3.1 – Types of accounts

Once you have decided to invest in NPS, it is time to understand the details of the product.

Before that, a quick note on the two routes you can choose to invest in NPS –

- You can directly invest through the All Citizens Model.

- Or, if your company is registered under the Corporate NPS Model, you can contribute to NPS as a deduction from your salary.

Under Corporate NPS, employers contribute to NPS on top of the Employee Provident Fund (EPF) contribution. The employer may either keep it a mandatory or a voluntary retirement benefit plan. If NPS is offered on a voluntary basis, you will have a choice whether or not to join NPS.

Moving on, under NPS, there are two types of accounts—Tier I and Tier II. Tier I is your primary retirement account, with restricted withdrawals and minimum contribution rules until you turn 70 or retire. So, all the minimum contribution requirements and withdrawal restrictions we mentioned earlier apply specifically to this Tier I account.

To keep your Tier I account active, you need to invest at least ₹1,000 per year (₹500 minimum per contribution). Tier II, on the other hand, is more of a savings account. You can only open it after getting a Tier I account, and there are no minimum contributions and withdrawal restrictions with Tier II. There’s no limit on how much you can invest in either account. In this chapter, let us focus on the Tier I option.

There are two important decisions you need to make at this stage – asset allocation and the fund manager.

3.2 – How it works

If you’ve ever been to a fancy five-star hotel, you’ve probably seen a variety of restaurants—Asian, Italian, Indian, Mediterranean, French, and more—all under one roof. Each restaurant offers you a starter, main course, and dessert.

Now, imagine you can pick and choose: maybe you have an appetizer in one, a main course in another, and dessert somewhere else, or if you’re feeling lazy (like me), you settle for everything in just one spot.

Think of the NPS (National Pension System) like this hotel. The restaurants are your fund managers, and the dishes are your assets. Each fund manager can offer you a mix of equity, debt, corporate bonds, and alternatives. You get to choose whether one fund manager manages all your assets or different managers handle each type, giving you full control over how you build your retirement portfolio.

3.3 – Investment options

You’ve got four fund options—Scheme E (equities), Scheme G (government securities) and Scheme C (corporate debentures) under the All Citizen Model.

- Scheme E primarily invests in listed shares and has a higher risk than others. However, this is the only component that contributes significantly to returns. NPS fund managers typically focus on large-cap stocks and keep the exposure to mid-cap stocks lower to reduce the risk.

- Scheme G focuses on central government securities and state development loans. While there is virtually no default risk here, the portfolio is still exposed to interest rate movements.

- Scheme C is riskier than Scheme G. It invests in corporate securities and infrastructure-related debt instruments.

- Scheme A is a relatively newer option (introduced in 2016) and invests in unconventional assets through Alternative Investment Funds (AIF Category I and II), Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), Basel III Tier 1 bonds, and securitized papers. These investments carry higher risk compared to other schemes. (Update: Based on PFRDA’s circular dated Dec 13, 2025, Scheme A will go away. Investment avenues under Scheme A will be merged with Scheme E or Scheme C. Also, under Scheme E, gold and silver ETFs are also now allowed.)

Now, you can invest up to 75% in Scheme E, and up to 100% in Schemes C and G. The NPS regulator announced in October 2022 that equity exposure under active choice can continue at 75% unless changed by the investor. This is under what’s called the “active choice” model. (Update: The new MSF framework introduced by PFRDA in September 2025 allows investors to invest in pure equity funds as well.)

If you don’t want to pick and choose, there’s also an auto choice- lifecycle fund option. In this, your investments are automatically balanced based on your age. The older you get, the less risky your investments become, meaning your exposure to equity and corporate debt decreases over time. Here too, depending on your risk appetite, you can choose from three different options available: a) LC75 – Aggressive Life Cycle Fund, b) LC50 – Moderate Life Cycle Fund, and c) LC25 – Conservative Life Cycle Fund.

For those up to 35 years, the maximum equity allocation under the aggressive plan is the highest at 75%, while for the moderate and the conservative funds, the equity allocation is capped at 50% and 25%, respectively.

In October 2024, a new investment option called ‘Balanced Life Cycle Fund’ has been introduced in which the maximum equity allocation of 50% tapers down after the age of 45 years as compared to 35 years under existing life cycle funds.

If you don’t choose any of the options in the auto-choice too, the Moderate Life Cycle Fund (LC50) will continue to be the default choice

If you’re just starting out in your career, don’t be put off by the relatively lower returns from Scheme E in the short term. Equity has the potential to give inflation-beating returns over the long haul.

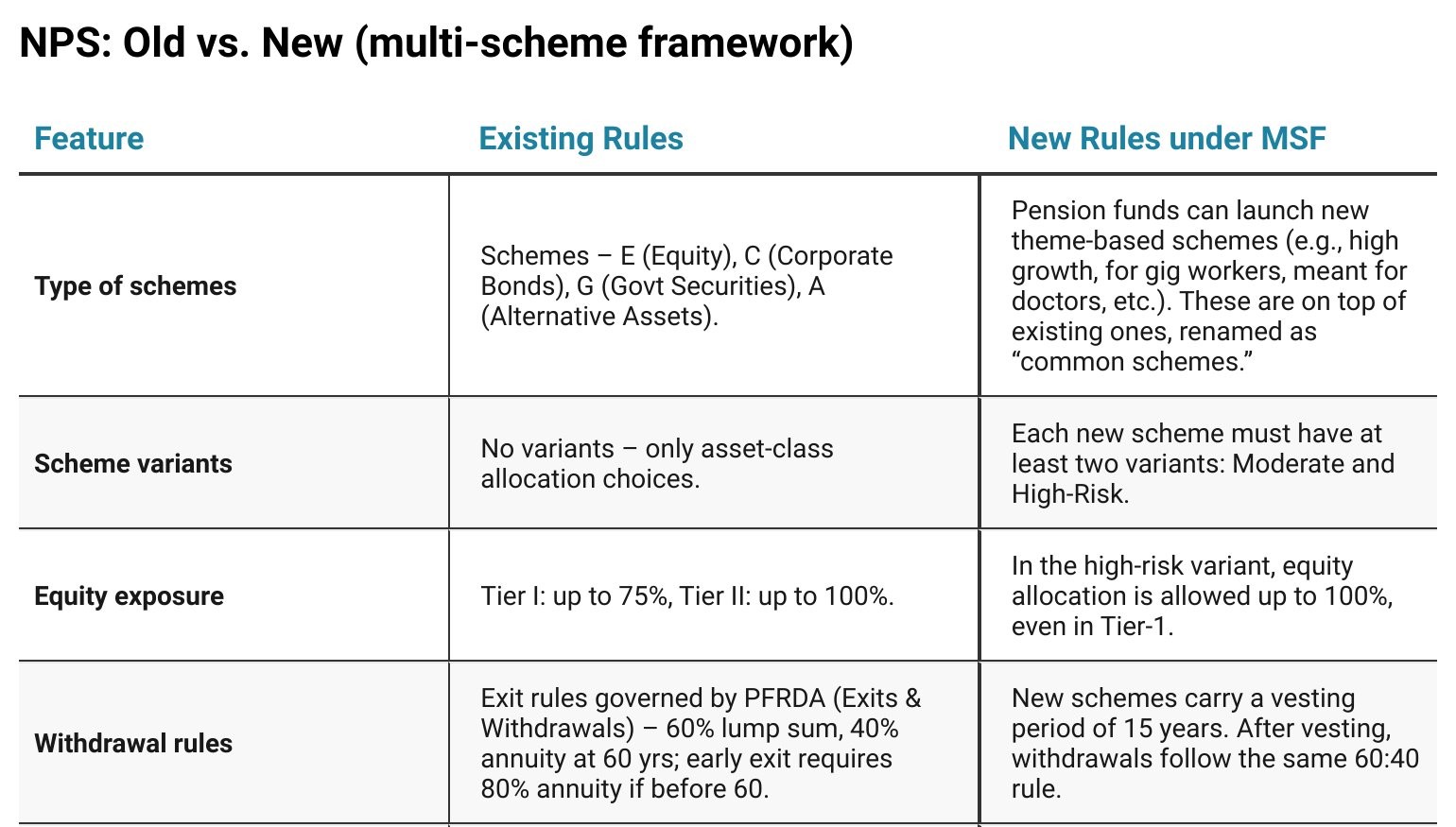

3.4 – New schemes under the MSF framework

The regulator, PFRDA, launched the Multiple Scheme Framework (MSF) in September 2025. Under this framework, pension funds can launch theme-based new schemes—for example, ones focused on high growth or designed for specific groups like freelancers or homemakers. Each scheme will come in two risk variants: moderate and aggressive. The aggressive variant can have equity allocation as high as 100%, which is a big shift from how NPS worked earlier.

The existing Schemes E, C, and G will continue to exist, and going forward, this set will be referred to as “common schemes.”

The key difference is that MSF schemes can come with a predefined asset allocation mix (like 100% equity, or 80% equity and 20% debt) and a clear theme. You will be able to invest in them without necessarily choosing to invest in the common schemes. Also, there is no limit on the number of schemes a subscriber can hold. These funds come at an expense ratio cap of 0.3% while the common schemes are capped at 0.09%.

If you are already an NPS subscriber and want to transfer your funds under ‘common schemes’ to these new schemes, note that it is not possible. It is only for the fresh money to be invested.

On withdrawals, these new schemes are expected to come with a vesting period of 15 years. For example, if you start investing at age 30, you could withdraw at age 45, following the usual NPS rule of 60% withdrawal and 40% annuity. If your retirement age arrives before the vesting period ends, you can withdraw at retirement using the same 60/40 rule. This is notably different from the current setup, where NPS investments are generally locked in until age 60.

3.5 – Selecting fund managers

Ten pension funds are currently available for the All Citizens Model: Axis, Aditya Birla Sun Life, HDFC, ICICI, Kotak, LIC, Max Life, SBI, TATA, and UTI. You can check their performance online to compare their performance across different schemes and time frames.

You are also allowed to select multiple Pension Fund Managers (PFMs) under the Active Choice option.

This means that you can choose up to three different PFMs to manage your investments across different asset classes. For instance, you can have one manager handling your equity investments (Scheme E), another managing corporate debt (Scheme C), and a third for government securities (Scheme G).

You should review your fund manager’s performance regularly and consider factors like long-term consistency. If you’re not happy, you have the option to switch fund managers once a year.

You can check the returns of the schemes here and portfolio details here.

The good part is that switching from one asset class to another or changing your pension fund manager will not have any tax implications on you. This is unlike mutual funds, where switching from one fund to another is treated as a sale, and profits are taxed as capital gains.

Key takeaways:

- There are two important decisions you need to make in NPS — asset allocation and the fund manager.

- You have three fund options: Scheme E (equities), Scheme G (government securities) and Scheme C (corporate debentures).

- You can decide the allocation under an active choice, or the auto choice will decide the allocation based on your age.

- You can change asset allocation four times a year and the fund manager once a year.

- Unlike mutual funds, changing the fund manager will not have any tax implications for you.

Hi Satya, I haven’t started NPS yet, and my employer isn’t registered under the NPS Corporate Model, though they plan to be. Can I start with the All Citizens Model and continue contributing through employer once they join the Corporate model?

Sarvesh,

There is an option to convert individual NPS account to Corporate NPS account. Here\’s a blog from Pensionbox for your reference. Hope this helps.

https://pensionbox.in/blog/How-to-Convert-Individual-NPS-to-Corporate-NPS

I am a regular contributor to NPS only because it is THE best retirement scheme that allows me to build my own retirement corpus with the finest blend of Equity and Debt.

Good to know, Jishnu. Yeah, we should stick to whatever suits us the best 🙂

Hi Pavan,

By continuing your NPS investments instead of withdrawing the corpus at 60, up to 50% of your portfolio can remain in equities. You have the flexibility to keep investing until the age of 70.

Hi Ramachandra,

We got in touch with one of the pension fund managers. As we understand, 75% equity exposure can continue even after 60 under the active choice unless the investor changes it.

Please note tat in Oct 2022, the rule on trimming equity exposure after 50 has been removed for the active choice.

Thank you team for this education, however I am not quite clear on Equity allocation for active choice. As per your table, for age 60 and above, the equity allocation is 50%. Does that mean that once we start retirement at age 60, the annuity option has 50% equity in the portfolio?

Hi Pavan,

In Oct 2022, the regulator announced that the equity exposure under the active choice will not be trimmed once the person reaches 50 years of age. And the cap on equity is 75%.

As we understand, even beyond 60 years, you can still hold 75% equity under the active choice. It continues as is, unless you make any changes.

I slightly simplified the text to remove any confusion, as per your comment.