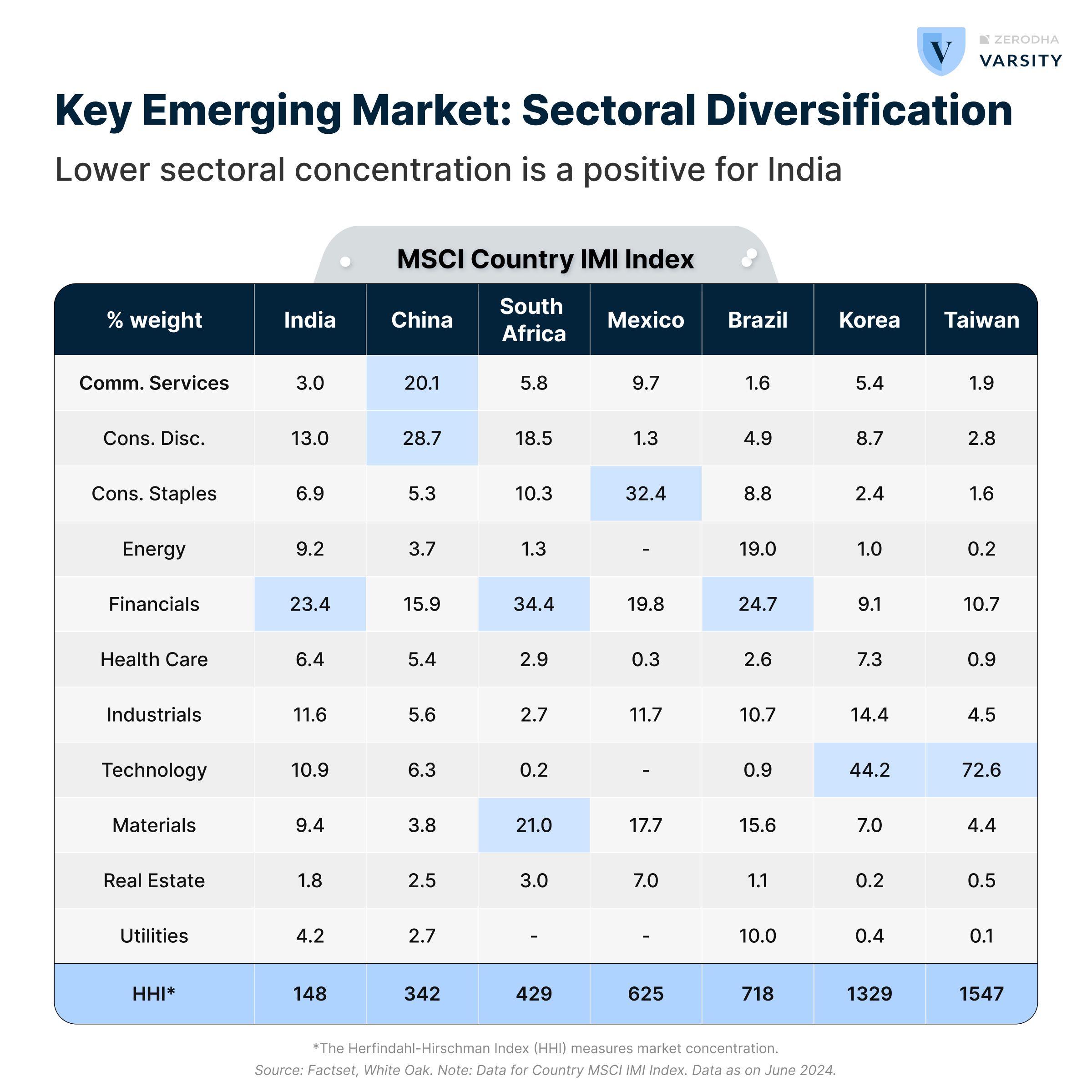

India has a large, profitable, and diverse corporate universe. Unlike several EMs with a disproportionately large weightage to lower multiple sectors like commodities, India has a diverse representation of sectors in the benchmark indices. Going by the experience of past cycles, India’s lower weightage in commodity-like sectors versus EM average makes its earnings less susceptible to global downturns.

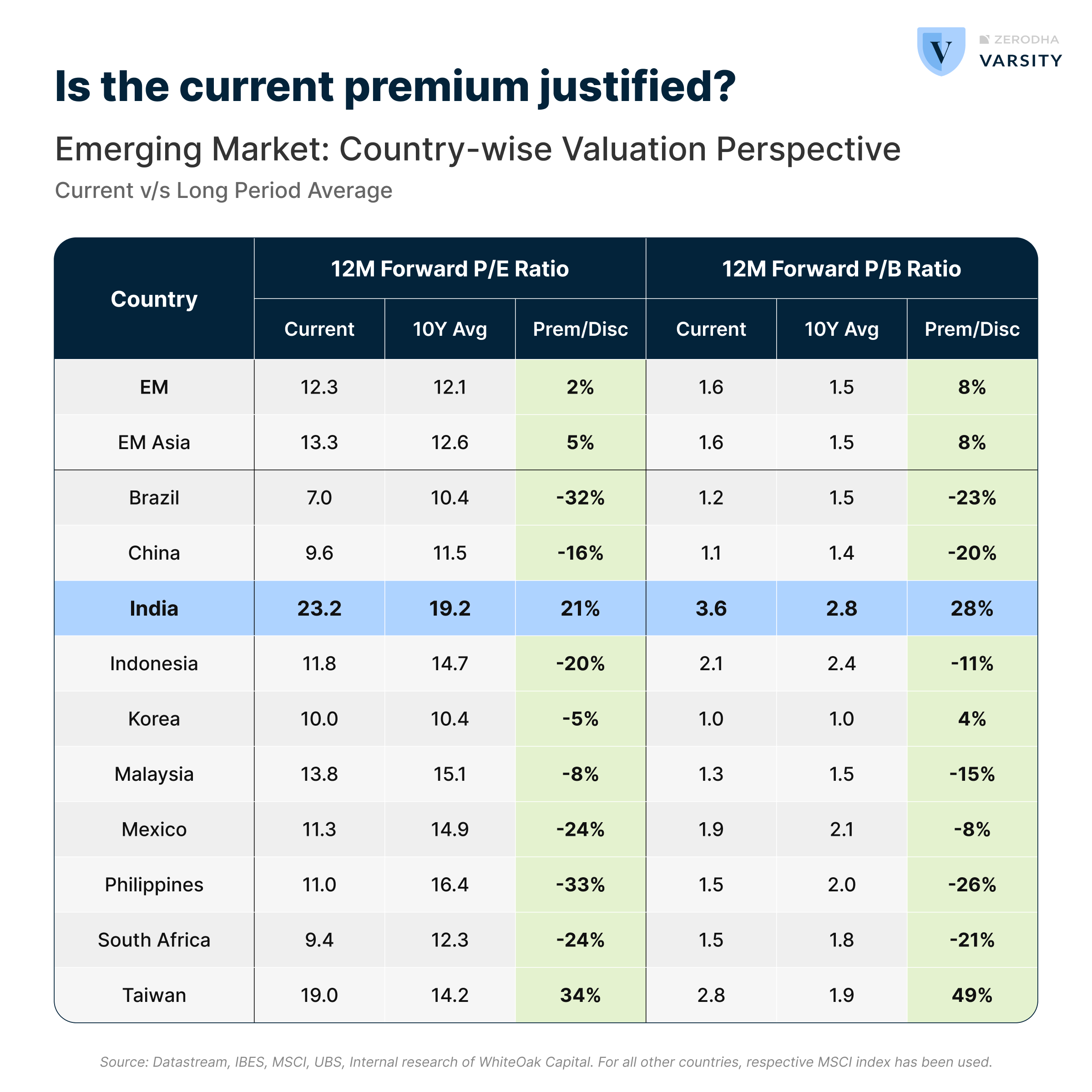

5. Ok, we talked about valuations compared to other emerging economies. Shall we now look at current valuations compared to its past?

As of June 2024, MSCI India is trading at a 92% premium on 12-month forward P/E and a 132% premium on trailing P/Bv compared to MSCI EM. A significant portion of this recent rise can be attributed to the de-rating of China. China, a major component of the MSCI EM Index, has underperformed significantly over the past four years due to various local issues. As a result, the overall valuation multiples for the EM basket have shrunk.

Even compared to its own past record, India is currently trading at almost 21% based on a 12M forward price-to-earnings ratio basis. Whether the current valuations justify the future potential of earnings? Only time will tell.

The views and opinions expressed in this blog are those of the author. All content provided is for informational purposes only and should not be taken as professional advice.