19.1 – The new beginning

In a fascinating new development, NSE in collaboration with RBI has recently made it possible for retail investors to start investing in Government Securities, mainly the long-dated bonds and the treasury bills (T-bills).

These were products which were available only to banks and the large financial institution, but now we can invest in them and take advantage of attractive and guaranteed returns. However, since these are new financial instruments (at least to the retail participants), understanding the nuances before investing is important. For this reason, we have put the following conversational FAQs with a hope that you will be able to figure out the basics.

Do read on and post your comments below.

19.2 – FAQs on G-Sec

What am I investing in?

You are investing in Bonds/T-bills issued by the Government of India. Since the Government of India backs these, these are virtually risk-free investments. The guarantee from the Government is also called ‘Sovereign Guarantee’.

What are bonds/T-bills?? Tell me more.

Whenever you and I need money, we go to the bank to avail a loan. Against this loan, we promise to pay the bank periodic interest and also return the money after a certain amount of time. This is common practice, where the interest and principal are repaid to the bank.

Likewise, the Government of India also needs money to build roads, bridges, dams, hospitals, etc. When they run short of money, they approach their bank for a loan, which is the RBI. The RBI, in turn, auctions the loan in the form of bonds/T-bills that you can purchase. Essentially, you are lending a part of the overall loan the government is seeking. Against this loan, the Government of India, promises to pay periodic interest and also repay the principal at the end of the tenure.

The loan which the government intends to repay within a year is called the Treasury Bills or T-bills. Loans which the Government intends to repay over many years are called the Bonds.

What should I choose? T-Bills or Bonds?

Both are great investments if you seek the safety of your capital. There are a few easy to understand variables that you need to look at before deciding on an investment in these two G-Sec instruments.

Variables like what? Start with T-bills, please.

There are three T-bills variants, and they vary based on the maturity period. They are 91 days, 182 days, and 364 days. T-bills do not carry an interest component; in fact, this is one of the biggest difference between T-bills and Bonds. T-bills are issued at a discount to their true (PAR) value, and upon expiry, it’s redeemed at its true value.

Woah! That sounds complex. Give me an example, please!

Ok, consider a 91-day T-bill. Assume the true value (also called the Par value), is Rs.100. This T-bill is issued to you at a discount to its par value, Say Rs.97. After 91 days, you will get back Rs.100, and therefore you make a return of Rs.3. Think of it; this is as good as buying a stock at Rs.97 and selling it after 91 days at Rs.100. The only difference is that this is a guaranteed transaction, meaning, there is no risk of you selling below 100 (or above 100).

This sounds quite straightforward, is there anything else I need to know about T-bills?

That’s it pretty much. You need to remember that t-bills are issued at a discount to par, and upon maturity, you get the Par value. Of course, you can get a little technical and measure the yield of this investment if you want.

I’m all ears, let’s get technical!

Yield essentially measures the return on your investment on an annualized basis. After all, all investments should be measured by its returns on an annualized basis. So if you have made 3 bucks over 91 days on investment of Rs.97, then at this rate, how much would you have made every year?

The formula is –

Yield = [Discount Value]/[Bond Price] * [365/number of days to maturity]

= [3/97]*[365/91]

= 0.0309*4.010989

=12.4052%

So in other words, the T-bill offers a return on investment of 12.4052%, but since you held it for 91 days, you will enjoy this return on a pro-rata basis.

Typical 91-day yields are around 6-7.5%. Needless to say, the higher the yield, the better it is.

What happens upon maturity of a T-bill?

Upon the maturity, the Government debits the T-bill from your DEMAT automatically, this is called ‘Extinguishment of Securities’ and the par value gets paid to the bank account linked to your DEMAT account.

Is that all about T-bills? Is there anything else that I need to know?

Nope, that’s it. You are all good to start 🙂

Alright, tell me how the bonds work.

Bonds differ from T-bills on 2 counts. Bonds have long-dated maturities, and they pay interest twice a year.

Sounds, interesting. Can you give me an example?

Every bond issued will have a unique name or symbol. The symbol contains all the information you’d need. For example here is a symbol – 740GS2035A, and here is what this really means –

Annualized interest – 7.40%

Type – Government Securities (GS)

Maturity – 2035

Issue – ‘A’ means it’s a fresh issue (don’t worry much about this, be aware that this is NSE’s internal nomenclature for their own book-keeping )

This issue is expiring in 2035 or 17 years from now (we were in 2018). If you were to invest in this bond, you would receive a 7.4% interest every year until its maturity in 2035. Please note, the interest will be paid semi-annually so that you will get 3.7% interest twice a year. Finally, upon maturity, you will also get back your principal amount.

Here are few more government security (GS) symbols –

| Symbol | Annualized Interest | Semi-annual interest | Maturity Year | # years to Mature |

|---|---|---|---|---|

| 662GS2051 | 6.62% | 3.31% | 2051 | 33 |

| 668GS2031 | 6.68% | 3.34% | 2031 | 13 |

| 737GS2023 | 7.37% | 3.68% | 2023 | 5 |

Can you give me an illustration to help me understand how much I earn if I were to invest in a bond?

Fair enough, but before we get into the details, you need to know one more thing.

Every bond has a Par value, of say Rs.100. When you invest in a bond, you usually invest either at a discount (ex: 98, 97 etc.) or par (100), or a premium to par (101,102 etc.). The price at which you invest in a bond depends on something called an ‘auction process’. More on that later, but for now, you need to be aware that you can invest in a bond at par, at a discount, or a premium.

Now, consider you invest in 700GS2020 (7% with a maturity of 2020 or 2 years from now) at a discount price of 98.4. Assume, you invested in 150 of these bonds, so you’d pay –

150*98.4

= Rs. 14,760/-

From the time you invest, the interest cycle starts. The interest is paid on the face value of the bond. The total amount you earn is as follows –

| Time Period | Interest | Cash flow | Remarks |

|---|---|---|---|

| 0 – 6 Months | 3.5% | 3.5% * 100 * 150 = Rs.525 | Half year interest |

| 6 months – 1 year | 3.5% | 3.5% * 100 * 150 = Rs.525 | Half year interest |

| 1 – 1.5 years | 3.5% | 3.5% * 100 * 150 = Rs.525 | Half year interest |

| 1.5 – 2 years | 3.5% | 3.5% * 100 * 150 = Rs.525 | Half-year interest |

| At Maturity (2 years) | Principal repayment at Par | 150 * 100 = 15,000 | Additional Rs.240 |

So on an investment of Rs.14,760/- you will earn –

525 + 525 + 525 + 525 + 15,000

= 2100 + 15,000

= Rs.17,100/-

If you do the math, the yield on this works out to approximately 7.88%. RBI has beautifully explained the calculation of yield here, do check this if you are keen to know more.

I’ve heard the term ‘ Yield to Maturity’, is this the same?

Hmm, not really. The concept of ‘Yield to Maturity’ or YTM is a little tricky. The YTM calculation assumes that you reinvest the interest payment back into a similar bond, which further generates interest on interest. Bond traders and institutional investors only look at YTM because this is the true comparable value between two different bonds.

This is similar to reinvesting the dividends from a stock back into the stock.

Alright, tell me about the interest payment? How does it get paid?

The interest payment gets credited directly to your bank account linked to your DEMAT account, just like the way you receive the dividends from a company.

Can you give me some insights into the auction process?

Till recently, investment in G-Sec bonds/T-bills was restricted to banks and large financial institutions with a minimum ticket size of 5 Cr. However, recently NSE and RBI have opened it up to retail investors with a minimum of Rs.10,000/- investment.

However, the price you pay for the bonds is still decided by the banks and other major financial institutions. They place bids on RBI’s auction platform, and RBI decides the price of the bonds based on these bids placed on their platform. So the auction process is basically a process to discover the price you’d pay for the bond, also called the weighted average price of the bond.

So it is the weighted average price of the bond, the price I need to pay to purchase the bonds?

Yes and no.

At the time of placing your order, you pay a slightly higher amount. This amount is called the ‘amount payable’. Once all the orders are placed, the auction process starts and RBI evaluates the weighted average price. Any difference between the ‘amount payable’ and ‘weighted average price’, is credited back to your account the very next day.

Wait for a second, what do you mean by ‘option to sell in secondary market’?

This works exactly like how you buy and sell stocks.

Let’s say you decide to invest in 740GS2035A. This means you will continue to enjoy a semi-annual interest payment of 3.7% every 6 months for the next 17 years, till 2035.

Now, after a few years, you no longer wish to hold this bond. In such an event, you can decide to sell this bond in the secondary market, pretty much like how you buy and sell stocks on NSE.

Check this post on TradingQ&A to know more about selling G-Sec in the secondary market.

Great! It looks like I’ve got my basics right. Is there anything else that I need to know?

Think of the whole thing as applying for an IPO followed by the stock getting listed on the exchanges. It’s pretty much the same. The auction process is like the IPO, and once the bidding is done, the Bond (or T-bill) will get listed on the exchange. You can sell the bond whenever you want, or you can even trade the bond once it gets listed!

The minimum ticket size is Rs.10,000/- and its multiples and a maximum of Rs. 2 Cr. You can place the orders when there are new auctions (just like an IPO). However, the good part is that RBI notifies the auction dates and schedule well in advance.

Here is the calendar for the upcoming t-bills auctions.

Here is the calendar for the upcoming bond auctions.

Here is the link of all the bonds that have been issued by RBI. Do pay particular attention to the nomenclature, coupon rate, and year of maturity.

What are SDLs?

To meet the budgetary requirements, State Governments also raise loans from the market, and these loans are called State Development Loans (SDLs). These loans are similar to the dated securities issued by the Central Government, the interest is credited half-yearly, and the principal amount is repaid at the time of maturity. SDLs also qualify for Statutory Liquidity Ratio (SLR), and they are also eligible as collaterals for borrowing through market repo as well as borrowing by eligible entities from the RBI under the Liquidity Adjustment Facility (LAF) and special repo conducted under market repo by CCIL. You may read this FAQ from RBI for more information.

Here is the calendar for the upcoming SDLs auctions.

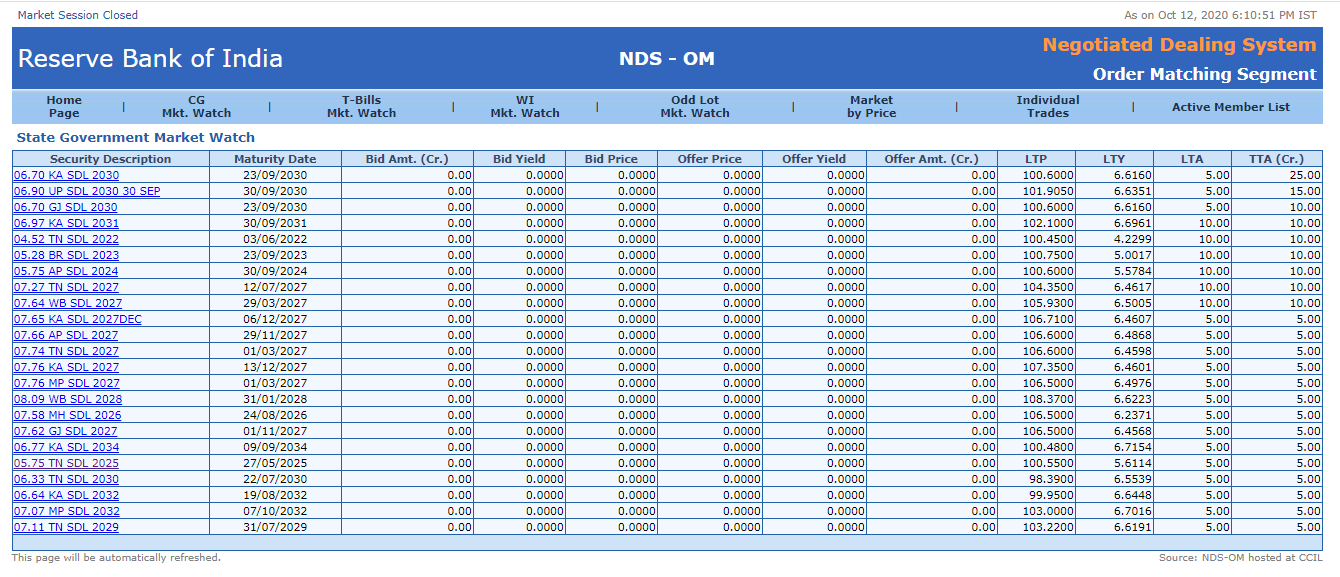

How does the Floatation and Yield of SDLs work?

RBI facilitates the issue of SDL securities in the Market, and the auctions are generally held every fort-night. These are traded electronically on the RBI managed NDS-OM (Negotiated Dealing System-Order Matching). Below is the snapshot of some securities floating for auction as on October 12th, 2020 on the NDS-OM managed by RBI.

Like every other Government Security SDLs also have a unique name or symbol. For example, let’s take 05.75APSDL2024 Security from the above snapshot. And, here is what it really means:

Annualized Interest – 05.75

State Code – AP (Andhra Pradesh in this case)

Type – SDL

Maturity – 2024

This issue is expiring in 2024, i.e. 4 years from now (we are in 2020). If you were to invest in this bond, you would receive 5.7% interest semi-annually until maturity, which is 2024. Please note, similar to other G-Secs the interest for SDLs will also be paid semi-annually so that you will receive 2.8% interest twice a year. Finally, upon maturity, you will also get back your principal amount.

What about the Risk Assessment?

Unlike most G-Secs that have Implicit Sovereign Guarantee ( High Risk or significant funding cost advantages for the institutions that benefit from them), SDLs are associated under Explicit Sovereign Guarantee, which basically means, according to CRAR prudential norm released by RBI the risk accompanied with SDLs is weighted as zero. Banks are not required to keep any capital for investing in SDLs. Hence, making it the risk-free instrument to invest in than most of the other Central Government Securities.

What about taxes?

Bonds – Interest income is credited to your bank account. It is considered as income from other sources and taxes have to be paid as per the income tax slab. If there is any appreciation in the bond price, it is considered capital gains. Long-term (LTCG) is 10% flat or 20% with indexation. STCG is as per the applicable slab rate.

T-bills – You buy at a discount and sell it at par. This appreciation is considered as short-term capital gain, and taxes as is per the applicable slab rate.

In the case of G-Secs, the gain is considered long-term (LTCG) if held for more than 3 years. Otherwise, it is short term capital gain (STCG).

Will I get assured allotment if I place my order?

These securities are issued for limited amounts, and there is no guarantee of allotment if the number of bids received is higher than the issue size. However, if you fail to get an allotment, you can try again next week. RBI carries out multiple issues a month.

This sounds good. How do I start?

Happy investing!

Post your comments below.

I did bit of research about 700GS2020 and similar names on NSE . I can only found bond futures trading on NSE that too with very low volumes. Also can you tell me ticker for T-bills or they will be available post 2018 Aug? Am I missing something?

Also I have read in books that people invested in bonds during 2008 crash and still made money. Which script do they went for in Indian markets?

Nikunj, yes at present only the bonds are listed. The actual bonds are yet to be listed, and NSE says they will be listed by August this year and I guess the trading symbol will be known around the same time.

I have no idea about the 2008 bonds, Nikunj. But I’m not surprised at all. When there is fear in EQ markets, the bond markets tend to perform quite well.

I want to buy old Gsecs (meaning Gsecs which were auctioned long back and have high interest rate) i don’t see any sellers ..how do i know the Gsecs traded in the secondary market ? Maybe i can buy from those ?

Milind, you can try placing an order in the market. These are now tradable anyway.

How to Actually invest in these securities ? Can we do this from our Dmat Account or there is any other way ?

We will be setting up an order collection form where you can place your orders to buy these securities. Should happen this very shortly I guess.

Is this now available for investment?

Next week onwards, hopefully 🙂

Why next week? NSE already advertise buying the government bonds via mail. So, it means Zerodha should have the facility by now.

The broker needs to build a system to accept and process the order, Hiren.

Hi Karthik,

Will Zerodha notify its registered users (via email) when the system is ready? Or do we have to keep checking this space?

Thanks

Please do follow us on Social media, thats the easiest and fastest way to keep track of developments at our end. Of course, we will also email all clients. Btw, I think we are almost ready, a matter of a day or at the most two 🙂

Thanks for the update, Karthik.

Good luck!

Here you go – https://coin.zerodha.com/gsec

Hi Sir, If i place order for T-Bill through Zerodha, by when can i see the securities in my demat if i get allocated?

By T+5 days at the most.

Hi sir,

If i place an order for T-bills through zerodha and its get allocated on my demat account and later if i want to sell that T Bill, Is it possible through zerodha?

Yes, for this you will have to write to us.

Hi,

https://coin.zerodha.com/gsec

This link doesn’t work. I am retail investors. Please tell How can I invest in government securities?

The link works fine Mayur. What is the issue that you are facing?

Is interest earned on this bills and bonds are taxable ?

Yes, they are taxable.

The article says that indexation benefit is available. How is that possible if we are getting paid interest semi annually?

Indexation is on the capital appreciation i.e the difference between the price at which you buy the bond and the price at which you sell the bond. The interest income gets clubbed to your other income and you are taxed accordingly.

Hi Karthik, the price of the bond gets pulled to the par as time passes (if nothing else changes aka credit rating of the govt), hence shouldn’t we price the bonds (buy price) at it’s constant yield-price trajectory while selling and calculate our capital gains against this price so that it is amortized over it’s time period.

Example for discount bond: We buy bonds @ Rs 95. After 2 years we sell @ Rs 98. But as per the constant yield trajectory, the price of the bond should be Rs 97. That means we have made capital gain of 98-97 = Re 1.

This is what I studied for CFA. Not sure how Indian Tax laws interpret it.

Sujeet, this is interesting, but I don’t think the taxation works on constant yield-price trajectory. I will verify and get back. However, when you hold the bond for more than 3 years, you can take the benefit of indexation (for capital gains), which works pretty much like the way you explained in the example.

hmm.

Also, If we invest (from initial bidding)/buy at Rs 95 and hold till maturity, we will get Rs 100. Then this is the maturity amount which we are guaranteed to get. I don’t think this should be considered as Rs 5 capital gains. The constant yield-price trajectory supports this idea.

Similarly, if it is a premium bond that we buy (say @Rs 105), we will still get Rs 100 at maturity. We shouldn’t be able to show this as capital loss.

Please do verify and update us. Thanks a lot 🙂

Sujeet, this is interesting, we will take the opinion from a tax consultant for this. Meanwhile, this is like the indexation way of treating capital gains. Maybe you should check this.

I guess India follows indexation rules then. Same as in debt MFs. Bit different. Sad that it will be considered STCG for T-Bills and bonds below 3 years and taxed. But it does make the calculations much easier.

How is the 10% flat or 20% with indexation chosen for LTCG?

This is like the debt mutual funds, Sujeet.

Hey Kartik!

I wanted to know whether there are any free paper trading platforms available online. Could you please help me out here.

Thanks.

I’ve not really explored paper trading platform, Rohan…so cant really help you with this.

Hi Karthik Rangappa

if we calculate the ytm for 91 days T bill ( at indicative yield of 6.93 % as shown on coin page ) ,

then the result is around 29 % . Is this so good to be true ?

It means that we can have almost 30 % return via investment in bonds alone (of course repeatedly investing upon maturity till 1 year ) ?

YTM is on an annualized basis, Raghu. So 6.93% is for the entire year.

If annualized percentage is 6.93% for 91 days as given on coin website.

Suppose i invested 10,000 then how it is calculated for 91 days and how much money will get into my trading account after 91 days.

You will get 100 minus the allotment price after 91 days.

Hi Karthik,

I did not understand the comment you made “You will get 100 minus the allotment price after 91 days.” Can you please explain a little more?

This line actually refers to the P&L, let us say the allotment price is 98, then the profit that you make will be 100-98 = 2. You will get this amount after 91 days.

How can we invest in government bonds and securities on Zerodha ?

We will soon open an order collection window for this.

Hi Karthik,

Can you explain more about auction process for retail investors? How we can apply for auction? Currently der is not much information about it.

Retail participants cannot really participate in the auction.

You can’t participate in the auction if you are the retail investor. The only institution who can bid with minimum 5cr are allowed in an auction process. Read more at: https://rbi.org.in/scripts/FAQView.aspx?Id=49

Hello Saurabh,

As a retail investor, you are not allowed to participate in the auction process. If you are an institutional investor, then you can bid with min. 5 cr in the auction process. As mentioned in the above chapter, you get the price of the weighted average price of that bond in that auction in that particular week. Read more at https://m.rbi.org.in/Scripts/PublicationsView.aspx?id=16413#1

Hello Saurabh,

As a retail investor, you are not allowed to participate in the auction process. If you are an institutional investor, then you can bid with min. 5 cr in the auction process. As mentioned in the above chapter, you get the price of the weighted average price of that bond in that auction in that particular week.

Check this out (m.rbi.org.in/Scripts/PublicationsView.aspx?id=16413#1).

Detail explanation of both competitive and non-competitive bidding of G-Bonds.

Hope this helps you.

[add https, as zerodha restricts putting complete link here]

Read more at (https://m.rbi.org.in/Scripts/PublicationsView.aspx?id=16413#1).

Detail explanation of both competitive and non-competitive bidding of G-Bonds.

Sir, what brokerage do u charge in buying and selling of G-bonds and T-bills?

We have not yet gone live on this, Apoorv. Cant really comment on the brokerage just yet 🙂

When is zerodha planning to start allowing retail investors to participate in non competitive auction? It was announced by nse in may, and no major player has started it yet.

We are working on this, on priority. We will have this soon.

Oka sari bond konte malli konanousaram leda prathi sanvasaram

Oka saari bond konte, maturity unna varaku, meeku interest vasthuntadi. Prati samvatsaram konalsunna avasaram ledu. Prastutam, ee bonds meeru inka Zerodha lo konadaniki avvadu. Twaralone konocchu.

Kartik,

Any idea how liquid this will likely be? The retail bond market is so illiquid that I have mostly given up on my aim to build a cost effective liquid debt portfolio. Will there be a common platform where retail and institutional lenders compete with scope for block deals? I feel the retail debt in India is artificially protected with schemes like ppf etc., I have seen people who had TDS for their FDs and still getting good tax refunds. Sad situation indeed.

We are working on this product and on priority. Request you to kindly wait for few weeks, thanks 🙂

So just to get a better idea, people say Gsec bond market is volatile, but if i buy and hold till maturity ? In that case i dont have to worry on volatility right ?

For eg: Face Value is Rs 1000 at 7% (annual payment) and i buy that bond at 1090 and hold it for 30 years, my annual payment is Rs 63 for that 30 years period right ?

Also by when will this be available in Zerodha ? Do we have the facility to buy 7.75% GOI bonds in Zerodha as well ?

Yes, thats right, Vikram. For as long as you hold, you will continue to receive the coupon payouts. We are working on putting up a platform, hopefully soon.

Shouldn’t the annual coupon payment remain the same (7% of 1000) Rs 70? Though the ROI will not be 7%, as he invested Rs 1090.

That’s captured in the YTM.

How come 63.

Hey Karthik, sorry to ask this once again, but you guys are definitely going to bring out a platform for retail investors to access T Bills and GSecs, right? And can you give an approximate timeline for when it’s going to go live, like end-November, December, or next year?

The reason I’m asking is that for personal reasons I’ve had to stop equities investments; I’m only interested in fixed income as of now. So the only reason for me to open an account with you guys would be to access T-Bills and GSecs.

We are positively looking into this space, Aritra. Unfortunately, I cannot give a timeline for this

Hi! What happens to the interest in case I sell the bond in between interest periods (six months)? Is it priced into the bond sale value accordingly?

Yes, it gets priced in the bond as accrued interest.

Hey, this post is really informative and I saw the comments about setting up an order collection form where we can place our orders to buy these securities.

My question is: What is the difference between Bonds described in this FAQ (https://support.zerodha.com/category/trading-and-markets/trading-faqs/articles/debentures-bonds-on-kite) VS the Bonds described here? If both are same, do the yield and return calculations done in a similar way? Also, if both are the same securities we’re talking about, how come the buying options are different?

Waiting for your help,

Saurabh

Saurabh, the bonds and t-bills described here are from the primary market plus they are backed by the Govt of India. On the support page, we are talking about bonds available on the secondary market, mainly tax-free and corporate bonds.

Hi Karthik, Thanks for the reply. I got the difference. My question is : If I buy bonds from secondary market, am I eligible for all the conditions of the bond like interest rates, maturity periods etc? I have been reading RBI post about this, but there’s no definite mention about such things (https://m.rbi.org.in/Scripts/FAQView.aspx?Id=79).

Again, many thanks in advance!

Yes, you would be the beneficial owner, hence you are entitled to all the coupon payments.

Hi Kartik sir,

When will we be able to buy rbi t bills and bonds on zerodha platform?

Next week onwards, hopefully 🙂

Hi Karthick,

Can i buy T-Bills and pledge them to zerodha and get trading margin ?

If Not, will zerodha be open to consider it ? (i mean, if you are giving margin on stocks, T-Bills/Bonds are literal cash. :))

– Vinny

This will be possible going forward, not to begin with.

Hello ,

Can you help me regarding how to know if the particular Bill/Bond is available at discount/Par/Premium on the platform.

Thanks.

As retail participants, we are price takers. Remember this is a non-competitive bidding, hence it would be difficult to ascertain if the bond will be priced at PAR or discount.

What is the penalty for early withdrawal?

There are no penalties as such for early withdrawal.

1. So say for 90 day T-bill, I could withdraw the amount in 30 days and still get the applicable % returns for the invested 30 days?

2. Then why do they have 20 years and 40 years bonds, I could subscribe them and withdraw after a year with higher interest right?

1) Yes, the sale price will carry the %return for 30 days on a pro rata basis

2) The long-term bond is bought with an intent of receiving cash flow from coupon rates.

Awesome Karthik. Thank you for your patience as always! 🙂

Cheers, Ashwin. Happy learning!

Are 91 days T-Bills are tax-free? if it’s tax-free, In a year how many times I can invest in that? and what will be ROI on that?

They are taxed like the way fixed income funds are taxed. This also means you can avail the benefit of indexation. You can invest in t-bills as many times as you want. No restriction on that.

When interest paid? is there any fix date?

Most of the GSec bonds pay interest on a semi-annual basis. Check this for the coupon payment dates.

How to know if the particular Bill/Bond is available at discount/Par/Premium on the platform.

As retail participants, we are price takers. Remember this is a non-competitive bidding, hence it would be difficult to ascertain if the bond will be priced at PAR or discount.

Do you provide margin against T bill held zerodha? If yes than how much?

get the answer there same question above

Yes, you can pledge these securities for margins.

Congrats on bringing this finally ! https://coin.zerodha.com/gsec/invest

Can I pledge those from Backoffice once i purchase ? Or I need to wait some time till you enable this feature ?

You can pledge this.

Will this margin be cash equivalent just like liquid bees

I guess you are talking about the margins against the pledge. Yes, you can treat it that way.

Can we know the brokerage charged for this T-bills and Bonds?

Its 0.06% or Rs 6 for every Rs 10,000 invested.

It’s 0.0006 * amount invested.

Hi,

Can you tell will be there be MTM of government securities (bonds) basis closing price if these bonds every day. Bcos if there is a -ve MTM then there will be loss if holder decides to sell. Thanks

No, there is no M2M here. Think of it as holding a stock in your DEMAT.

Hi,

I placed an Order for 184 T Bill but I do not see that now , where can i track the Orders I do not see anything on the coin/gsec page

1.on maturity of 10 years g sec principal repayment happens to bank account or trading account?

2.in case of accidenttal death of g sec holder are these bonds transferred to nominee of demat account ?

If yes can nominee able to sale bond or hold till maturity

1) Bank account. The government debits the bond from your DEMAT, this is called ‘Extinguishment of Securities’.

2) Yes for both.

Hi Karthik,

I need to understand more on the secondary market.

Let’s say I bought a bond which will mature in 10 years from now for 10,000. I hold it for 2 years and get the interest amount semi-annually. After 2 years I want to sell the bond in secondary market, but why would anybody buy it for higher price than 10,000 and get back only 10,000 after maturity ? Instead they would prefer to buy a new bond , right?

I mean in stocks, if the company is doing well ( plus other market factors) the stock price goes up. What are the factors here that contributes for the bond price to go up ?

Harish, the prices of bonds are market driven, just like the way the price of the stock does. The fluctuating price makes the yields attractive/unattractive to investors and therefore. Interest rates play a huge role in determining the price of the bond.

With this said, can clients apply for IPO through Zerodha any soon? Asking as there is a bidding process going in this flow.

With the new block feature in UPI 2, IPOs should soon be possible via Zerodha.

For now, you can check this – https://support.zerodha.com/category/trading-and-markets/corporate-actions/articles/how-to-apply-for-ipos-and-how-to-stay-informed-of-new-ones

This is great news!!!

Happy investing!

I find T-bills to be more attractive investment than bonds, how am I wrong with this statement?

Not really, both differ in terms of the maturity period and cashflows. The yield is roughly the same.

Hello Karthik,

Thanks for educating!!.

Not everyone has a great heart to share the knowledge.

I’m actually searching for material which helps to know everything about trading coffee, but couldn’t find any. I had approached traders who trade coffee, but couldn’t find a convincing answer. Can you help me out with the problem.

Thanks in advance ☺

Thanks for the kind words, Jagat. By the way, coffee futures are not available on MCX, yet.

How do people trade coffee??

I’m curious about this topic because I’m from coffee town and there are traders who trade coffee, on what basis do they get into trade or how do they predict the direction of price?

When can we expect this on MCX as coffee is one of the largest trading commodity by volume next to crude (If I’m not wrong)

Trading happens in the spot market I guess. I’m not aware of this. I’ll check with MCX on this.

Guys – Your transaction costs for G-Sec’s are 0.06% or Rs 6 for every Rs 10,000 invested? In that case for 91 day TBill we are effectively paying 0.24% annualized which is quite high? Suggest considering 0.06% annualized for G-Sec’s which would mean pricing a little differently for short term paper. Thanks, Puneet

Puneet, this is only in the case of 91-day t-bill (i.e if you really consider Rs.6 is very high for Rs.10,000/- invested). For 181 and 364 days t-bills, it works out to 0.12% and 0.06% on an annualized basis.

Thats exactly right and it’s not about the amount but uniformity in pricing. Hence the suggestion that you could price all the T-Bills with an annualized 0.06% cost structure… Therefore the 91 day could be 0.015% and so and so forth… Anyway this was just an observation – If it doesn’t make economic sense for you guys – It’s fine.

Today the only incentive to buy 91 day paper is the 0.4% to 0.5% spread especially given hikes in the future are certain and if one has to give up 50% of the spread in transaction costs – it will be not be attractive. Just an observation for you guys to consider…

After considering the brokerage of 0.06%, the effective yield is lowered from 6.93% to 6.65%, for 91days t-bill.

For an investment of Rs 10000, brokerage charged is Rs. 6.96

Sanchita, I was looking at Oct 2018 91 Day t-bill issue @ 98.26. The yield on an annualized basis works out to 7.10% without the charge. Post-charge, it drops to 7.07%.

Thanks, Puneet. This is a valuable observation. I’ll pass the feedback to the product team.

Thank you sir, whats the procedure to write to you? Do we need to call and inform on this or any platform is provided by zerodha for selling T-Bills?

You can write to [email protected].

Thank you sir

Welcome!

For the various bonds is there a webpage where we can quickly find out dates for interest payment, ex-dates etc.? Gsec prices can vary all the way from say, Rs. 85 to 105 depending upon coupon rate, residual maturity, date of interest payment, etc. Knowing these dates will become very important when one wants to sell them.

Ramesh, the variation in price does not really matter if you intend to hold the Gsec to maturity and enjoy the coupon payouts. Check this page with all the details – https://rbi.org.in/Scripts/NotificationUser.aspx?Id=11391&Mode=0

Can the Zerodha Varsity team come up with a comparison between T-Bills ( 91,182,364 day) vs Debt Mutual Funds with duration less than 1 year ? ( Liquid Funds, Ultra Short Term Funds )

Sounds like a project, will try and take this up. By the way, what exactly do you want us to compare?

Can we classify STCG as business income, just as we do with stocks? Or is classifying it as Capital Gains absolutely necessary?

Its best if you check with your CA for this. But I guess this goes under Capital gains as you don’t really invest in GSec for a living.

govt securities come under income tax rebate.

No tax rebates for Gsecs.

GREAT WORK BY ZERODHA TEAM

Thanks and happy learning 🙂

Can I show this under any section like section 80 C while filing returns ? Ie tax returns.

No, there are no tax breaks for this.

Hi,

Is it possible to buy State gov securities (bonds) as well at Zerodha? If not, by when expected?

Thanks so much.

Not for now, Harsh. We have Gsec and T-bills for now. Hopefully in the near future.

Thanks so much. A few more questions please:

1) Do I need to first move money into my Zerodha A/c to buy G-secs, or the money is pulled from linked bank a/c as I put in my buy order?

2) Are the RBI/Gov’s sovereign gold bonds possible to buy at Zerodha?

Thanks again, so much.

Harsh

1) You need to have funded your trading account go buy G Sec (like the way it works for MFs)

2) Yes, check this – https://zerodha.com/gold/

Great 👍, Thanks.

Looks like I missed the recent window on Oct 19. Is there another window coming up at Zerodha? Thanks for your answers and guidances.

Not really, bids will be open from Monday to Tuesday and will close at 8 PM on Tuesday. Bonds open on Tuesday and close on Wednesday.

Very nicely explained.

Happy learning, Nirmala!

hi

need to know the tax structure for G-Sec. they are taxed like EQ? LTCG STCG 10 % and 15 % resp.

A bit of confusion here.

Also on RBI’s portal Faqs it says do not buy Gsec from a brokerage firm , instead buy it from E-Kuber RBI banking platform. need clarification on this

They are taxed exactly like the debt MFs, Nikhil.

Btw, I’m not sure why RBI would say that 🙂 Can you please share the link?

HI KARTHIK

I WANT TO INVEST IN 91 T-BILLS FOR 31 OCT 18 AUCTION … HOW TO PROCEED,, SHOULD I MAIL DETAILS TO ZERODHA ?

There is another auction coming up on Monday. You can please order here – https://zerodha.com/gsec/

Hi,

Can I book/buy T bills or bonds thru Zerodha mobile (Kite/Coin) APP ??

This is part of Coin, check this – https://zerodha.com/gsec/

Hi ,

Can we invest in State Govt Security like 8.73 KA SDL 2033 which is having high YTM. What is the liquidity situation .

Not for now, Suresh. Hopefully in the coming days.

In Bank FD you wil get compounded interest but in bonds you will get simple interest? Am I correct?

Yes. In fact, ppl reinvest the coupons in other investment…this way they ensure compounding continues.

Hi Karthik,

Is the Bank paying 7% per FD is better or G-SEc or T-bills better?

The government notifications for future g-sec and t-bill publish the rate of interest upfront? where can we see those details ? would like to compare the Bank FD rate of interest with gsec or t-bill rate of interest before investment..

can you pl explain me.

For short term, T-Bills rates are comparable to FD.

For longer terms, with Government bonds you can lock-in a high rate of return and continue to receive guaranteed interest payments. There are bonds available going up to 2055. With FDs you can only go upto 10 years.

Once these bonds list on the exchange, you will also get the advantage of exiting early while FDs charge penalties for premature exit.

You can find details for future issues here

Hi,

I have a query. if i am investing now in T bill 91 days. how will i get the interest and what is indicative yield ?

You will be paid the interest upon maturity i.e 91 days. The yield is about 6-7%, based on the competitive bids.

For T-Bills, when you invest, the blocked amount is in multiples of Rs 10,000. Once the cut-off price is decided, the interest amount is credited to your account.

For example, for a Rs 10,000(100 units) T-Bill with a cut-off yield of 7%. The interest for the period will be 1.75%. You will receive Rs 175 to your account. On Maturity, you will receive Rs 10,000(for an effective investment of Rs 9,825)

Since the interest rate yield is only decided in the bidding that is conducted by the RBI. We display the indicative yield based on past issues.

Hi Karthik,

If I am buying T Bills, will the transaction or status will be shown in coin, as it shows for the mutual funds. If we invest some amount how we will come to know that how many /quantity t bills are credit in our demat account.

Thanks,

Manish

Yes, the status will show as Processing/Allotted/Rejected. The number of units will be in multiples of 100(Face value of Rs 100, 100 units for an investment of Rs 10,000). You will also receive a confirmation email after allotment.

Why does the article say that t-bills could give a return of 12.4052%? Is it an error because that’s too high

It is not an error (mathematically), but yeah, I do agree that it is quite high for t-bills. Will fix it.

Hi,

When we put money in equity trading account that money will use used for purachasing G Sec I suppose. Now, do the client need to mention the specific GSEC security to buy or will ZERODHA buy which is having maximum Yelid to maturity security ?. How the process of purchase of GSEC works

Second – when we want to sell GSEC how is the liquidity situation – If we need money can we sell and get the amount within weeks time?

Thanks & Regards

1) Suresh, you will have to select the GSEC you’d want, we won’t be able to do that for you :). I’d suggest you log in here and check – https://coin.zerodha.com/gsec

2) NSE plans to list these GSECs soon in the cash segment, once this happens, you can sell this like any stock.

on which date the bonds will get matured,i mean on exactly after stipulated peirod or at the year end

You can check this link on RBI – https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11403&Mode=0

Happy to know and participate in GSec’s online – thanks for bringing this to retail investors.

I got 7.59% GS 2026 allotted to me on 17th Oct. The e-mail from ZeroDha said auction rate was 97.98. So I was expecting to get 5103 units. Instead i got 5000 units. Could you help explain the gap please? Does ZeroDha charge 2.2% commission on GSec’s?

Abhay, no Zerodha does not charge 2.2%. We charge Rs.6 for every 10K of investment. The balance money will be credited to your bank account.

Hi,

Is there any way by which I can indicate that I want to reinvest the interest in the bond itself?

My understanding is “no”. But please correct me if wrong.

Thanks,

Manan

That’s right Manas, not possible. The coupon payments hit your bank, you will have to manually reinvest this.

Hi,

Recently i purchased Gsec 740GS35O18 from Zerodha terminal, I understood this is a re issue. I checked in RBI archive page to know the coupon payment dates, no luck. Is there a easy mechanism to check the payout dates from the security code ?? Any pointers in this regard is highly appreciated.

Thanks,

Divakar

740GS35O18 ? Are you sure? I don’t think this symbol exists. I think you are referring to 7.4% 2035 maturity. Check the details here – https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11399&Mode=0

I think stocks are better than G-Secs. Investing Rs.10000 would give you 25-35% annually.

There is no capital risk in GSecs. Remember, its guaranteed by the Government.

Hello sir,I buy NSE bond future 717gs2028 at value 96.07 total 5 lot(overall 24000rs).how much interest will I get after yearly settlement? Do they calculate interest on real invested money or this future is based on margin?

You will receive 7.17%*24000 = 1720.8 per year. The interest is paid on the invested amount.

Thank you so much sir

Welcome!

Sir I am highly interested in g security and want to hold it for 10 years. So do I need to buy each month contract like December ,January etc. ? And second after 10 year maturity will I receive 24000rs or more since I buy it below par value?thanks in advance

You just have to buy it once, Yogesh. There is no concept of ‘rollover’ here. As long as you hold the bond, you will continue to receive the coupon payouts.

Hi,

I have placed a order to Buy T-bill in Gsec, how much time it takes to process.

The settlement is on a T+5 basis, request you to check this next week.

Thanks

hi,

I had placed a order to buy T-bill in Gsec on 30/10/2018, in status column message is displayed as “placed” where as in the remark column it displayed as “Order placed-pending verification”.

Please let me know how much time it will take to execute.

Is investing directly in G-Secs better than investing in a liquid fund (if the fund invests only in G-Secs)? if yes, then how?

Yes, because the fund has an expense ratio which eats into your return.

so you are charging 0.06% at buy, is the commission same while selling at your platform?

any chance of looking at this question please?

Sorry, I dont know how I missed this question, Kamal. There are two possible scenarios here –

1) The instrument eventually lists on the exchanges and you sell via the exchange. For this case, the brokerage is not fixed as of now.

2) You write to us and request for a sell. No brokerage here.

sir

pls, clarify the charges charged by coin/zerodha as buying and selling both.

Sir I buy 5 lot gsec 717gsoct2028 at 96.07 invest 24000 rs.after maturity will I get 24000(capital)+39000(coupon @100)+interest? Is it right calculations?

Yogesh, no you will not get 39000 as the coupon payment. The coupon rate is 7.17%, which mean you will earn 1720 per year or about 17208 over the tenure of the bond.

Then what’s meaning of par value?I’m in still loss because bond future price reduced.should I sell off bond because interest profit smaller than loss actually realized?

I’m confused. If I invested gsec at discount of 3rs suppose 97.will I get 100rs at maturity?what happen if I invested at premium suppose 105 shall I receive 100 par value?

Yes, you will lose 5, but still continue to get the coupon payments.

Par value is the face value. There is no loss here, Yogesh and there are no bond futures here. Hold this to maturity and you will get all the coupon payments. Also, please read this chapter once again.

So far it is messed up for me, team says bonds are allotted to me but i didnt got any mail from bse. I have asked for order details which is not provided yet.

Will look into this, Nishanth.

Hello Karthik,

The article was really well explainatory.

I have invested 10k in T-bills on 05-Nov

I read somewhere in comments that to reflect the T-bills,it will take T+ 5 days.

I am patient because of your above comment as no mails received about confirmation of my order & money is deducted from Zerodha account so waiting for your positive response.

Can you please confirm if it will be reflected in holdings of Zerodha ?How will I get to know at what discounted value I have got the T-bills?

Can I get info who was main bidder for the T-bills in which I have inveated.

Also please advise if we get different discount at different time (like on Monday it is different & on Tue it is different)

Thanks

Sanket, the price discovery happened on 6th Nov (auction day), but the settlement is today (there were holidays this week due to Diwali). You will receive the units within the next 5 working days. Btw, you should have received the refund by now, so this will give you the buy price (auction price).

No, we wont get to know who the main bidders are, but they will be the primary dealers recognized by RBI.

Will I get 7.17% interest yearly and do I need to square off November contract?https://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuoteIRF.jsp?underlying=717GS2028&instrument=FUTIRC&expiry=29NOV2018&key=FUTIRC717GS202829NOV2018–09NOV2018

Yes, 7.17% is the yearly coupon. The Bond/T-bill, upon maturity is considered extinguished and gets automatically debited.

But I’m facing interest rate risk.what should I do if bond future price reduce day by day I.e. rising yield and losses is consider high?

If you hold to maturity, then you wont be facing this risk.

Can declare this investment in Income Tax section 80C.

No, these are not exempt under 80C.

Hi

I bought the G-Sec bond 91 Day T-Bill, the amount it is showing in my account is 9830. While amount deducted from my account is 10k.

why this amount is deducted from my account. I heard that the profit earned on T-Bill is the discount amount, but amount deducted from my account is full.

T-Bills are not bonds, they are money market instruments 🙂

By definition, bonds are debt instruments which have a maturity period of more than 1 year.

The difference amount will be credited to your bank account, can you kindly check?

Hi

Even I bought the G-Sec bond 91 Day T-Bill, the amount that is shown in my account is 9830. While amount deducted from my Zerodha account is 10k.

Why this amount is deducted from my account. I heard that the profit earned on T-Bill is the discount amount, but amount deducted from my account is full. Also, no difference amount has been credited to my bank account as was told by you in one of the previous questions

The settlement date was Friday, I think you will receive the refund within this week.

Dear Sir

I have one suggestion. Why don’t you publish all the modules available in the varsity as a book and sell it online. We would like to buy that.

Why so, Kumar. The PDFs are freely available for you to download 🙂

Actually i have already downloaded first three modules of the varsity, printed the same and hard binded as a book. I feel like it is more convenient way for studing the modules. So just sharing my feelings.

I’m glad you thought the content was worth taking that kind of the efforts 🙂

Thank you so much sir.how can I get information about “nse bond future”? Any Link or PDF will be helpful.

Everything that you need to know – https://www.nseindia.com/products/content/derivatives/irf/irf.htm

The profit on T-bills is STCG and taxed at 15%? Can you kindly confirm. Thank you.

Govind, T-bills are bought at discount and sold at par. This appreciation is considered other income and taxed at your over all tax rate.

Thank you so much sir.what is best way to hedge NSE bond future price?debt MF or any other instrument?

The biggest risk with bonds is the interest rate risk. So yes, in a crude sense maybe you can buy a debt MF.

Hi

T- bills is a great option for investment and glad that you have facilitated this. Can I sell Tbills ( 91/182/364) before maturity and if yes is the facility enabled by Zerodha?

Sankar, yes, you can sell before maturity. Write to us on [email protected]. But I’d suggest you hold to maturity to reap in the full benefits.

Thanks Karthik. In normal course yes- shall hold till maturity.

This to be exercised only in case of exigencies-

Sorry to trouble you but is there somewhere I can read up and see the quotes etc – only for information sake.

I get that. Unfortunately, quotes are not really available. This is otherwise an OTC market.

I placed an order for 10Lakhs Tbill 91 day – The order is showing pending for over two weeks. Please suggest?

hi,

I had placed a order to buy T-bill in Gsec on 30/10/2018, But still it is not executed (in status column message is displayed as “placed” where as in the remark column it displayed as “Order placed-pending verification”).

Please let me know how much time it will take to execute.

Dear sir,what’s difference between gsec and nse bond future?will I get interest if I short one leg and long other one?

Consider the G Sec as the underlying (spot) and the IRF as its futures. No interest is paid for holding futures.

Hi

Can the OCI card holder purchase this bonds ?

If YES , can you let us know the TAX implication on the returns each year and when they sele the bonds ?

Thank you

1. OCI card holders can invest in government securities subject to compliance with the provisions of Foreign Exchange Management Act,1999. You may check this Gazette notification to know more: https://rbidocs.rbi.org.in/rdocs/content/pdfs/GOI27032018_A.pdf

2. You can refer this for info on taxation: https://www.nseindia.com/products/content/debt/ncbp/Taxation_of_Government_Securities.pdf

hi,

I had placed a order to buy T-bill in Gsec on 30/10/2018, But still it is not executed.

Please let me know how much time it will take to execute.

The order would have been processed and the T-bill should be in your DEMAT. Can you please check your holdings once?

T-Bills still not credited to my DMAT.

Placed order on 30/10/2018.

Satish, can you please create a ticket on https://support.zerodha.com/category/mutual-funds/government-securities for this? Thanks.

1. Can NRIs invest in GSecs?

2. If someone who is an ordinary citizen of India buys bonds today and becomes an NRI later, will the interest keep on getting paid into the linked bank account? what will be the tax treatment?

1. NRI’s can invest in government securities subject to compliance with the provisions of Foreign Exchange Management Act,1999. You may check this Gazette notification to know more: https://rbidocs.rbi.org.in/rdocs/content/pdfs/GOI27032018_A.pdf

2. If your residential status changes from a resident to a non-resident, you will have to inform your bankers and DP where you are holding the securities. Your ordinary account will be changed to an NRI account. The interest will get credited to your NRO savings account which will be linked to your DP. The interest income or capital gains arising will be taxable as per the applicable tax slab. You can refer this for more info: https://www.nseindia.com/products/content/debt/ncbp/Taxation_of_Government_Securities.pdf. Also, suggest you approach a professional tax consultant for more info on the tax liability.

hi

I placed a order of 10k for t bills through zerodha gsec. Fund as been deducted from my account but it doesn’t reflect anywhere in kite as well in coin nor I got a mail from zerodha about the transaction .

can u please help

Did you place this order on 12th Nov? The units will hit your DEMAT on T+5 days from settlement. The settlement for this would be on 14th Nov.

Dear sir ,I could not find 717gs2028 bond security in coin,other bond having maturity 2020 2023 2032 etc are availability. So how can I buy 717gs2028 underlying

That bond is not available for bidding now, Yogesh. Check this link – https://nseindia.com/products/content/debt/ncbp/ncbp_issues.htm

Can we pledge T-Bill and Bonds to get margin for selling options? Also what would be the applicable haircut on pledging the same, how much margin would we get?

Vivek, yes eventually you will be able to do this. But for now, you cannot pledge these securities.

what is the approximate time frame can we expect for pledging to be active in govt securities? Are there any regulations which currently prevent Zerodha to do this?

Unfortunately, I cannot commit a timeframe, Vivek. But I’m hoping this will be real soon.

I applied for G-SEC in ZERODHA on 30th Oct, still I did not get the update on the application. still it is showing as “Order Placed – Pending verification” in Dashboard. How long will it take to reflect the status to allotted or not allotted. ?

Bhargava, can you please create a ticket here – https://support.zerodha.com/category/mutual-funds/government-securities for this? Thanks.

Hi,

Where can I check the coupon rate for RBI issued T-Bills.

Check this – https://www.rbi.org.in/scripts/bs_viewcontent.aspx?Id=1956

Hi,

I have sent an email to [email protected] to sell my “#20181105405000 – SELL MY 91 Day T-Bill”.But no response on that in 10 days and i’m not sure if T-Bill can be sold in secondary market.I think this is my First terrible customer service experience with Zerodha. Appreciate quick response and resolution.

Will look into this, Sindhu.

Hi,

My issue has not been resolved but my ticket has been closed with out any proper comments.

Can you answer my question ” if T-Bill can be sold in secondary market”????????

T-Bills are not listed in the secondary markets, yet. The exchanges are working towards making this happen. No timelines yet. Meanwhile, if you want to sell, please write to [email protected]

Also, please do share the ticket number. Thanks.

Hi

I have ordered 300 units of 91Tbill on date 13/11/2018 and same I have got it @ re 93.31

Hence I am getting ytm yield of 6.895%

You are charging brokarage of rs 6.96 per 100 unit which is at quite higher side and the ultimate yield is reduced to 6.605%

I am senior citizen and my bank is giving 6.25+0.5=6.75% interest on fd

So purchase g sec through is costly dur higher brokerage charge

So request pl reduce the brokerage charge

Sir, 91day T-bill was at 98.3 and not 93.31, also the brokerage is Rs.6 per 10K Sir. How much more do you want us to lower the rate?

Sir,

While you suggest us to Invest in T-Bills because it gives a better return than FDs. And you give comparative figures of yield on T-Bills/Bonds and FDs (which serves us better to compare and take the decision. That is a good thing and I really appreciate you for that). But while you give us the comparative yield figures, there is a catch, you don’t account for the cost of Investment (brokerage, fees) and Banks provide quarterly interest compounding on FDs which increases the actual yield on FDs. A word of caution regarding the cost of investment and other things would help investor better in judging the investments and taking the decisions.

We don’t expect you to lower any fees or brokerage but we expect you to account for these things while providing us the actual yield information.

Vishal, the transaction costs are clearly mentioned on the home page – https://coin.zerodha.com/gsec

I Agree with Vishal

I had ordered 2200 units of GSEC 740GS35N18, at INR 9027 per unit amounting to INR 1,98,594.00. I understand INR 148.87 is brokerage at 0.06% of INR 1,98,594.00 + GST. Now I see an extra amount INR 11,679.65 being deducted today. Why is this deducted? If this is it, please explicitly declare this in your Documentation explaining GSEC else investor gets misguided(that actual price we investor pays will be known only after alloted , and the indicative par is no longer valid, why would I invest 7.4% if I dont get the par value!!), that what we order and what can be deducted is different. Unreliable to order the units if I dont know how much it is costing me!! Absolutely Crazy for making in informed decision, not investing in this BS anymore

RBI WEBSITE HAS THE FOLLOWING SCHEDULE FOR TREASURY BILL IN NOVEMBER 2018

20-Nov-18 22-Nov-18 7,000 –> 91 days

YET THE T BILL WINDOW IN COIN SHOWS :

Currently no issue open. Bidding opens again next Monday.

WHY ?

Im looking at short term g secs as I need liquidity .

The bidding for T-bills is on Monday/Tuesday and Tuesday/Wednesday/Thursday for G-sec.

if you noticed it is still a tuesday when i mentioned. i wish i could post a screenshot. but i cant.

take your time and look into it. I wish i got a more detailed answer.

I just wish coin had a total charges calculator so that people knew how much money they need for an investment into bonds/t bills.

So just for my information and others as well , please work out this example:

a 91 day t bill offered at a hypothetical value of 9821 for a par value of 10,000.

please calculate all the charges(GST, STT whatever that may be applied onto this.)

and the final amount credited at maturity .

I will do my income taxes on the final value.

looking forward to your reply.

Aditya, thanks. We will have try and have t-bills/G-Sec on brokerage calculator soon.

Please tell me why I shouldn’t invest all my money in t bills rather than bonds or stock market because there are two reasons I think makes it a genuine choice

1. It has less period of completion so I will not be charged tax for LTCG and thereby better than a bond investment

2. It assures me that my money wouldn’t go down because as you said buying a t bill is like buying a stock for 97 and then selling it for 100 at the time of completion so it makes it better than the stock market.

If this suits your return requirements, then fair enough. People opt for equity for higher returns.

Can you please give me a few reasons why bonds are better than t bills if we leave equity aside?

Bonds give you regular cash flow in terms of interest payouts, plus you can also lock in attractive rates for a longer term.

Hello,

So 6 Rs for every 10K is brokerage. Got it.

What about the taxes (STT or GST etc) for purchase transactions?

Also, if one decides to sell his Tbills/Bonds before maturity, brokerage/taxes still applicable? It would make more sense if you create online calculator where one can find the final maturity for T-bills & bonds.

We will put up a brokerage calculator for this sometime soon.

BTW, why would one email you to sell? can I sell it myself on secondary bond market like usual stocks/ETF we sell on NSE/BSE?

Email because we will act as counterparty till the time exchange lists these securities in the cash segment.

1) Any idea when exchanges are officially going to list it in cash segment for retail investors?

2) Safe to assume the liquidity in the proposed segment/market is going to be ZERO/insignificant initially?

3) If you’re going to honor all the sell requests by your clients? How do you discover the price of sell in that case? Most important of all – do zerodha honor all the sell requests submitted by clients?

1) 17th Dec is the expected date

2) Market making is allowed, so I think there should be liquidity

3) We would take quotes from other institutional participants. However, this is no longer required as the product is listing on the exchanges and the pricing would be market driven.

1. In case we want to sell Tbills, What is expected timeline for receipt of funds?

2. Brokerage of 0.06% on 90 day tbills is insanely high..Zerodha we are used to low fixed fee:)

3. 90 day T bills will be short term capital gain, right?

1) Usually takes about T+6 days

2) Rs.6/- was the lowest we could think of 🙁

3) Yup.

Have a look at RBI press release for 91 T-bill auction for today – https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=45588

The numbers for non-competitive bids are very interesting . Total bids received are 8 worth ₹ 14,801.465 crore. huh?

If retails investors are mostly allowed in NCB, how is the amount so high? Or may be they want to say 14.8K?

They count the bids at the member level. So if NSE and BSE take the order, then its considered as 2.

Hello Karthik Ji,

My concern is about the taxation. Let’s say by trading stocks I made 15% i.e Rs.6,00,000 in 6 months.

Now I put all of the 6,00,000 in a Tax Free government security of 180 days . After that I do not do any transaction for the Entire Year.

So what will be my tax liability for the year assuming I have no other income sources.

Will I be charged for LTCG on my Trade or can I omit LTCG since I invested all the money in a Tax Free Bond.

Nishant, there is no tax-free Govt security maturing for 180 days. You will have to pay STCG on this. I’d suggest you please speak to your CA on this. Thanks.

Hello Karthik Ji,

I have another question. So as we all know that we are liable to pay 15% STCG & 10% LTCG.

Is there any way by which we can omit the taxes may be investing our Gains in any Tax Free Bonds.

You can offset the gains with losses carried forwarded from the previous years (if any). More details here – https://zerodha.com/varsity/module/markets-and-taxation/

Hello Karthik,

Please help me with this. I have short-term capital losses for a year from Equity shares. Can I adjust this short-term capital gains from Treasury bills?

Yes, Parag. You can do this.

Thank you for answering the query.

However, I have drawn some inferences and need your endorsement on the same.

1. The article mentions “T-bills – You buy at discount and sell it at par. This appreciation is considered as short-term capital gain, and taxes as is per the applicable slab rate.”

This means this STGC will not be taxed at 15% (unlike STCG tax on sale of equity shares) and will be taxed as per my tax slab. Correct or Incorrect?

2. Are T-bills and Zero Coupons bonds the same or T-bills is a type of Zero Coupon bond?

3. In many sources of information, the appreciation in T-bills is considered as interest income? If that is correct will I be able to set-off losses from equity shares with gains from T-bills? It will be Capital losses vs Interest income. Doesn’t seem correct. Can you please help me with this conundrum.

Thanks in advance

The price we pay is decided by the MAJOR BANKS & FINANCIAL INSTITUTIONS.

a) So, when we buy via COIN, is that price decided by ZERODHA ?

b) what are the criterias & procedure for FINANCIAL INSTITUTION to be able to bid directly on RBI auction portal ?

a) Remember, this is non-competitive bidding for retail, we just collect bids and place the order with the exchanges.

b) You need to be a bank or RBI approved primary dealer

Allotment price of very recent Bond 8.24% Government Stock, 2027 is 104.49 RS for Non-Competitive Bids.

So per value of this Bond is 100 or 104.49?

if per value is 104.49 then interest rate is not 8.24, right?

if the allotment price is 104.49, that that is the price. The interest rate stays fixed at 8.24%, that would not change.

Thank you.

Welcome, Hardik!

Can G-Sec able to pledge. If not when this will be available.

Yes, it can be. This should be made available soon.

That’s Good Karthik. Do we have any estimate.

Hopefully over the next quarter 🙂

Hi Karthik,

Is there any update. Looks like we have passed one quarter 🙂

Regards

Shankar

Not yet, Shankar 🙁

besides 0.06% brokerage, do you charge demat transaction fee for T-bills?

No Sir, we don’t.

Hi,

can we decide which g-sec bond I would like to buy. say can i buy 737GS2023 and not 662GS2051..

because when I goes to ‘Start Investing’ Link given in Coin, i cannot find any such option to choose.. am i missing something

Pramod, whatever is available for bidding is what gets shown on Coin. If there are no issues, then you won’t see this.

I am new to the stock market

can i invest in G-secs with just an amount of 10,000 rs.

Yes Sir, you certainly can.

Hi,

Just like other users experience in comment section, I placed a G-Sec order and deadline is passed, but I still see the following status: “Order Placed – Pending verification.” Could you elaborate what this status means?

Also it would be good to describe it in this chapter (even, if this is specific to Zerodha workflow).

Hi,

Please provide T-bills calendar for the quarter JFM 2019

Thanks

Anurag, check this – https://tradingqna.com/t/issuance-calendar-for-treasury-bills/49991

hey, It’s my first time to purchase a T-bill as i placed the order my status to that order comes with a remark ” Verification pending” may i know what does that mean? and is there something which i can do?

Shiva, the order will be placed on T+2, until then its the collection period. Hence the ‘verification pending’ status.

Do we get any 80c benefit or some other tax benefit when we invest in G-secs or T-bills ?

Nope, no 80C benefit on the GSec investments.

kindly advise in which bond or T bill, we can get monthly interest . Like FD

or advise best scheme with govt guarantee in which we get monthly interest instead at the time of maturity.

No bond pays a monthly interest, Naresh, at best bonds pay semi-annual interest. The semi-annual payments are made by the Government bonds.

If I hold 10 years bond, can I exit in 2 months? What will be the interest I gain if I sell and what would be the other charges involved?

So instead of holding T-bills I can hold bonds instead and sell as I wish correct? Then why would anyone buy T bills.

Hi Karthik,

Hope you are doing well!

Firstly, I would like to thank you for replying to all your the queries asked above. Having said that let me bother you by asking another question

It says that the bond interest is paid semi-annually and will be credited back to the associate bank account, So is there any feature available using which I can configure as to automatically invest the interest received back into the bond?

Thanks

Rohit Saluja

Rohit, unfortunately, that option is unavailable for now. You will have to manually do this for now.

I’m trying to bid for 91 day T-Bill today (04/03/2019) – Monday, it’s saying there are no issues today, try again next Monday. What it means??? Could you explain!

That means RBI has not opened any bids!

Even today there’s no openings!! In kite

I guess there is auction today, please check Coin – https://coin.zerodha.com/gsec/invest

I have bought 100 units of 8.24% GS 2033, I have to pay 11581 rs , I think its contains the 0.06 % charges . But at this moment the amount is showing 10,666.96. why there is a difference

The difference amount will be known when the final offer price gets discovered by the bidding process. The balance amount will be credited back to your account.

For TBills, your brokerage is ₹6 per ₹10000 investment, that is for 91 days. This works out to be ₹24 per ₹10000 per year. This is quite close to expense ratios of actively managed debt funds. So zerodha brokerage seems very expensive in case of TBills.

Ok.

Hi,

Can you please explain indicative yield? What is it’s purpose?

I see an issue 8.24% GS 2027 open for bidding now with an indicative yield of 7.49%. Does this mean I will not get 8.24/2% semi-annually and only get approximately (based on the bid) 7.49/2% semi-annually? If my understanding is incorrect, what exactly is indicative yield? Thanks!

Indicative yield is to help you get an understanding of earning potential (in % terms). Here, 8.24% is the coupon rate (paid semi-annually, so 8.24%/2)…and 7.49% is the capital appreciation in the bond itself.

Thanks for your reply. I understood the coupon rate part but not the capital appreciation part.

Could you please explain how the capital appreciation works for a bond lets say 8.00% GS 2029 indicative yield 7% (10 year bond for example) and tell me what I will earn semi-annually and what I will get at the end of the bond when I invest Rs. 100000 now.

A detail of the calculation will help as well.

Another request, could you please build a bond calculator as well if time and resources permit.

Thanks!

Lets say, the face value of the bond is 10K, you’d pay 7.5K for it today…but upon maturity, you will get back the face value i.e 10K. So there is a capital appreciation here, and this is what the indicative yield suggets.

If the coupon rate is 8%, then you’ll get 4% every 6 months, this is semi-annual coupon payment.

Dear Karthick,

I have placed a T-bill order this Monday, the amount related to it has been deducted from my account. I’m yet to receive its transaction details via mail/ any communication . Meanwhile kindly help me out to track the same in coin app( as navigation in coin is not easier for me) since I have been trying hard.

John, usually you will get the units on a T+5 basis.

Sir how do I buy Corporate Bonds/ Debentures through Zerodha platform? Where can I find the list of Debentures that are currently available for subscription?

Yes, check this – https://coin.zerodha.com/gsec

Bonds ko maturity sa pahla sell kr skta hai….???

Yes, you can.

Hi,

When I read through the G-sec doc T-Bill section, I find the following:

“What happens upon maturity of a T-bill?

Upon the maturity, the Government debits the T-bill from your DEMAT automatically, this is called ‘Extinguishment of Securities’ and the par value gets paid to the bank account linked to your DEMAT account.”

-So, once the 91 days are over and my T-Bills are matured, all the mentioned process will be happening automatically? Or is there anything should be done from my side?

And, what is the Brokerage amount Zerodha charges for G-sec transactions?

Yes, that happens automatically. Brokerage is 6 paisa….so about Rs.6 for Rs.10,000/- of investment.

Dear Zerodha, any update on pledging the G-Secs?

We have been waiting for it since a long time….

Please give it a priority

This is on the list of things to do. Hopefully soon.

Dear Zerodha,

I buy 100000 G-Sec 20 yer 8.34

interest withdrawal yearly basic ?

The interest on G-Sec is paid semi-annually.

For This Bond 7.26% GS 2029 can i know how the indicative yield is higher than bond coupon if the bonds is trading at Premium (105.5)

THanks

VInod

Vinod, 7.26GS2029 is currently trading at Rs 98.7. You can check the yields of all bonds and t-bills here: https://www.ccilindia.com/OMHome.aspx

Please clarify this for me:

Imagine i have taken and got allotment worth Rs. 5Lakhs on Goverment Securities at ROI 7.5% for 20yrs. Now if RBI cuts Interest rate at 7.25% during 2nd year, will my allotted securities ROI also changes or will it remain the same like in Fixed deposits ?

The coupon rate will remain the same, the yield however will change. But if you intend to carry forward this position till its maturity, then you need not have to worry about this.

Thanks Karthik for replying, can you please Elaborate this part with figures to understand better.

Which part, John?

I need to know like i invest say about 10 Lakhs for 20yrs, what will be my semi-annual returns if at all there is a drop in ROI on 2nd year and what if the drop in ROI continues down the line, say for 3rd year, 4th year….so what will be the effective Returns that is been paid to me (semi annually) under these circumstances ?

The semi annual return depends upon the coupon rate of the bond. So for example, if the bond has a coupon rate of 8%, then you are entitled to 4% every six months. Bonds are capital protected (you can check the ratings), and if you hold for complete 20 yrs (called held to maturity), then there is no problem with drop-in ROI.

Will 772GS2055P (7.72% GS 2055) be available for further allocation ?

It last available on 15-Apr-2019.

Not really sure, Somnath. Depends on the RBI’s auction dynamics.

Thanks

I see Outstanding Stock for 7.72% GS 2055

https://rbi.org.in/Scripts/bs_viewcontent.aspx?Id=1956

Can you have a look ?

Outstanding is the one which is floating in the market. Not indicative of future issues.

Thanks Karthik.

Good luck!

Don,t we use par value to calculate intt. On yearly basis while calculating for treasury bill.

Coz i studied during my CFA studies that the formula is discount/par value × 360/n !!!

If anyone could answer that would be great.

Are you talking about yield?

Can you all please start a chapter on corporate bonds or NCDs. Like how to analyse and all and most importantly where do I find the prospectus of old bonds.

Yes, Javid. I’ve been wanting to do this. Guess it will be a part of the next module on Personal finance.

Sir,

After reading this: Every bond has a Par value, of say Rs.100. When you invest in a bond, you usually invest either at a discount (ex: 98, 97 etc) or at par (100), or at a premium to par (101,102 etc). The price at which you invest in a bond depends on something called as an ‘auction process’.

Is there any way to participate in buying bond only for the discount price? I do not want to buy a bond premium or at per price. Could you please help!

Nope, right now the participation is allowed only for the banks and institutions.

Sir,

Bond ko maturity date se pahle sell kar sakte he? or sell karne pr interest milega jitne time ke liye hold kiya gya he?

Yes, you can sell the bond before expiry. Yes, you will receive the interest for the period you held the bond.

Sir,

Today I had place order for

Sec name: 7.63 % GS 2059

Maturity date: 17-06-2059

Initial Amount Block: 1,01,556.

Unit-900

I’m not sure whether I will get the bond either discount price or Premium price until the allotment process/auction process is complete.

For Example, if the final amount is the same as Rs. 1,01,556, do I get back in the maturity full amount of Rs, 1,01,556 ? or there is still a chance to get a Capital Loss due to Premium? Also, Do I get interested twice a year on Rs. 1,01,556 as well?

Please reply as earliest possible, so I can cancel the bid I place for if there is any change to get “Capital loss” due to Premium or any reason on the Maturity time, I never mind whether G-sec allotment me a discount or at a premium price until there is no change to get capital loss. I need back the entire amount in maturity I’ll pay.

The additional amount is towards the accrued interest payable to the previous bondholder. On maturity, you will receive 10L. You will receive the interest twice a year on 10L investment.

Sir,

For example, I am paying Rs, 1,01,556 I will get back of Rs. 100000 as well I will get interested twice in the year on Rs. 100000

upon Invest the amount of Rs. 1,01,556 and I will get back of Rs. 1,00,000 . So here I will lose my Capital of Rs. 1,566 am I right or wrong?

Please clear me if I misunderstand it! I UNDERSTAND IF I BUY THE BOND I WILL CAPITAL LOSE OF RS. 1556

Not really, Soumen. You will also have to account for the yearly interest you’ll receive.

Sir, I understand about “accrued interest” Thanks for the information.

Now, consider you invest in 700GS2020 (7% with a maturity of 2020 or 2 years from now) at a discount price of 98.4. Assume, you invested in 150 of these bonds, so you’d pay –

150*98.4

= Rs. 14,760/-

So on an investment of Rs.14,760/- you will earn –

525 + 525 + 525 + 525 + 15,000

= 2100 + 15,000