“What doesn’t kill you makes you stronger”

This chapter covers the exit and withdrawal rules from the NPS Tier I account. These rules apply whether you want to exit at maturity or want to withdraw prematurely from the fund. We will also discuss what happens to the fund upon the subscriber’s death.

4.1. Normal Exit (Superannuation) Rules

- Upon Retirement at Age 60:

Upon retirement at age 60 (or superannuation, as applicable), when a subscriber exits NPS, at least 20% of the accumulated pension wealth must be used to purchase an annuity, which provides a regular pension. The remaining amount can be withdrawn as a lump sum.

-

If the total corpus is less than or equal to ₹8 lakh, the subscriber can withdraw 100% of the corpus as a lump sum.

-

If the corpus is between ₹8 lakh and ₹12 lakh, the subscriber can withdraw ₹6 lakh as a lump sum, and the balance may be taken as periodic payouts as permitted under the regulations.

Vesting / Lock-in Rule:

Under the updated framework, a 15-year lock-in (vesting period) applies across schemes, and this period is calculated from the date of opening the NPS account—not from each individual investment. After completing 15 years from account opening (or upon attaining age 60, whichever is earlier), the subscriber may exercise the applicable exit option by complying with the prescribed annuity and withdrawal conditions.If the subscriber reaches retirement age before completing the 15-year period, the normal superannuation exit rules will apply at that time.

-

- Continuation of NPS Account: At 60 years, if you are still working and you feel that you don’t need funds immediately and are comfortable with NPS rules, you can continue contributing to the NPS account until the age of 85. All the benefits you would get otherwise will continue to be available, including the tax benefits.

- Deferment of NPS Account:Deferment of NPS benefits: After becoming eligible to exit (for example, on attaining 60/superannuation as applicable), the subscriber may defer the purchase of annuity and/or defer withdrawal of the lump sum amount up to age 85, by submitting a request to the NPS Trust (or an authorised intermediary/entity). During the deferment period, the subscriber retains the option to exit at any time.

If the subscriber takes no action before turning 60, the account is automatically continued. Also, if you are not comfortable receiving 80% of the deferred amount all at once, you can also withdraw it in a phased manner anytime. At 85, your account will be automatically closed.

4.2 Types of annuity plans

Whether you like it or not, you must use 20% of your retirement savings to buy an annuity plan. To refresh your memory, an annuity guarantees a regular pension for life. There are 15 annuity providers – who are insurance companies—empanelled with PFRDA to offer these products. You can check the list here.

- Annuity for Life: You receive a consistent pension for life. Upon your death, the policy ends with no further payments.

- Life Annuity with 100% to Spouse: You receive the pension, and after your death, it continues to your spouse at the same rate. Once both pass, payments stop.

- Life Annuity with Return of Purchase Price: You receive a pension for life. Upon your death, the initial investment (purchase price) is returned to your nominee, and the policy ends.

- Life Annuity with 100% to Spouse and Return of Purchase Price: The pension continues as long as one annuitant (you or your spouse) is alive. After both passes away, the purchase price is refunded to the nominee.

- NPS Family Income Plan: The pension is paid to you and then to your spouse. After both, it goes to your parents. After their demise, the purchase price is returned to your nominee or child.

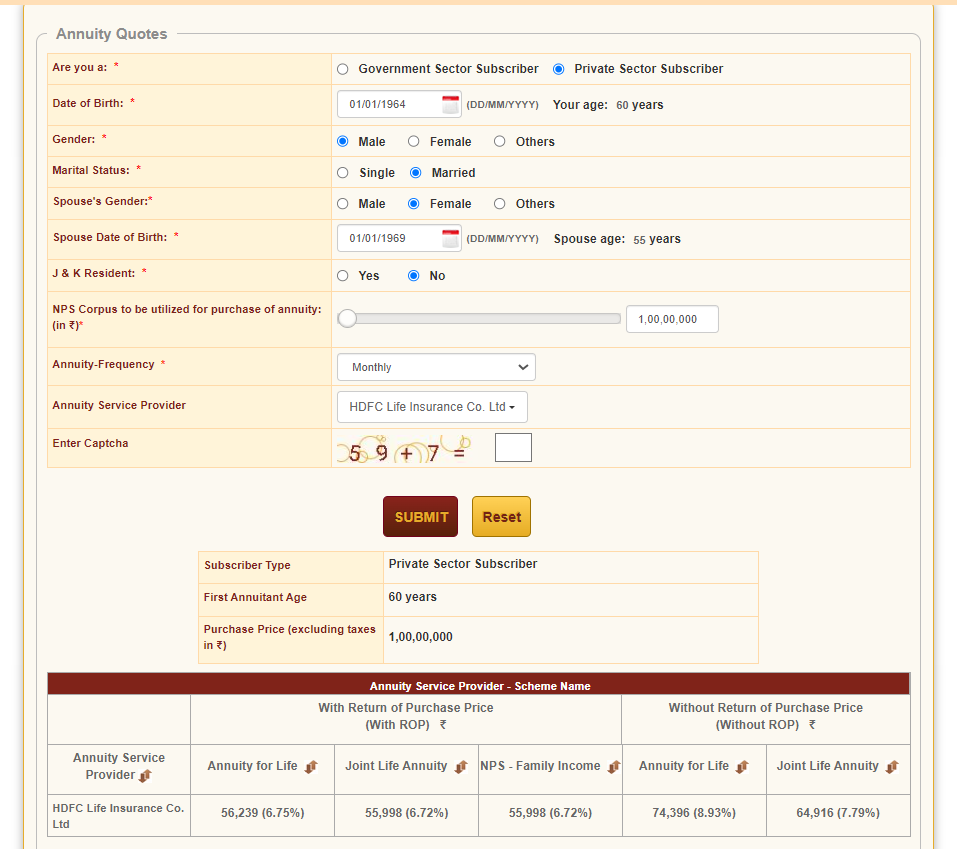

The annuity amount depends on the amount invested and the payment frequency (monthly, quarterly, etc.). Compare rates from providers before making a choice. As of October 2024, annuity rates range from 7.5% to 9%, but these higher rates typically don’t return the purchase price. A slight difference in rate can significantly impact your monthly income, so research carefully. You can check the annuity calculators online here.

For your reference, I give a sample of how this calculator works and the annuity returns offered by HDFC Life Insurance for a 60-year-old under various plans –

4.3 – Partial or pre-mature withdrawal

If you need funds before retirement age, there are two options – partial withdrawal or pre-mature withdrawal. The difference is that partial withdrawals are when a subscriber wants to use the NPS amount for certain conditions like health or buying a house, while the pre-mature withdrawals are when the investor wants to close the account and exit.

In both cases, you wouldn’t get more than 25% of your corpus in your hand. This highlights how hard it is to get your money from the retirement kitty once it is locked. By the way, rules were amended recently to allow loan against NPS. That’s a relief to some extent.

Partial Withdrawal

If you need funds before reaching retirement age, partial withdrawal is an option:

- Eligibility: After completing 3 years in the NPS.

- Withdrawal Limit: You can withdraw up to 25% of your contributions.

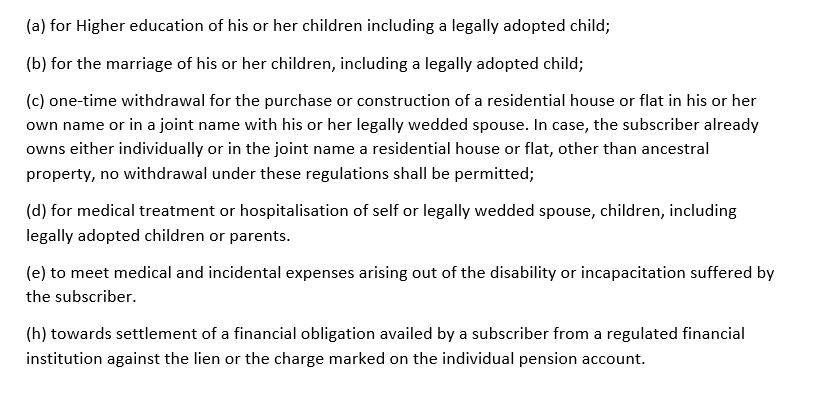

- Specific Reasons: Funds can be withdrawn for specific purposes:

- Frequency: You can make partial withdrawals up to four times during your tenure in NPS with a gap of 4 years between each withdrawal.

Pre-mature exit

If you want to exit NPS before the retirement age of 60 and not for any of the conditions above, you need to choose pre-mature exit.

- Eligibility: After completing five years of mandatory contribution in NPS.

- Withdrawal Limit: If the corpus is more than 5 lakh, at least 80% of the accumulated pension wealth of the Subscriber has to be utilized to purchase an annuity. That is, only 20% can be taken as a lump sum payment from the NPS, while the rest of the amount generates a regular annuity throughout your life.

- Exception: If the corpus is equal to or less than 5 lakh, the entire amount can be withdrawn without any annuity purchase requirement.

4.4 – Unfortunate death

If the Subscriber dies before or after attaining 60 years, the entire accumulated pension wealth of the Subscriber is payable to the nominee or legal heirs. The nominee/family members of the deceased subscriber can also purchase an annuity if they want to, but it’s not mandatory.

you need to mention a nominee at the time of opening of a NPS account. You can appoint up to 3 nominees for your NPS Tier I and NPS Tier II account. And tell the percentage of your savings you wish to allocate to each nominee.

4.5 – Final words

The withdrawal rules are different for those who onboarded NPS between the ages of 60-70. Check the NPS website for the details. Those mentioned above are the exit or withdrawal rules that apply to those who joined NPS before 60.

Even in the case of most emergencies, not more than 25% of the corpus can be accessed. This highlights the importance of having separate investments and an emergency fund outside of NPS for access in case of emergencies.

Just so you know, if a subscriber ceases to be an Indian citizen, they can close the account and withdraw 100% of the accumulated wealth.

Key takeaways

- Options at age 60: NPS subscribers have three choices—withdraw a max of 60% as a lump sum and use the remaining to purchase an annuity, continue contributing to NPS, or stop contributing but defer the withdrawal.

- Account closure at 85: The NPS account will automatically close at age 85 if no action is taken.

- Partial withdrawals: Allowed for specific purposes such as education, marriage, illness, or starting a business, with a limit of up to 25% of the corpus.

- Pre-mature withdrawal: If withdrawing before age 60, 80% of the funds must be used to purchase an annuity.

- In case of death: The total NPS corpus is transferred to the nominee.

1. Is 15 year withdrawal rule available for corporate employees? Unable to confirm this anywhere

2. Should we invest in any specific fund or all contributions are eligible for 15 year withdrawal?

Hi Shivasai,

1. No, under corporate NPS, 15 yaer vesting period rule is not yet applicable. One can exit only after the retirment age set by the company or 60 years, whichever is earlier. But if you come out of the employment and convert corporate nps to individual nps acccount, the vesting period of 15 yaers gets applicable.

2. Under individual nps account, all schemes get the eligibility of 15 years vesting period.

This is whatw e udnerstood as per our reading of the rules. We urge you to check with your HR too, about this once.

Thanks for the reply, so assuming i have contributed X amount under corporate through employer. After 15 years i resign and convert it into individual NPS, i can withdraw X amount is what i understood. Is that the right understanding?

Sure, will check with my HR too

Hi

So, yeah, that\’s the reading so far. We spoke to PensionBox offering Corporate NPS, even their interpretation is the same based on PFRDA\’s communication. But we dont know how it works in practice.

Under the new MSF Scheme, how does this 15-Year Vesting means? Does this mean that if someone is 30-Yr. old and now start investing in NPS, and by the time he/she reaches 45 years this matures and normal withdrawal rules are there? Or he/she still have to continue till the age of 60 and post that only withdrawal can be made? Then what is the significance of this 15-Yr Vesting Period?

Hi Ankit,

Yes, if you invest under the new MSF framework at the age of 30, you will able be bale to withdraw at the age of 45.

Lets say I do premature exit after 5 years and amount is less than 2.5 lakh. Then I will get whole amount.

Is this amount taxed?

After premature exit can I enter again?

Hi Sandee,

Yes, you can withdraw entirely and going by the intent of the law, you will not have any tax benefit.

And, there is no restriction on entering NPS system again.

If a non-government employee exits NPS before age 60 with the accumulated corpus less than 2.5 lakh and have remain invested for more than 5 years, are there any taxation applicable on the withdrawn corpus?

As per our understanding, the tax benefits may not be applicable here since the withdrawal is not at the time of retirement.

Hi sir, Assume that I choose to continue contributing to the NPS even after the age of 60. For some reasons, If I want to exit and withdraw 60% from my NPS account, Is that possible? or since, I chose to continue, would the exit window be extended to 75 years?

Hi Karthik,

Yes, the subscriber can exit from the NPS at any point of time during the deferment period. Please check the rules here – https://npstrust.org.in/sites/default/files/inline-images/22-Exit-FAQs-All-Citizen-Model.pdf

Okay, I have some queries but if they are answered in later chapters, you can just ignore them:

1. For partial withdrawal, there is a limit of 25% but is there any penalty too?

2. \”If you are wondering if one can take a loan from NPS, the answer is no, atleast until 2024\”, what about 2024?

1. No

2. No

Is it possible to provide some information on how convenient the withdrawal process is and if there is any difference in this respect when using POP or direct account? As we know there are so many issues with EPF, it would be good to know if similar issues exist with NPS as well.

Hi Aditya,

Frankly, I don\’t know. Asking around.

Meanwhile, I tried reading about it online. But there\’s no enough information. Since most of the subscribers who joined NPS in the last few years wouldn\’t have been eligible for withdrawal yet, we don\’t have so much information about that. Having said that, I assume the procedure wouldn\’t be too tough as the processes will be made easier for users few years down the line. EPF processes are also undergoing changes as we speak.

Taking about the rules of NPS withdrawal, if you want to withdraw pre-maturely, you will not be able to do so unless you meet the specific conditions.

Update to the comment – I reached out to two people familiar with the procedures of NPS. Both confirmed that the withdrawal process is more straight-forward for NPS compared to EPS.

What if a central government employee who is enrolled in NPS takes voluntary retirement before reaching age of sixty.

Further I would like to add that, after VRS, I don\’t want to contribute further. And I don\’t want opt for only 20% lumsump withdrawal.

Do I need to wait till I attain the age of 60 for 60-40 rule.?

Hi Nitish,

Looks like you have to wait till the age of 60 to take 60% withdrawal. The rules say the following – \”If the corpus higher than ₹ 2.5 Lakh, at least 80% of the accumulated pension wealth has to be utilized for purchase of an Annuity providing for monthly pension to the Subscriber and the balance 20% is paid as lump sum to the Subscriber.\”

You can consider shifting to All Citizens model – \”Subscribers can opt and encouraged to continue in NPS under All Citizens Model post carrying out Inter Sector Shifting (ISS)\”

You may refer to this link – https://npscra.nsdl.co.in/nps-exit/#:~:text=or%20beyond%20/Superannuation%20%29-,Complete%20%28100%25%29%20Lump%20sum%20withdrawal%20is%20allowed%20if%20the,annuity%20if%20they%20desire%20so

Thank you so much for the detailed information!

Some constructive feedback: There is a typo in this sentence:\”Clearly, there are strict regulations with regulations, and rightfully so, in most cases.\”

Noted. Thank you Rushabh.

Add your views, pros and cons of NPS Vatsalya also.

Hi Manikumar,

Yes, we will adding that chapter too, soon.

1. Sir, what about chapter \’dynamic hedging\’?

2. Also, I would love detailed chapter on macro economics that affect markets.

Noted, Prinkesh.

If Tier 2 account of NPS acts like a savings account, would that mean we can invest and withdraw the amount at any point of time ? Also would there be any tax implications like STCG/LTCG on the withdrawn amount ? Is there any lock-in period for Tier 2 investment ?

Hi Sharath,

Once can open tier II account after opening a tier I account. Yes, one can invest and withdraw form NPS anytime. There are no lock-in restrictions for Tier II account. However, there are no tax benefits on Tier II account.

Have watched all the interviews of fund managers on Varsity YouTube channel, next can be your CIO Nikhil Kamath, his thoughts on trading and investing are really insightful. Please do.

Thanks for the recommendations, Prikesh. Noted.

Thank you, Prinkesh!

Karthik sir, I would like to know your views on Ray Dalio and his approach towards investing.

I\’ve not read or followed his work much, cant really comment 🙂

1. Sir, How do we manage inner peace and composure with the volatility of equity markets?

Million dollar question and I wish there was a standard answer to that 🙂

But this has more to do with your personality and less to do with volatility. Btw, stock markets are by default volatile in nature 🙂

Please add a seperate module on Quantitative Analysis.

Check this – https://zerodha.com/varsity/module/trading-systems/

sir following are the requested modules

1. economic analysis

2. ipo analysis

3. cryptos

Sharing this with our team Sid.

However, we doubt covering Crypto 🙂