Think of two siblings growing up in the same household. The older sibling is always expected to follow the rules—curfews, responsibilities, and a clear path laid out by the parents. Meanwhile, the younger one comes with a happy-go-lucky attitude — fewer rules imposed, has the flexibility to choose their own path.

NPS Tier I and Tier II work just like that. Tier I is the older sibling with stringent rules and regulations. Tier II, on the other hand, is the younger sibling—no minimum contribution, no withdrawal restrictions, and no mandatory annuity purchase. But there’s a catch. With anything in life — you can’t have your cake and eat it too — while you enjoy the flexibility, you lose out on the tax benefits that Tier-I accounts offer.

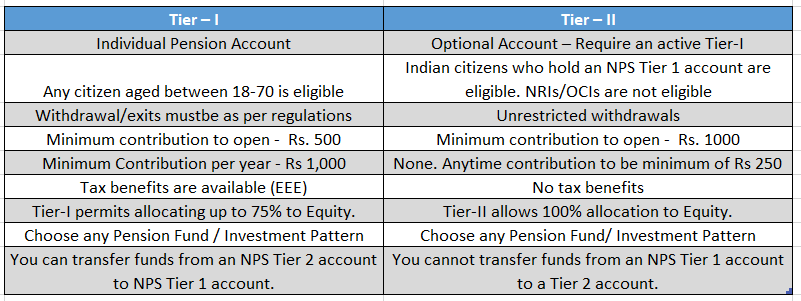

Tier II account works just like the NPS Tier I account and can be opened once you have a Tier-I account. Subscribers in NPS Tier 2 also have three fund options to choose from—Scheme E (primarily equities), Scheme G (government securities) and Scheme C (corporate debentures). You can opt for the ‘active choice’ option, where you set your own investment allocation. Alternatively, there’s the ‘auto choice’ option, where your exposure to equities and corporate debt is automatically reduced as you grow older, providing a more conservative approach as you near retirement.

Further, one can also choose different fund managers to manage different assets.

The flexibility here is that subscriber can select different Pension Fund and Investment Option for his/her NPS Tier I and Tier II accounts. For example, if you have selected 50% allocation to equity in Tier I to be managed by HDFC Pension, you can go for 60% in Tier II and select UPI as fund manager in Tier II.

In fact, in Tier I, a subscriber can have an equity allocation of only up to 75% of the overall investment value (in common schemes, not under the MSF framework) , but in Tier II, you can allocate up to 100%.

As mentioned earlier, the Tier-II account does not have any withdrawal restrictions and one can also transfer the funds from this account to the Tier-I account (only one-way). In case of closure of NPS Tier-I (pension account), the balance outstanding in NPS Tier-II account will also get transferred to the bank account.

Should you invest in the NPS Tier II account?

If the lock-in period of NPS Tier I isn’t appealing to you, but you appreciate its structure and performance as a retirement fund, Tier II could be a good alternative. Psychologically, you can still set aside your investments in Tier II for retirement and maintain financial discipline, even though there are no restrictions.

You might recall how I mentioned that the real strength of NPS as a retirement product comes from its strict withdrawal and contribution rules, which encourage long-term discipline. Since the Tier II account doesn’t come with these restrictions, it’s not technically a retirement savings scheme—it’s more like an open-ended savings account in the form of a mutual fund.

Whether for retirement or other financial goals, NPS Tier II is simply another investment option alongside mutual funds.

Let’s compare it in the usual ways—returns, liquidity, and safety.

In terms of safety, it depends on the underlying assets of the schemes. Scheme E, which invests in top-listed companies, carries the same risks as any equity product with a large-cap focus.

Schemes C and G, which invest in corporate bonds and government securities, respectively, have historically taken on lower risk than similar mutual fund options like gilt or corporate bond funds in terms of credit risk as NPS funds primarily focussed on AAA-rated bonds, for which the probability of default is low. For debt funds, there’s another risk – interest rate risk – as the duration of the papers held by the funds goes up, the risk also increases. It is more nuanced based on the country’s economic conditions. The duration of NPS debt funds is typically higher than that of peers in the MF space – hence NPS funds can be slightly volatile.

When it comes to liquidity, Tier II offers complete flexibility—you can withdraw your money anytime.

As for returns, Scheme E typically mirrors the performance of broad market indices, while Schemes C and G have often outperformed their mutual fund counterparts in similar asset classes.

So, if you’re already considering gilt funds or corporate bond funds for your debt allocation—whether for retirement or another financial goal—Schemes C and G in NPS currently look quite competitive.

For equity exposure, Scheme E of NPS can be one of the options when considering, but there are plenty of strong alternatives available in the mutual fund space as well.

Tax moves the needle!

NPS Tier II comes with no tax benefits, and everybody seems to have made peace with it. As per the NPS website, gains from NPS Tier II are taxed at a slab rate and not treated as capital gains. This is similar to how debt funds are treated as well.

However, there is a significant difference between this and equity funds. Equity gains are treated as capital gains and taxed at a lower 12.5%, which is much more attractive compared to the slab rates of those in the higher brackets.

NPS Tier II taxation is also in a grey area. Some say it can be taxed just like other capital gains – but there is no official clarification.Thus, the analysis also changes based on which tax interpretation you consider.

But you know what? Tax rules keep changing—while taxation moves the needle, it can’t be the only metric used to decide which product to invest in.

We also hear about so-called ‘tax planning’ with NPS Tier II funds. Since one can freely transfer funds from Tier II to Tier I, and since withdrawals from Tier I are tax-free, one could transfer the money to Tier II at the time of redemption. By being in the industry for quite some time, my hunch is that this loophole in the name of ‘ta planning’ will not be entertained for long. So, be cautious when considering that as a potential route to save taxes.

Key takeaways

- Tier II account works just like the NPS Tier I account and can be opened once you have a Tier-I account.

- But Tier II has no minimum contribution or lock-in restrictions

- No tax benefits are available for investing in Tier II

- You can choose different fund managers and allocations for Tier II, independent of your Tier I selections.

- NPS Tier II can be considered an additional investment option, alongside mutual funds, either for retirement or other financial goals.

Thank you very much for the insights explained on nps tier2. Still, I have a query, whether, your entire corpus i.e. pricipal plus gains will be taxable at the time of redemption. I would be grateful, if you could please clarify my query urgently, so that, I can plan accordingly.

Thank and regards

J S Pal, Dehradun

Hi Pal,

As mentioned in the article, there is no specific clause or provision in the Income Tax Act that talks about the tax treatment of gains from NPS Tier II account. So, whether it is to be treated as capital gains or \’income from other sources\’ to be taxed at slab rate is not clear.

Sorry, couldn\’t provide much clarity on this.

Actually calculation of capital gain for Tier-2 account is very tricky. Since it allows ratio change between equity and debt mutual funds without any tax implication, one can do multiple shifts between debt and equity funds and then eventually do partial withdrawal.

In this case, I believe it is not even defined how to compute capital gain. Is this correct understanding?

True, Sakthi.

Capital gains rules of NPS Tier II are not very clear.

Madam please clear taxation on gain , made in Jan 2024,is as per slab rate or ltcg can be claimed .

Hi Anubhav

As mentioned in the story. It\’s a bit of a great area.

But we spoke to Quicko, a tax filing portal, to understand this.

They believe that there\’s no reason to exclude it from capital assets. The profits can be treated as capital gains with a holding period of 2 years to qualify for long term capital gains.

Ltcg would be taxed at 12.5% with no exemption limits. And STCG would be taxed at an individual\’s slab rate.

Can NPS Tier II account be used as an alternative to traditional debt mutual funds as NPS offers better returns at low cost with similar credit risk profile?

Hi Akshay

yes, NPS debt fund performed well in the past. As you know no one knows whether they will continue their performance going ahead as well.

But yeah, similar to mutual funds, tier II account offers flexibility to enter and exit.

If I transferred my funds from TIER II to Tier I, at the time of redemption, my Tier I amount will be tax free, but what about at the time of transfer from Tier II to Tier I, will it be taxable at the time or not?

There is no tax liability at the time of transfer, to our understanding.

Please note that, as mentioned in the module as well, this tax benefit on redemption of money transferred from tier 2 to tier 1 can be closed by the govt anytime.

Hi, how to calculate profits or gains in NPS tier 2 in case of partial withdrawal. I have checked NPS website P&L statement or TAX statement is not available

Hi Yogesh,

According to Kuldeep Parashar from PensionBox, you can get these details from your CRA (Central Recordkeeping Agency). First, check who your CRA is—Protean (formerly NSDL e-Gov), CAMS, or KFintech—and then try to retrieve your details from that platform. Alternatively, if you invested through a POP (Point of Presence, like your bank or Zerodha or any tech platform), you can also get your details from them.

Hope this helps.

I remember there was an official circular PFRDA /2017/11/PD/3 released by the Govt way back in 2017 which mentions that Transfer of funds from EPF to NPS is possible. If i ask about the possibility of transferring the funds from EPF to NPS, neither the EPF body nor the NPS body is giving me the clarity that i need. Neither the NPS PFM gives the necessary clarity in this regard.

I have a couple of queries.

1. Can i move funds from EPF to NPS ?

2. I have a tier 2 account. I will contribute to Tier 2 account without making any withdrawals until i become 57 and then transfer all the funds in Tier 2 account into Tier 1 account. Will taxes be applied even then ?

Hi Aniruddha

As I understand, while the circular was issued, it wasn\’t enabled to transfer funds from PF to NPS yet.

NPS tier 2 account has a tax benefit for Central government employees upto rupees 50k deducted from income above rupees 1.5lac deductions.

NPS TTS account should be activated.

Yes, Amit. government employees are eligible for tax benefits for investing in Tier II account.

However, here, we are talking only for individuals from non-government sector.