Clarification on additional brokerage for F&O trades

Additional ₹20 charge is only for traders using collateral margin without the required cash and only if the shortfall exceeds ₹5 lakhs.

No, the brokerage for F&O at Zerodha has not gone up to ₹40. It remains at ₹20 per order. The only change is an additional ₹20 per order for customers who trade on collateral margin (by pledging stocks) without maintaining at least 50% of the required margin in cash or cash equivalents, and only if the cash shortfall exceeds ₹5 lakhs. Fewer than 10,000 of our tens of lakhs of active F&O traders are affected, and even they can avoid it by keeping enough cash in their account.

For the full context behind this change, read on.

What is collateral margin?

When you take an F&O position, you need to maintain SPAN & exposure margins or pay the option premium. Most traders fund this with cash. But you can also pledge securities to get collateral margin against them. If you hold a stock worth ₹100 and pledge it, you get ₹100 minus the Value at Risk (VaR) haircut as collateral. At a 10% VaR, that’s ₹90 in usable margin.

You can pledge two types of securities: cash equivalents (government securities, liquid/debt mutual funds, and ETFs) and non-cash securities (stocks and equity mutual funds). Margins from cash equivalents are treated as cash by the Clearing Corporation (CC). Margins from non-cash securities are not. That distinction is what this entire post is about. You can check the list of securities that can be pledged here.

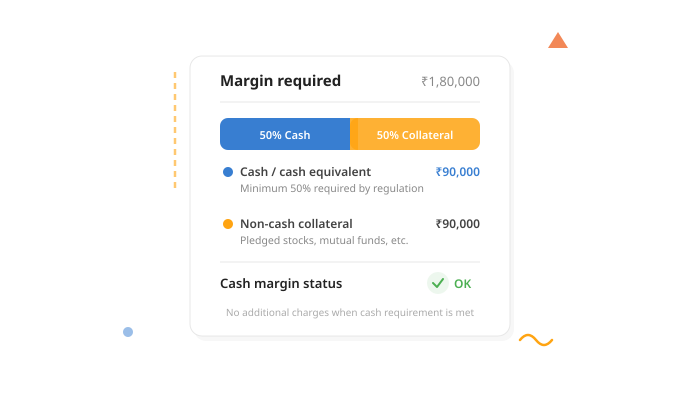

The 50-50 rule

Regulations require at least 50% of the margin for any F&O position to be in cash or cash equivalents. The rest can come from non-cash collateral.

Say you want to buy 1 lot of Nifty Futures, which needs roughly ₹1,80,000 in total margin (SPAN + exposure). You need at least ₹90,000 in cash or cash equivalents; the remaining ₹90,000 can come from pledged stocks.

Now, if you only have pledged stocks and no cash, you are not meeting the 50-50 requirement. We still let you take the trade, but the CC requires the broker to cover the cash shortfall from its own funds. So we would be blocking ₹90,000 of our capital with the CC on your behalf, for as long as the position is open.

In 2022, when SEBI introduced the regulation on segregation of client collateral, we had written about how this would increase working capital requirements for brokers. The 50-50 rule is a big part of that. Every time a client uses non-cash collateral without the required cash component, the broker funds the gap from its own capital.

What we have been doing until now?

Until now, we have not charged anything for intraday cash shortfalls against the 50-50 requirement, even though our capital stays blocked with the CC during that time. We are the only major broker that hasn’t. Industry-wide, brokers charge interest between 7% and 18% per annum on such shortfalls. We do charge a nominal 0.035% per day (roughly 12.7% per annum) on overnight shortfalls, but intraday has been free.

In 2023, we introduced an additional brokerage for margin overutilisation, but only for accounts that went into a negative balance, typically from hedge breaks where the shortfall left no cash or collateral cover at all. We did not extend it to regular non-cash collateral shortfalls.

As collateral usage has grown, so has intraday utilisation of our funds to cover the 50-50 gap. We want to nudge traders towards maintaining the ratio themselves. It is the regulatory intent, and it reduces our capital exposure.

The new charge from April 1, 2026

From April 1, 2026, orders placed when the 50-50 ratio is not being maintained will attract an additional ₹20 per order, but only if the cash shortfall exceeds ₹5 lakhs. Below that, nothing changes. The vast majority of our clients are unaffected.

To put this in perspective: most brokers would charge interest on the shortfall. At 12% per annum, the interest cost on a ₹20 lakh shortfall is about ₹650 per day. ₹20 per order is a fraction of that. We could have gone the percentage-fee route, too, but chose not to because the cost to the customer would have been much higher.

You can check your 50-50 status at any time on the Kite Funds page. If the “Available Cash” field is negative, you are not maintaining the ratio, and this charge would apply once the shortfall crosses ₹5 lakhs.

For traders who prefer to keep cash deployed elsewhere and use stock collateral for F&O, this is a small cost. For those willing to maintain even a portion of the required cash, it is easy to avoid entirely.

In case I have a collateral margin of 2 lakhs and no cash balance. Can I take a FnO trade of 1.5 lakhs using the collateral

Hi Anuj, yes, you can take trade using the collateral margin.

I am paying you around 20 lakhs a year in brokerage, You have applied this rule to options sellers who are trying to make money in a right way.

On the other hands there are brokers who don’t even charge a interest for using collateral even more then 50%.

Congrats to you. Such a poor practice Zerodha to earn money. Best of Luck.

I have 7 accounts You will soon loose all customers.

which broker is offering no interest and Rs. 20 or lesser per order? Please let me know I am also looking to move out ASAP.

my Ticket no is 20260422841318.

I am maintaining more than sufficiant Cash marging than my Non Cash Margin in my accout despite that i have been charged 40 Rs /Order on 21st & 23rd April.

The representative called me dosent have basic understanding of what is OIpneing Balance….he is making confusion in cash equivalent & non cash margin.

I dont have any short margin issue & never breached cash shortfall which exceeds ₹5 lakhs……

so check & correct your system & reverse the Extra brokerage you have charged.

Otherwise i need to changed the Broker

Does this apply only to f&o or cash and commodity market trades as well?

Hi Mayur, this applies to the F&O segment in both equity and commodities. Not for the equity cash segment.

If I have pledged total equity mutual fund for a capital of 100000, and i have a cash balance of 10000 if i take intraday options buying, does this 50 50 rule affects me, will I be paying rs40 per order.

Such a poor practice Zerodha to earn money.Best of Luck.

Yesterday after a long time , I buy a single lot of Nifty for that i add fund into my zerodha account a place a order. Everything goes good but today when I check my zerodha p&l i found zerodha charge me 80 rupees of brokerage for 40 rupees each buy and sell order. What’s wrong zerodha, should I transfer all my stock portfolio to another brokerage app. What type of thing you are implementing? On placing order you shows 20 rupees as brokerage and now you charged it double.

Hi lalit, we’re sorry to hear this. Please create a ticket at support.zerodha.com so we can check this.

Just a clarifying questions. Are we saying Per Order or Per lot??

Say I have placed call sell of 195 quantity(3 lots) of Nifty in a single order. What will be brokrage for the same if I do not maintain 50 percent cash or cash equivalent amount?

Brokerage is per executed order, not per lot.

Hi, brokerage is charged per order, not per lot. In this scenario, brokerage will be Rs. 40 only.

Could you be kind enough to clarify:-

Whether GST will also be charged on this additional amount?

What I mean to say is that Is Zerodha collecting this additional amount as penalty or as additional brokerage?

Hi Paritosh, this additional charge in brokerage, GST will be applicable on it.

thanks for the clarification

I have maintained sufficient cash fund even though they are charging more than before in F&O

|If the “Available Cash” field is negative

@nithin @siva This goes down to negative for fuly hedged and well funded derivative positions very often. This is not the correct metric – you do not show the split intraday that what amount of Available Cash will later get adjusted to the Margins already pledge next day. For eg. I have 0 Available Cash and 10 L in Cash Pledged Securities and 10 L in Non Cash Pledged Securities. I took a fully hedged position utilizing 2 Lakh in Margin today. Say the expiry is in 30 days. Tomorrow onwards you show the Available Margin and Used margin as 18L and 2L respectively. Lets say the next day if market falls or my derivative position is going agisnt me you start showing the Available Cash as negative during the entire day say max I see is 50K as negative Available Cash (you do not show anywhere that this will adjust by tomorrow) – then next day again I see 0 Available Cash and Available Margin and Used Margins have changed somewhat. In this entire scenario I had more than enough Cash equivalent margin. This happens on a daily basis. Looking at Available Cash during a trading day is not a good metric to figure out actual shortfall (as Cash equivalent margin is always available and you don’t adjust against that first) – I manitain it separately at my end. Please change this in the blog – this is blatantly incorrect.

I am paying you around 2.5 lakhs a year in brokerage, You have applied this rule to options sellers who are trying to make money in a right way.

On the other hands there are brokers who don’t even charge a interest for using collateral even more then 50%.

Congrats to you.

You have lost one more customer.

That’s Right.This rule is for options seller.Zerodha want’s to earn more money from them.Lost one more customer.Best of Luck.Zerodha.

which broker is offering no interest and Rs. 20 or lesser per order? Please let me know I am also looking to move out ASAP.

Do you need to front cash from your end for intraday trades as well? Say if one of your “10000” customer does an intraday option sell (ie. Sells first and buys within the same day) without maintaining 50:50, do you send 50 cash to CC intraday, that you are now charging 40 bucks to cover for it ?

Needless to say, now you’ll lose my brokerage too with this decision as I’ll be moving away from ZERODHA.

Team Zerodha,

Slowly you will lose the customer base. If the affected customer base is Fewer than 10,000, what will you gain out of this decision. I switched to cheaper brokerage plan, and you must have lost business of Rs 250000/ per year from me. Gone are the days where Rs 20 per order was talk of the town. These days better and faster APIs are available at much cheaper per order brokerages. Please reconsider your decision and in fact reduce the brokerage with some fixed subscription plan the way rest of the industry is offering it to their customers.

Thank you For Making this post answer most questions.