What changes for investors after Budget 2024?

The finance minister Nirmala Sitharaman presented the Union Budget 2024 today and announced several changes aimed at simplifying the taxation of capital gains. These changes will have a direct impact on your take-home gains and there’s a lot of confusion going around the same.

So, we will try to provide clarity on how your capital gains from various capital assets were taxed earlier and what changes henceforth.

What were the major announcements?

i) Short term gains on certain financial assets to attract a tax rate of 20%, while other financial and non-financial assets to be taxed at applicable rate

ii) Long term gains on all financial and non-financial assets to attract a tax rate of 12.5%

iii) Limit of exemption of long term capital gains on certain financial assets increased to ₹1.25 lakh per year

iv) Listed financial assets held for more than a year will be classified as long term

v) Unlisted financial assets and all non-financial assets should be held for at least two years to be classified as long term

vi) Unlisted bonds, debentures, debt mutual funds and market-linked debentures will attract tax on capital gains at applicable rates, irrespective of holding period

What do they mean?

The above announcements have two primary implications.

One, the determination of long-term vs short-term changes with revision in the holding period of some assets. And second, the tax rates themselves have changed in the case of most assets.

Further, investors used to get indexation benefit on long-term capital gains from certain assets, which is now removed and replaced with a flat 12.5% tax.

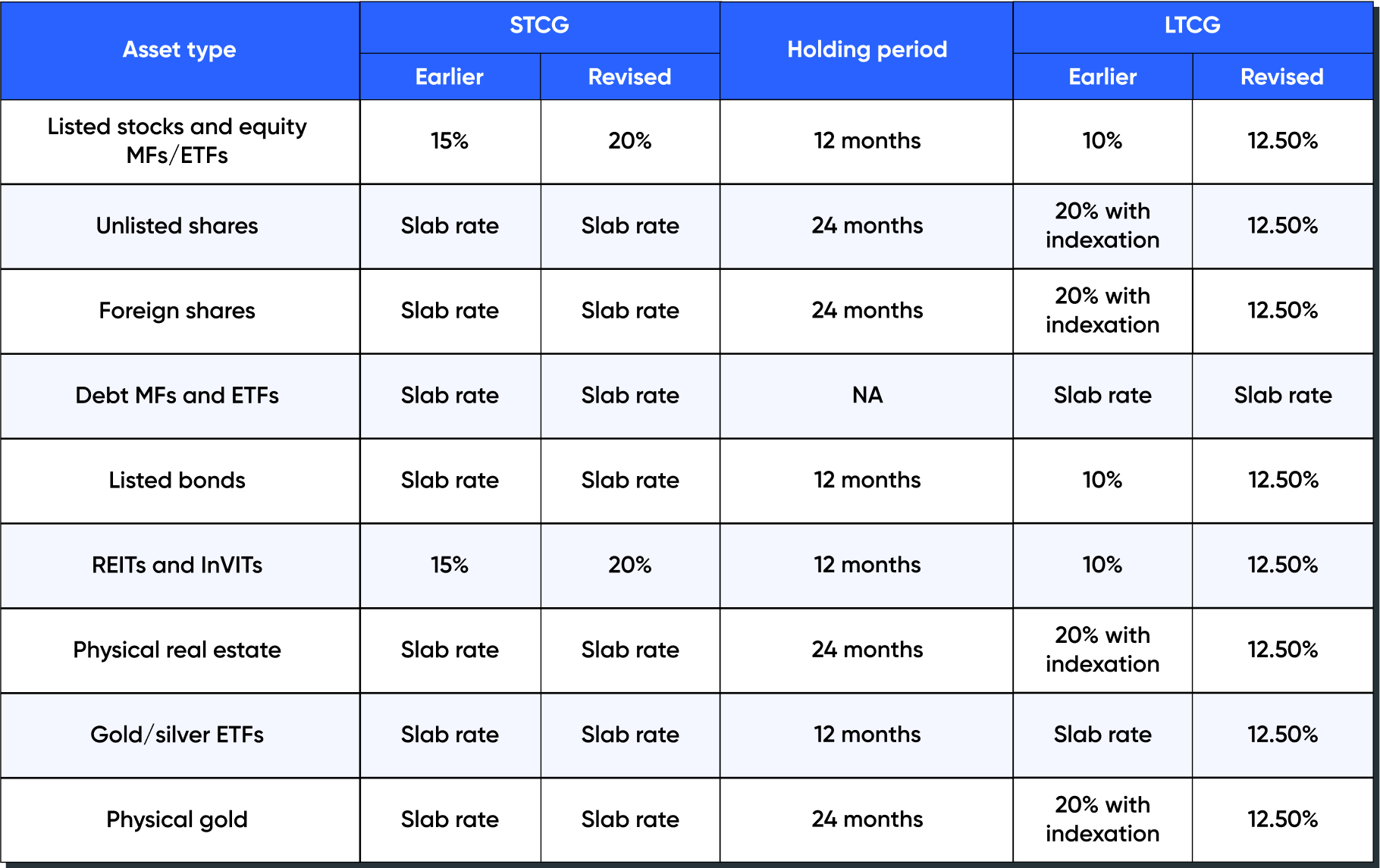

We have summarised the revised capital gains tax rates and applicable holding period for each asset type in the table below.

You can come back to this table for reference as you read further.

Changes in capital gains tax from various assets (effective 23rd July 2024)

1. Listed shares and equity mutual funds: Previously, STCG from these assets were taxed at 15%, while LTCG were taxed at 10%. Following the Budget 2024 amendments, LTCG tax has been increased to 12.5%, and STCG will also be taxed at 20%, marking a 5% increase from the current rates. The holding period remains unchanged at 12 months.

2. Unlisted and foreign shares: LTCG from unlisted and foreign shares were taxed at 20%, with STCG taxed according to slab rates. Now, LTCG will be taxed at 12.5%, while STCG remains unchanged. The holding period to classify gains as long-term or short-term is 24 months.

3. Listed bonds: LTCG on listed bonds was previously taxed at 10% and STCG taxed according to slab rates. While STCG taxation remains unchanged, LTCG will now be taxed at 12.5%.

4. Debt ETFs/mutual funds: Gains from specified mutual funds and ETFs investing over 65% in debt and money-market instruments will be taxed at slab rates irrespective of the holding period.

5. Physical real estate: Gains from the sale of immovable property were taxed at 20% for LTCG and according to slab rates for STCG. STCG tax is still as per the applicable slab rates, while LTCG tax is reduced to 12.5%. The holding period is 24 months.

6. Physical gold: Similar to real estate, LTCG from gold will now be taxed at 12.5%, reduced from the previous 20%. STCG remains taxed according to slab rates. The holding period for LTCG is reduced from 36 months to 24 months.

These changes will be effective from 23rd July 2024 onwards. This means that if you have realised gains before this date, taxes will be applicable as per the old rules.

Increase in Securities Transaction Tax (STT) on F&O

There was also an increase in the STT charged on the sale of futures and options contracts. Starting 1st October 2024, STT on the sale of futures contracts will be increased from 0.0125% to 0.02% and STT on the sale of options contracts will be increased from 0.0625% to 0.1%. The below table gives you a representation of how this affects you as a trader.

| Old STT rate | Applicable STT | New STT rate | Applicable STT | |

| Nifty Futures 1 lot (25 quantity) @ ₹25000 | 0.0125% | ₹78 | 0.02% | ₹125 |

| Nifty Options 1 lot (25 quantity) @ ₹1000 | 0.0625% | ₹16 | 0.1% | ₹25 |

Note: STT values rounded off to the nearest integer.

Other changes that affect you

1. Income from buybacks is now taxable in the hands of recipient investor: The full buyback amount will be taxed similar to dividend income at your slab rate. The amount paid for buying shares will be treated as capital loss to the investor which can be set-off against other capital gains.

2. TDS applicable on government securities: Interest earned from government securities will now be subject to a 10% TDS if the amount exceeds ₹10,000. This will be applicable from 1st October 2024 onwards.

You can also check out this video, where we try to decode the important stuff from the budget for you, in conversation with Vishvajit Sonagra, founder and CEO of Quicko and Dinesh Pai, Head and Chief Strategist at Rainmatter.

Debt MFs and ETFs are of slab rates is hybrid funds are come in same category ?

hi, do I need to pay the 20% stcg, if my total income comes under lower slabs like 5%,10% or 15%

The entire buyback amount would be treated as dividend and taxed at slab rates while the amount paid to buy shares would be treated as capital loss which can be knocked off against capital gains which in effect attracts lesser tax. Why would an investor go for a buy back participation when the tax conservation on capital loss would be less while the amount received would be taxed at respective slab rates?

Your information on Listed bonds in the image vs the text explanation are different.